Question: 1. Consider a $100 par value bond that has an 8% coupon rate, pays a semi-annual coupon, matures 2 years from today, and is priced

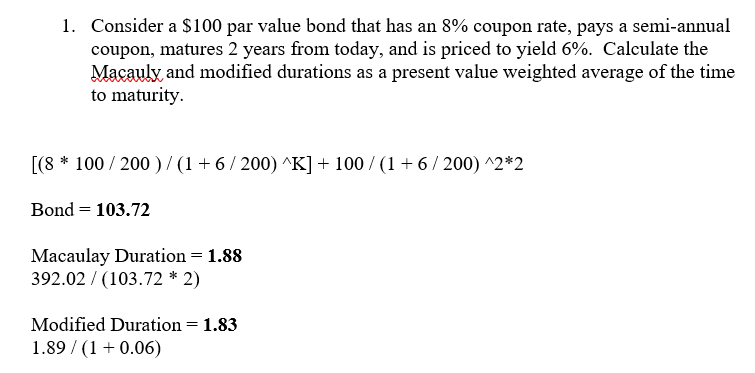

1. Consider a $100 par value bond that has an 8% coupon rate, pays a semi-annual coupon, matures 2 years from today, and is priced to yield 6%. Calculate the Macaulx and modified durations as a present value weighted average of the time to maturity. [(8 * 100 / 200 )/(1+6/200) *K] + 100/(1+6/200)^2*2 Bond = 103.72 Macaulay Duration = 1.88 392.02 / (103.72 * 2) Modified Duration = 1.83 1.89 /(1+0.06) 2. For the bond above, calculate the dollar duration and the price value of a basis point. 1. Consider a $100 par value bond that has an 8% coupon rate, pays a semi-annual coupon, matures 2 years from today, and is priced to yield 6%. Calculate the Macaulx and modified durations as a present value weighted average of the time to maturity. [(8 * 100 / 200 )/(1+6/200) *K] + 100/(1+6/200)^2*2 Bond = 103.72 Macaulay Duration = 1.88 392.02 / (103.72 * 2) Modified Duration = 1.83 1.89 /(1+0.06) 2. For the bond above, calculate the dollar duration and the price value of a basis point

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts