Question: 1. Forwards and Swaps ( The current yield curve (in years): Time Ti 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 r(0,Ti)

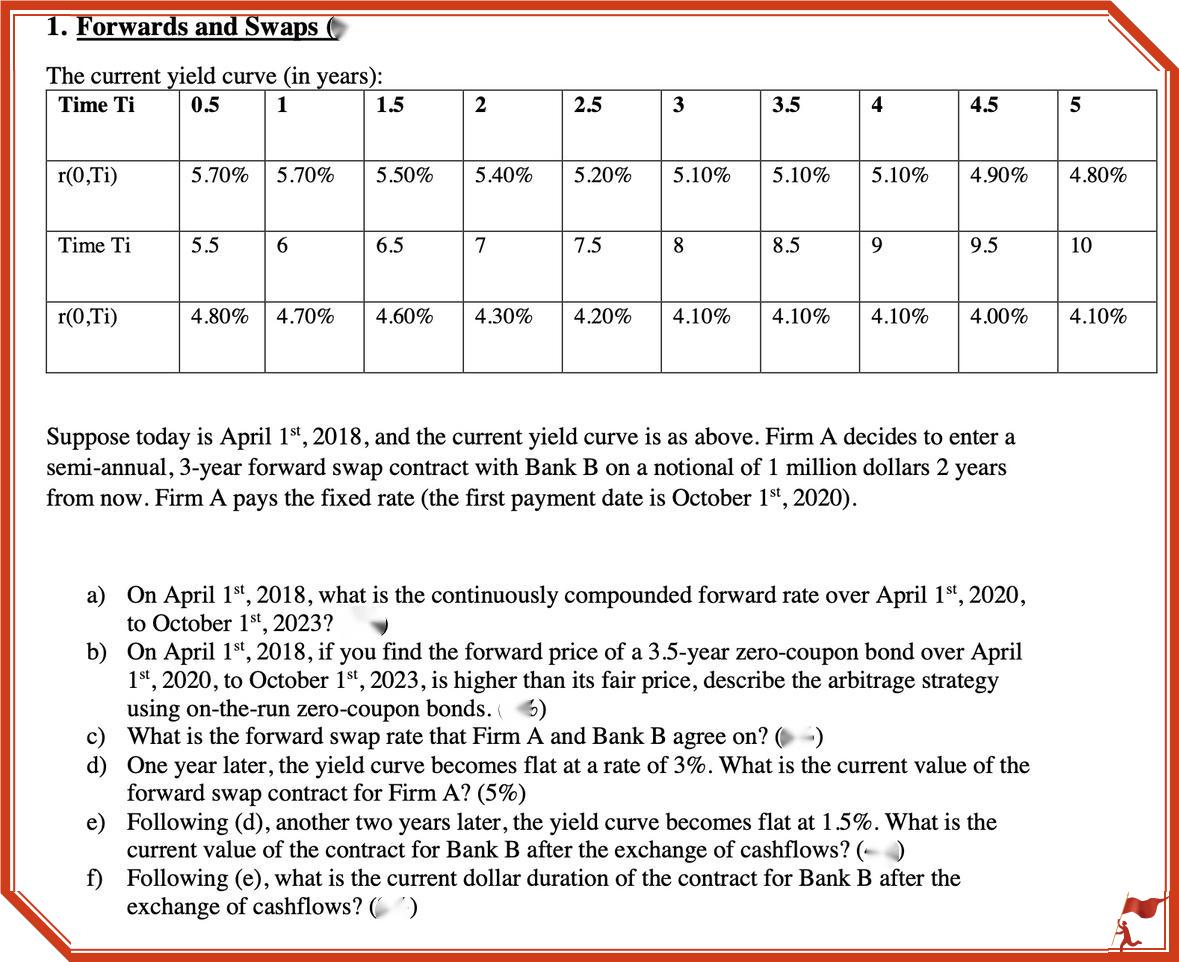

1. Forwards and Swaps ( The current yield curve (in years): Time Ti 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 r(0,Ti) 5.70% 5.70% 5.50% 5.40% 5.20% 5.10% 5.10% 5.10% 4.90% 4.80% Time Ti 5.5 6 6.5 7 7.5 8 8.5 9 9.5 10 r(0,Ti) 4.80% 4.70% 4.60% 4.30% 4.20% 4.10% 4.10% 4.10% 4.00% 4.10% Suppose today is April 1st, 2018, and the current yield curve is as above. Firm A decides to enter a semi-annual, 3-year forward swap contract with Bank B on a notional of 1 million dollars 2 years from now. Firm A pays the fixed rate (the first payment date is October 1st, 2020). a) On April 1st, 2018, what is the continuously compounded forward rate over April 1st, 2020, to October 1st, 2023? b) On April 1st, 2018, if you find the forward price of a 3.5-year zero-coupon bond over April 1st, 2020, to October 1st, 2023, is higher than its fair price, describe the arbitrage strategy using on-the-run zero-coupon bonds. (5) c) What is the forward swap rate that Firm A and Bank B agree on? (-) d) One year later, the yield curve becomes flat at a rate of 3%. What is the current value of the forward swap contract for Firm A? (5%) e) Following (d), another two years later, the yield curve becomes flat at 1.5%. What is the current value of the contract for Bank B after the exchange of cashflows? ( ) f) Following (e), what is the current dollar duration of the contract for Bank B after the exchange of cashflows? ( )

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts