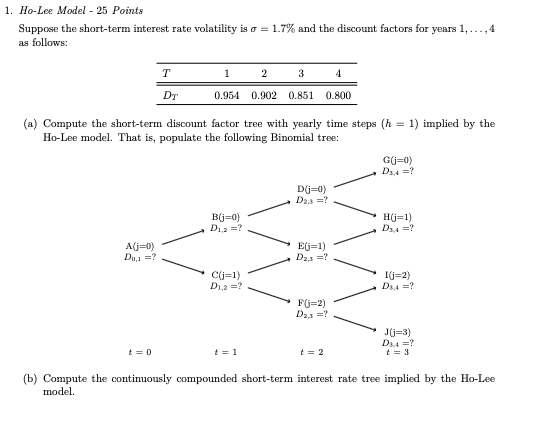

Question: 1. Ho-Lee Model - 25 Points Suppose the short-term interest rate volatility is o = 1.7% and the discount factors for years 1,..., 4 as

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock