Question: 1. Forward on Zero Coupon Bond Consider a 1-year forward contract on a zero coupon bond with 3-year maturity. The face value of the bond

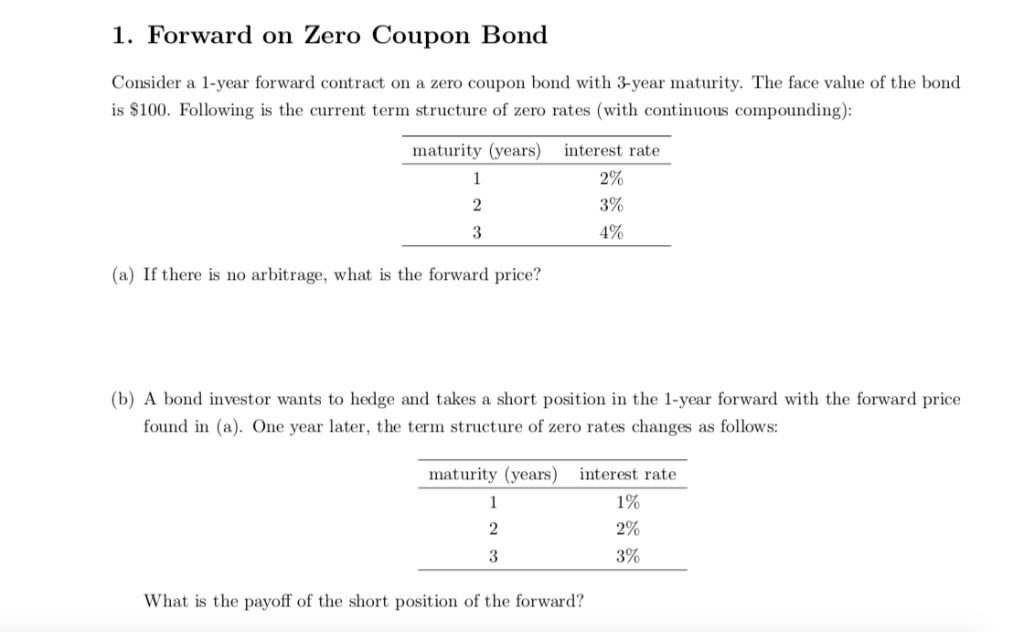

1. Forward on Zero Coupon Bond Consider a 1-year forward contract on a zero coupon bond with 3-year maturity. The face value of the bond is $100. Following is the current term structure of zero rates (with continuous compounding): maturity (years) nterest rate 2% 3% 4% (a) If there is no arbitrage, what is the forward price? (b) A bond investor wants to hedge and takes a short position in the 1-year forward with the forward price found in (a). One year later, the term structure of zero rates changes as follows maturity (years) interest rate 1% 2% 3% What is the payoff of the short position of the forward

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock