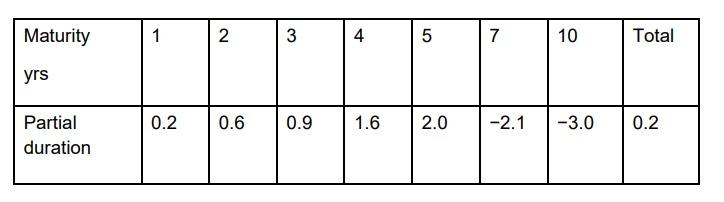

Question: 1. Consider the partial durations as from the Table 1 below and: a) Estimate the effect of a shift in the yield curve where the

1. Consider the partial durations as from the Table 1 below and:

a) Estimate the effect of a shift in the yield curve where the ten-year rate stays the same, the one-year rate moves up by 9e, and the movements in intermediate rates are calculated by interpolation between 9e and 0. (20 marks)

b) Estimate the percentage change in the portfolio value arising from the rotation? (10 marks)

Maturity yrs Partial duration 1 0.2 2 0.6 3 4 0.9 1.6 5 2.0 7 -2.1 Total 10 -3.0 0.2 Maturity yrs Partial duration 1 0.2 2 0.6 3 4 0.9 1.6 5 2.0 7 -2.1 Total 10 -3.0 0.2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock