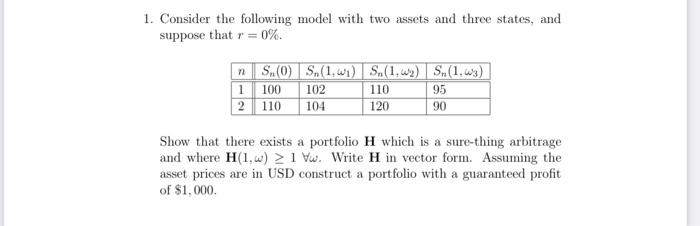

Question: 1. Consider the following model with two assets and three states, and suppose that r 0%. n S(0) S(1,w) S(1, w) Sn(1.3) 1100 2

1. Consider the following model with two assets and three states, and suppose that r 0%. n S(0) S(1,w) S(1, w) Sn(1.3) 1100 2 110 102 110 95 104 120 90 Show that there exists a portfolio H which is a sure-thing arbitrage and where H(1,w) 1 Vw. Write H in vector form. Assuming the asset prices are in USD construct a portfolio with a guaranteed profit of $1,000.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock