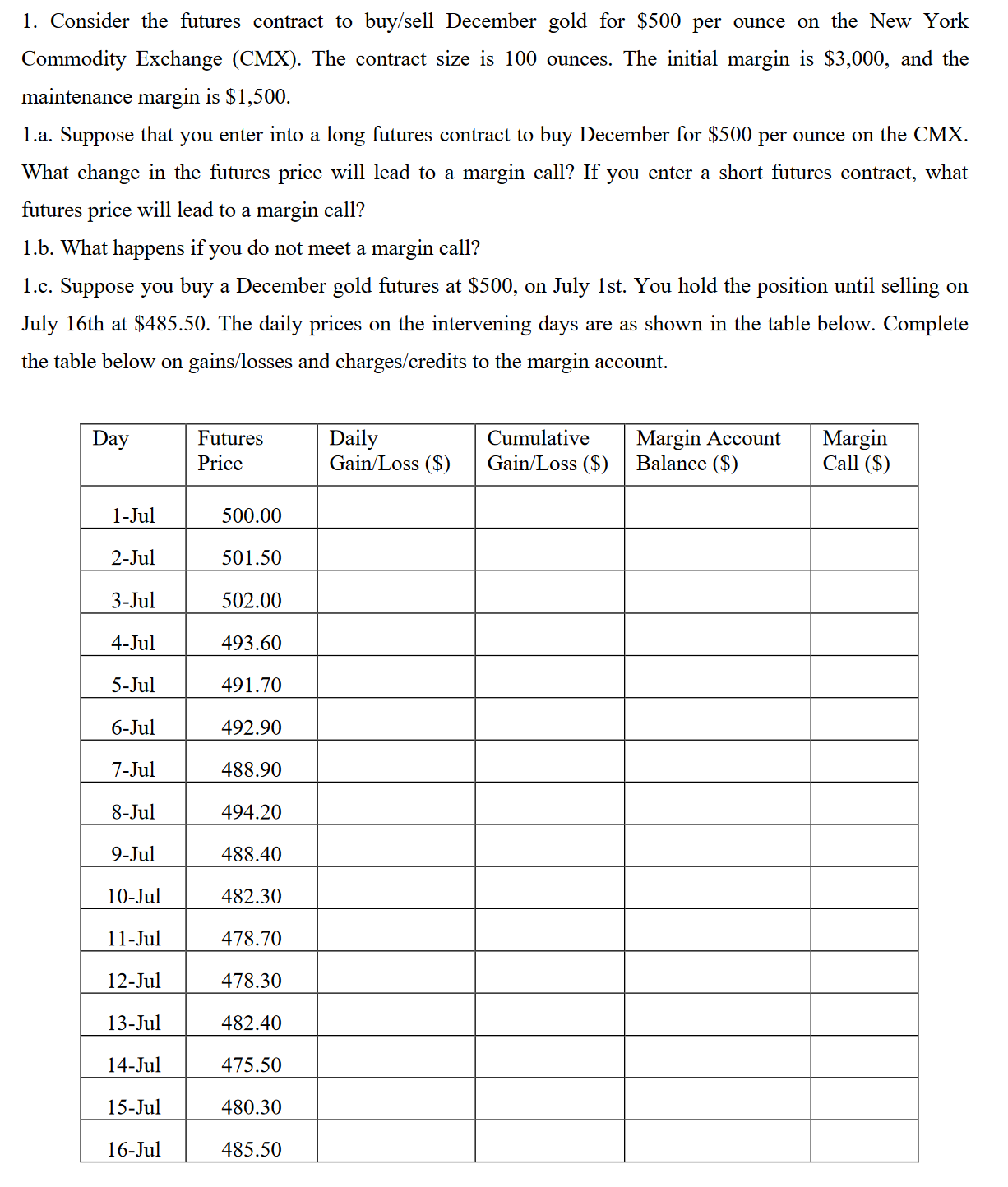

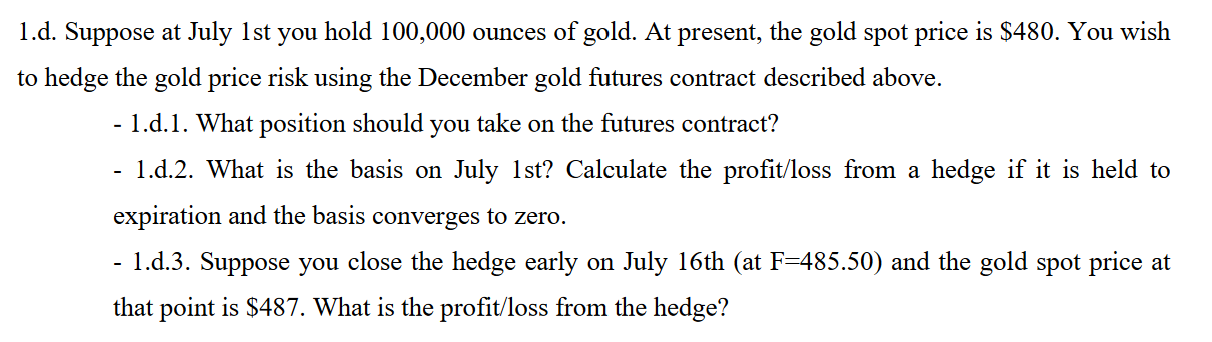

1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge? 1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge? 1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge? 1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge? 1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge? 1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge? 1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge? 1. Consider the futures contract to buy/sell December gold for $500 per ounce on the New York Commodity Exchange (CMX). The contract size is 100 ounces. The initial margin is $3,000, and the maintenance margin is $1,500. 1.a. Suppose that you enter into a long futures contract to buy December for $500 per ounce on the CMX. What change in the futures price will lead to a margin call? If you enter a short futures contract, what futures price will lead to a margin call? 1.b. What happens if you do not meet a margin call? 1.c. Suppose you buy a December gold futures at $500, on July 1st. You hold the position until selling on July 16th at $485.50. The daily prices on the intervening days are as shown in the table below. Complete the table below on gains/losses and charges/credits to the margin account. Day 1-Jul 2-Jul 3-Jul 4-Jul 5-Jul 6-Jul 7-Jul 8-Jul 9-Jul 10-Jul 11-Jul 12-Jul 13-Jul 14-Jul 15-Jul 16-Jul Futures Price 500.00 501.50 502.00 493.60 491.70 492.90 488.90 494.20 488.40 482.30 478.70 478.30 482.40 475.50 480.30 485.50 Daily Gain/Loss ($) Cumulative Gain/Loss ($) Margin Account Balance ($) Margin Call ($) 1.d. Suppose at July 1st you hold 100,000 ounces of gold. At present, the gold spot price is $480. You wish to hedge the gold price risk using the December gold futures contract described above. - 1.d.1. What position should you take on the futures contract? 1.d.2. What is the basis on July 1st? Calculate the profit/loss from a hedge if it is held to expiration and the basis converges to zero. 1.d.3. Suppose you close the hedge early on July 16th (at F=485.50) and the gold spot price at that point is $487. What is the profit/loss from the hedge?

Expert Answer:

Answer rating: 100% (QA)

1a In a long futures contract to buy December gold for 500 per ounce a margin call will occur if the futures price decreases The amount of decrease th... View the full answer

Related Book For

Intermediate Accounting

ISBN: 978-0470161012

9th Canadian Edition, Volume 2

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield.

Posted Date:

Students also viewed these finance questions

-

If you could model yourself after one or more of the historical leaders we discussed in this chapter, whom would you model yourself after? Please learn more about the leader you chose. Identify two...

-

If you were the sixth member of this team, what kinds of communication might you enact to help relieve tension in the group

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Discuss the different sampling procedures and techniques that you will apply to the qualitative and quantitative phases of the study.

-

Two cross-country running teams participated in a (hypothetical) study in which a fraction of each team used weight training to supplement a running workout. The remaining runners did not use weight...

-

Kent Duncan is exploring the possibility of opening a self-service car wash and operating it for the next five years until he retires. He has gathered the following information: a. A building in...

-

2. Agency funds maintain accounts for: a Liabilities b Revenues c Net position d Expenditures

-

For each of the following accounts, indicate the effect of a debit or a credit on the account and the normal balance. (a) Accounts Payable. (b) Advertising Expense. (c) Service Revenue. (d) Accounts...

-

Connection to Practice: Final Assessment Case Study-Connecting the Dots: 100 points\ This case study counts towards 40% of your final assessment grade (the final assessment is 10% of your\ total...

-

Pharaoh company obtains $44,800 in cash by signing a 7%, 6 month, $44,800 note payable to First Bank on July 1. Pharoah's fiscal year ends on September 30. What information should be reported for the...

-

Buzz's Educational Software Outlet sells two or more of the video games as a single package, Managers are keenly interested in individual product - profitability figures. Information pertaining to...

-

Find the explained variation for the paired data. The equation of the regression line for the paired data below is y = 5.18286 + 3.33937x. X 972 23 34 4 22 17 y 43 35 16 21 23 102 81

-

5. The vertical stress at a point is 28 kPa, while the horizontal stress is 14 kPa. shear stress on the horizontal plane is +4 kPa. The (a) Draw the Mohr's circle of stress and show the pole point...

-

I need assistance with the below questions for my HIM 5370 at texas State University Case Mix Table: 4. Complete the Case Mix table shown below. Calculate the case mix for each month. The table below...

-

The probability that a printing press will print a book with no errors is 78%. The company is about to process an order of 30 books. Round decimals to 3 places or percentages to 1 decimal place. 9....

-

alculate Product Costs, using JOB COSTING SYSTEM. Please SHOW CALCULATION. Dream Chocolate Company: Choosing a Costing System TABLE 1 Typical Prices and Costs of Chocolate 641 1.25 oz. Bar 3.0 oz....

-

The William B. Waugh Corporation is a regional Toyota dealer. The firm sells new and used trucks and is actively involved in the parts business. During the most recent year, the company generated...

-

The May 2014 revenue and cost information for Houston Outfitters, Inc. follow: Sales Revenue (at standard).............. $ 540,000 Cost of Goods Sold (at standard) ..........341,000 Direct Materials...

-

Tercek Inc., which uses accounting standards for private enterprises (ASPE), had the following balances and amounts appear on its comparative financial statements at year end: Calculate the amount...

-

The following accounts appear in the ledger of Samson Inc. Samsons shares trade on the Toronto and New York stock exchanges and so the company uses IFRS. Samson made a special election to account for...

-

Grenier Limited issued $300,000 of 10% bonds on January 1, 2011. The bonds are due on January 1, 2016, with interest payable each July 1 and January 1. The bonds are issued at face value. Prepare the...

-

19. What are the two fund-based financial statements for governmental funds? What information does each normally present?

-

18. What are the two government-wide financial statements? What does each normally present?

-

22. How are internal service funds reported on government-wide financial statements?

Study smarter with the SolutionInn App