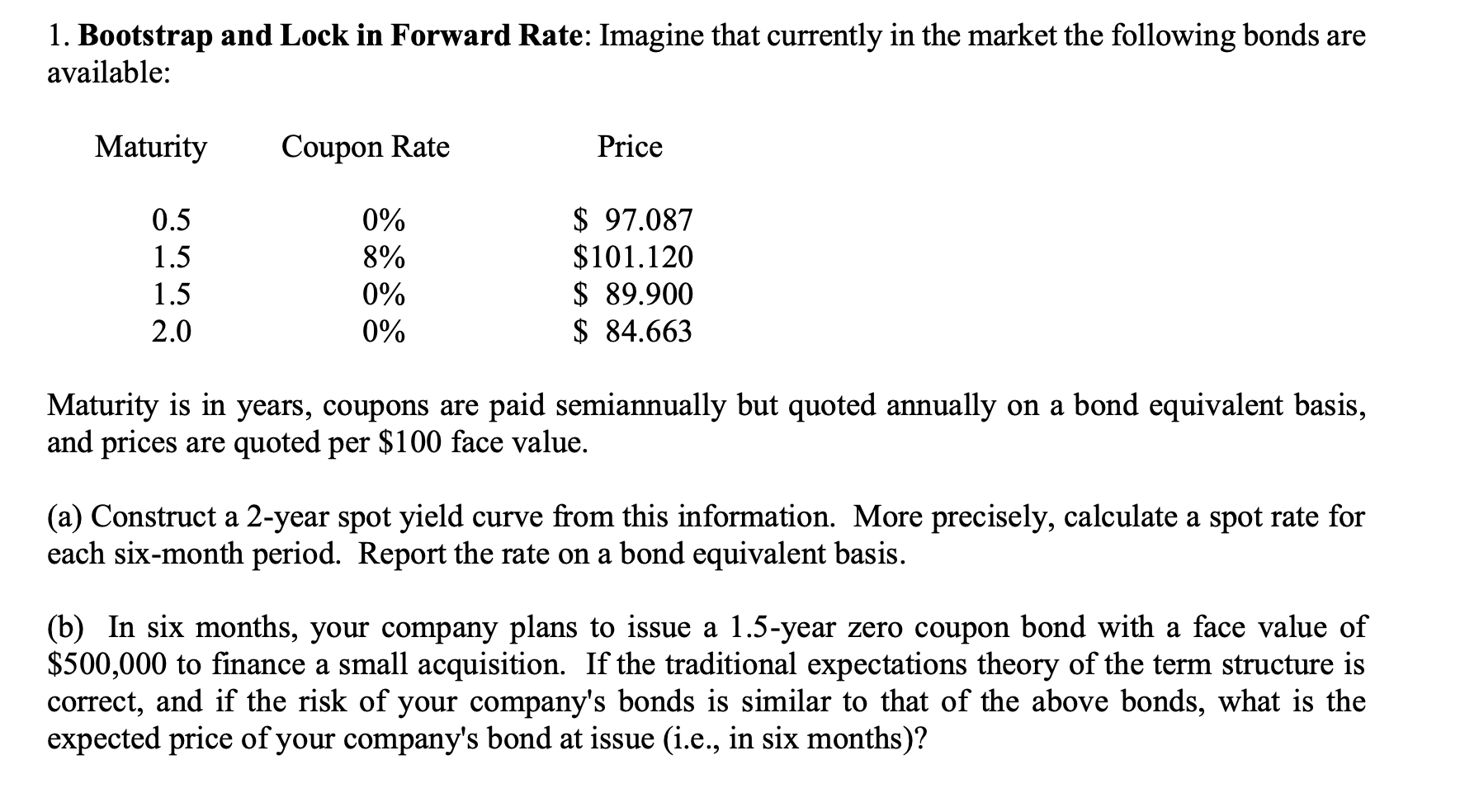

Question: 1. Bootstrap and Lock in Forward Rate: Imagine that currently in the market the following bonds are available: Maturity is in years, coupons are paid

1. Bootstrap and Lock in Forward Rate: Imagine that currently in the market the following bonds are available: Maturity is in years, coupons are paid semiannually but quoted annually on a bond equivalent basis, and prices are quoted per $100 face value. (a) Construct a 2-year spot yield curve from this information. More precisely, calculate a spot rate for each six-month period. Report the rate on a bond equivalent basis. (b) In six months, your company plans to issue a 1.5-year zero coupon bond with a face value of $500,000 to finance a small acquisition. If the traditional expectations theory of the term structure is correct, and if the risk of your company's bonds is similar to that of the above bonds, what is the expected price of your company's bond at issue (i.e., in six months)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts