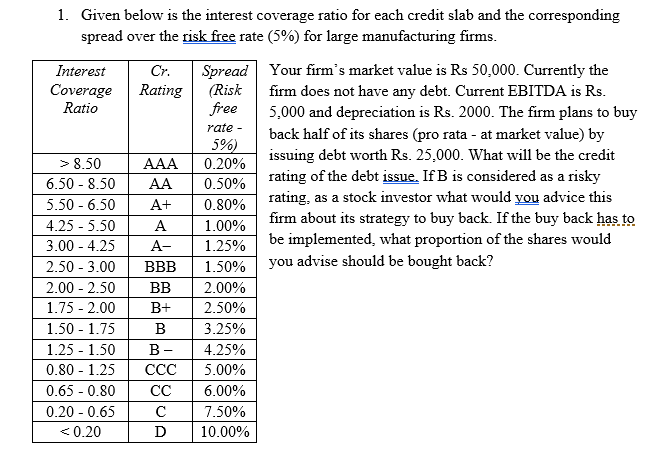

Question: 1. Given below is the interest coverage ratio for each credit slab and the corresponding spread over the risk free rate (5%) for large manufacturing

1. Given below is the interest coverage ratio for each credit slab and the corresponding spread over the risk free rate (5%) for large manufacturing firms. Interest Cr. Spread Your firm's market value is Rs 50,000. Currently the Coverage Rating (Risk firm does not have any debt. Current EBITDA is Rs. Ratio free 5.000 and depreciation is Rs. 2000. The firm plans to buy rate back half of its shares (pro rata - at market value) by 5%) > 8.50 issuing debt worth Rs. 25,000. What will be the credit AAA 0.20% 6.50 -8.50 AA 0.50% rating of the debt issue. If B is considered as a risky 5.50 -6.50 A+ 0.80% rating, as a stock investor what would you advice this 4.25 -5.50 A 1.00% firm about its strategy to buy back. If the buy back has to 3.00 -4.25 A- 1.25% be implemented, what proportion of the shares would 2.50 -3.00 BBB 1.50% you advise should be bought back? 2.00 -2.50 BB 2.00% 1.75 -2.00 B+ 2.50% 1.50 -1.75 B 3.25% 1.25 -1.50 B- 4.25% 0.80 - 1.25 5.00% 0.65 -0.80 6.00% 0.20 -0.65 7.50%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts