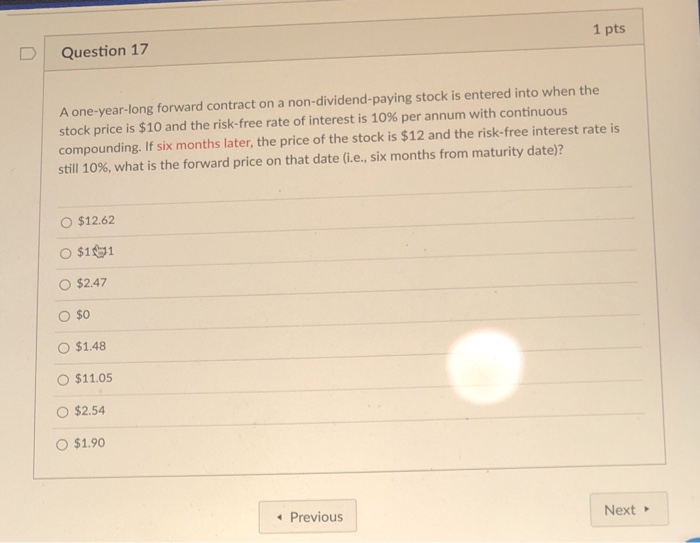

Question: 1 pts Question 17 A one-year-long forward contract on a non-dividend-paying stock is entered into when the stock price is $10 and the risk-free rate

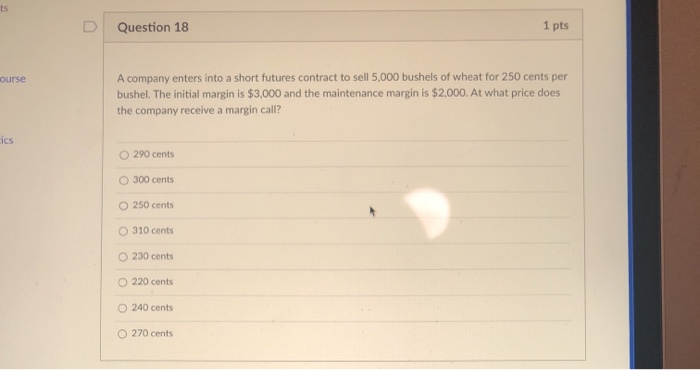

1 pts Question 17 A one-year-long forward contract on a non-dividend-paying stock is entered into when the stock price is $10 and the risk-free rate of interest is 10% per annum with continuous compounding. If six months later, the price of the stock is $12 and the risk-free interest rate is still 10%, what is the forward price on that date (i.e., six months from maturity date)? O $12.62 O $11 $2.47 $0 O $1.48 O $11.05 O $2.54 $1.90 Previous Next > ts Question 18 1 pts ourse A company enters into a short futures contract to sell 5,000 bushels of wheat for 250 cents per bushel. The initial margin is $3,000 and the maintenance margin is $2,000. At what price does the company receive a margin call? ics 290 cents O 300 cents O 250 cents O 310 cents 230 cents 220 cents O 240 cents 270 cents

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts