Question: 1. Let 0 be the random variable of the future loss for a fully continuous whole life insurance on an individual age 60. You are

1. Let 0 be the random variable of the future loss for a fully continuous whole life insurance on an individual age 60. You are given the follow: (i) = 0.03 (ii) Mortality follows = 100 , 0 100. (iii) 60 = 0.45 2 (iv) Premiums are determined by the equivalence principles. Calculate [ 0].

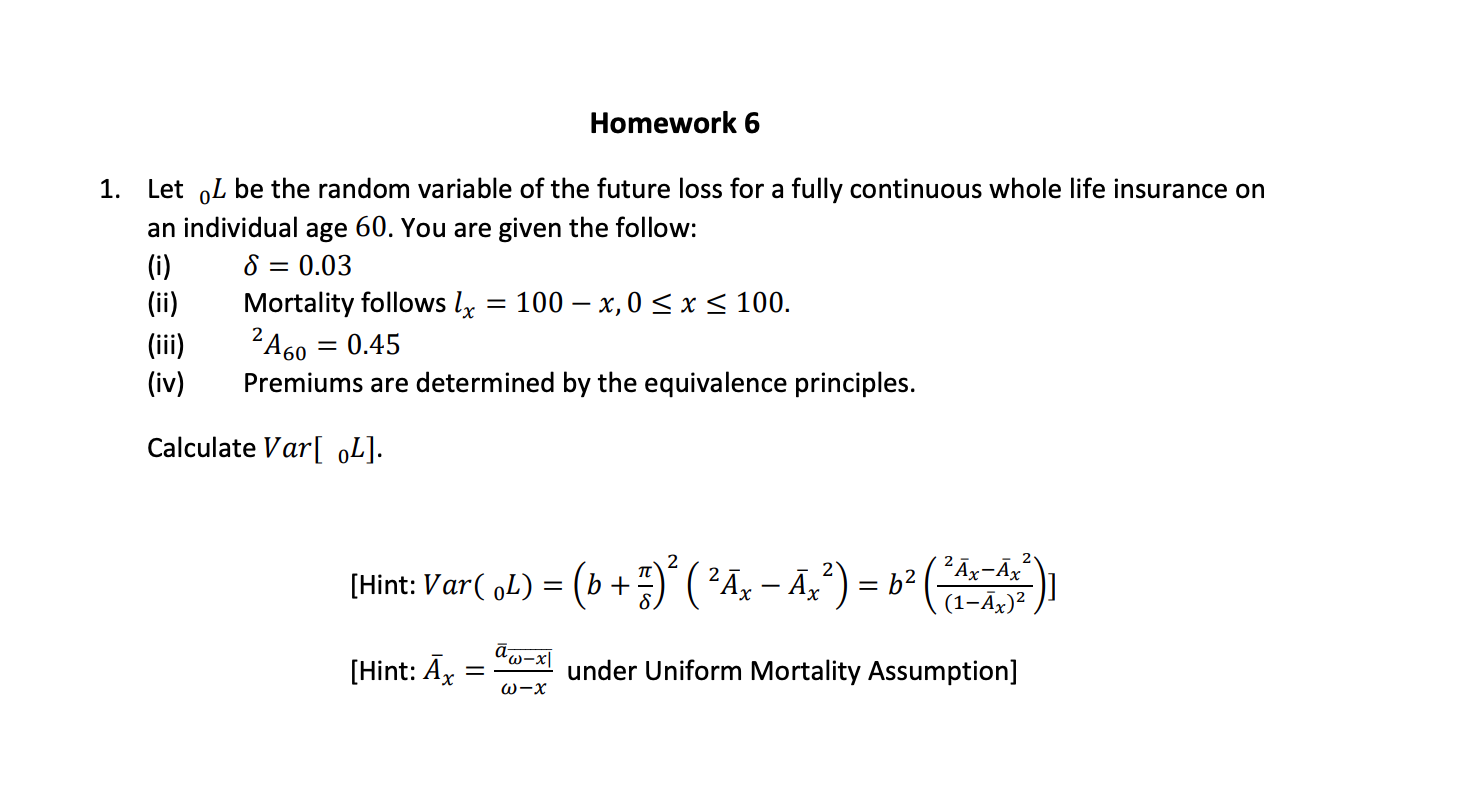

Homework 6 1. Let 0L be the random variable of the future loss for a fully continuous whole life insurance on an individual age 60. You are given the follow: (i) 6 = 0.03 (ii) Mortality follows lx = 100 - x. 0 S x S 100. (iii) 2A60 = 0.45 (iv) Premiums are determined by the equivalence principles. Calculate Var[ 0L]. [Hintz Var( OL) = (b + 32 ( 25x - 3x2) = 1'2 (:f_:):)1 acux wx [Hint: Ax = under Uniform Mortality Assumption]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts