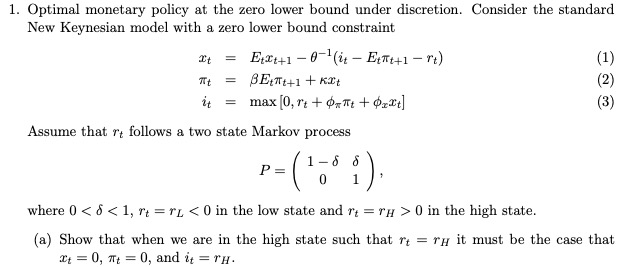

Question: 1. Optimal monetary policy at the zero lower bound under discretion. Consider the standard New Keynesian model with a zero lower bound constraint D =

1. Optimal monetary policy at the zero lower bound under discretion. Consider the standard New Keynesian model with a zero lower bound constraint D = Etrt-0-(it - Eint+1 - it) = BETit1 + Kit it = max [0, r + dont + dart] Assume that t follows a two state Markov process 1 -6 6 P = 0 1 where 0 0 in the high state. (a) Show that when we are in the high state such that re = ry it must be the case that It = 0, at = 0, and it = TH

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock