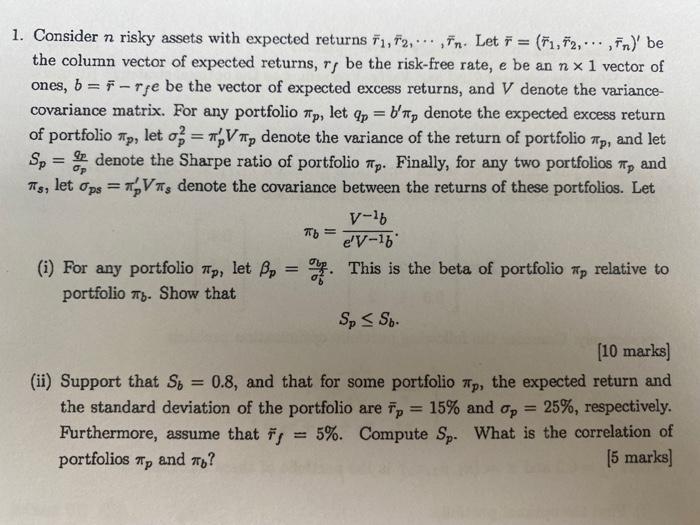

1. Consider n risky assets with expected returns F1, F2, Fn. Let F= (F1,F2,,Fn) be the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Differential Equations and Linear Algebra

ISBN: 978-0131860612

2nd edition

Authors: Jerry Farlow, James E. Hall, Jean Marie McDill, Beverly H. West

Posted Date: