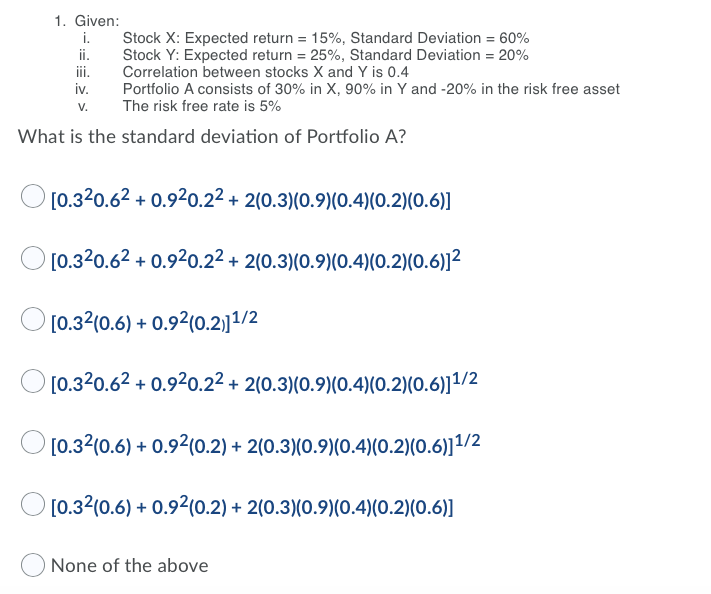

Question: 1. Given: i. Stock X: Expected return = 15%, Standard Deviation = 60% ii. Stock Y: Expected return = 25%, Standard Deviation = 20% iii.

1. Given: i. Stock X: Expected return = 15%, Standard Deviation = 60% ii. Stock Y: Expected return = 25%, Standard Deviation = 20% iii. Correlation between stocks X and Y is 0.4 iv. Portfolio A consists of 30% in X, 90% in Y and -20% in the risk free asset V. The risk free rate is 5% What is the standard deviation of Portfolio A? O [0.320.62 +0.920.22 + 2(0.3)(0.9)(0.4)(0.2)(0.6)] O [0.320.62 +0.920.22 + 2(0.3)(0.9)(0.4)(0.2)(0.6)]2 [0.32(0.6) + 0.92(0.2)]1/2 [0.320.62 + 0.920.22 + 2(0.3)(0.9)(0.4)(0.2)(0.6)]1/2 [0.32(0.6) +0.92(0.2) + 2(0.3)(0.9)(0.4)(0.2)(0.6)]1/2 [0.32(0.6) + 0.92(0.2) + 2(0.3)(0.9)(0.4)(0.2)(0.6)] None of the above

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock