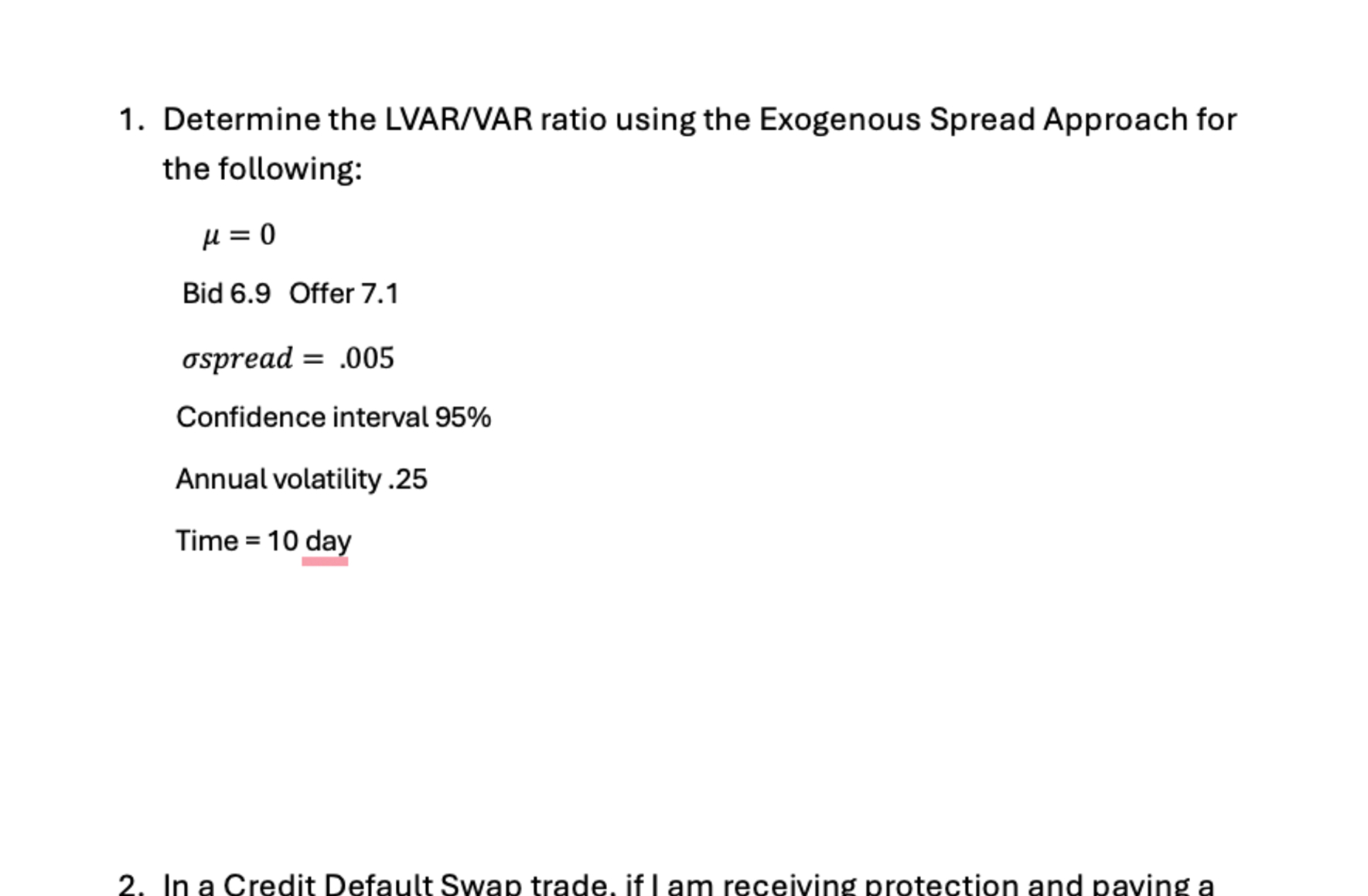

Question: 1 . Determine the LVAR / VAR ratio using the Exogenous Spread Approach for the following: [ mu = 0 ] Bid

Determine the LVARVAR ratio using the Exogenous Spread Approach for the following: mu Bid Offer ospread Confidence interval Annual volatility Time day In a Credit Default Swap trade. if I am receiving protection and paving a

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock