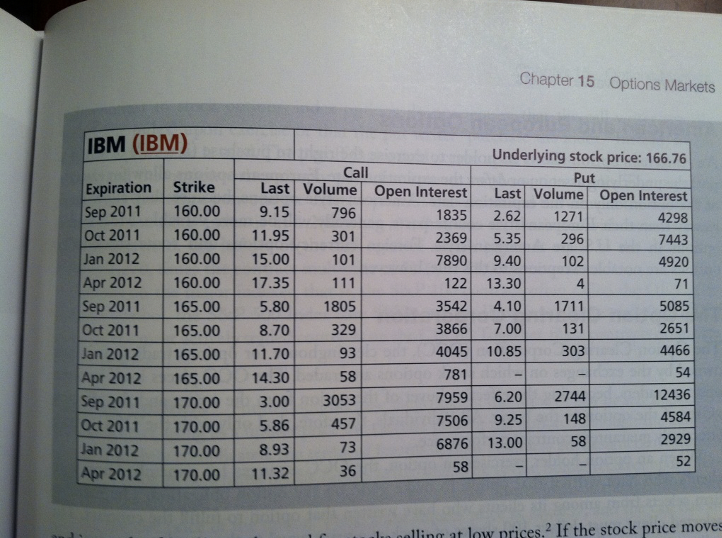

Question: 1 . Consider the following options portfolio: You write a January 2 0 1 2 expiration call option on IBM with exercise price $ 1

Consider the following options portfolio: You write a January expiration call option on IBM with exercise price $ You also write a January expiration IBM put option with exercise price $

a Graph the payoff of this portfolio at option expiration as a function of IBMs stock price at that time.

b What will be the profitloss on this position if IBM is selling at $ on the option expiration date? What if IBM is selling at $ Refer to Figure

c At what two stock prices will you just break even on your investment?

d What kind of bet is this investor making; that is what must this investor believe about IBMs stock price in order to justify this position?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock