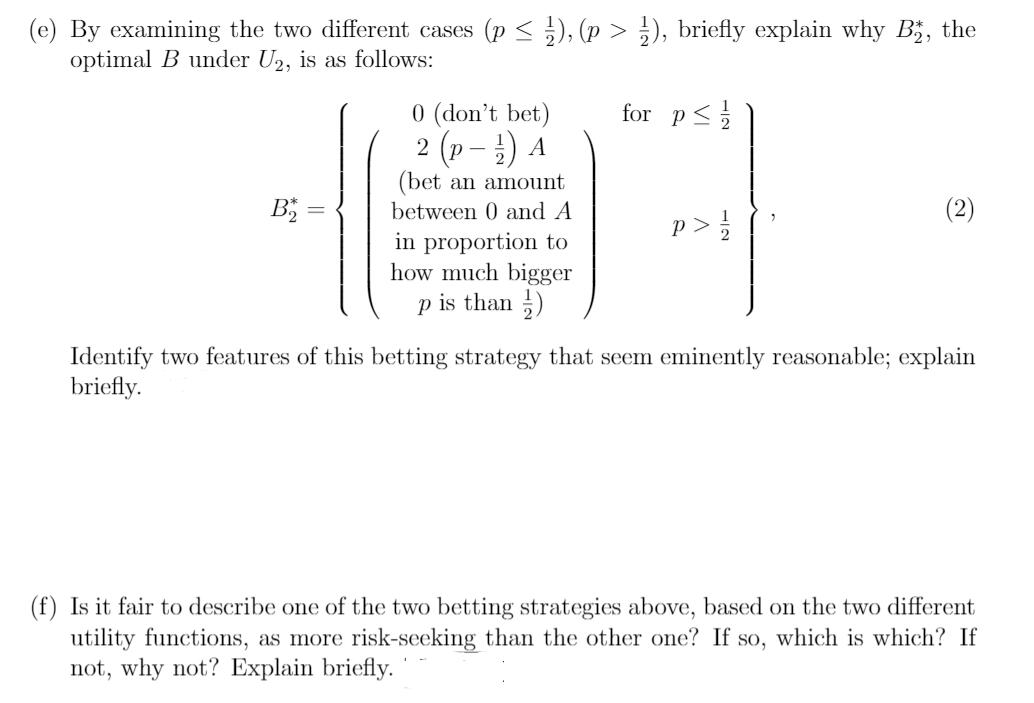

Question: ((1) Now let's suppose instead that you use Daniel Bernoulli's utility function U2 (:3) = 1 + log(:r). (i) Work out your expected utility E[U2(X}]

![utility E[U2(X}] as a function of A, B and p. Take A](https://s3.amazonaws.com/si.experts.images/answers/2024/06/6678637f8b6e0_8236678637f706f9.jpg)

((1) Now let's suppose instead that you use Daniel Bernoulli's utility function U2 (:3) = 1 + log(:r). (i) Work out your expected utility E[U2(X}] as a function of A, B and p. Take A = 10 for illustration and get Wolfram Alpha (or some other equivalent envi- ronment) to plot this as a function of B from 5 to A for two different values of p: 0.4 and 0.7; reproduce these plots in your solutions, either electronically or by hand-sketching what your software environment showed you. Holding A > U and 0 i , briey explain why 3*, the 2 2 2 optimal B under U2, is as follows: 0 (don't bet) for p 5 % 2 (p i) A (bet an amount B; = between 0 and A 1 a (2) i" > a in proportion to how much bigger p is than %) Identify two ft-zaturt-zs of this betting strategy that seem eminently reasonable; explain briey. (f) Ls it fair to describe one of the two betting strategies above, base-3d on the two different. utility functions, as more risk-seeking than the other one? If so, which is which? If not, why not? Explain briey. ' ' ' Someone offers you the possibility to play a gambling game with the following rules. First, you decide how much money you're willing to put at risk in this game: this amount let's call it A > 0 is referred to as your stoke (all the monetary quantities are in dollars in this problem); think of A as a xed known positive real number in what follows. Having chosen your stake, you're allowed to bet any amount 0 g: B g A (thus, as a decision problem, your possible actions in this situation correspond to values of B). If you win the bet, which occurs with probability 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts