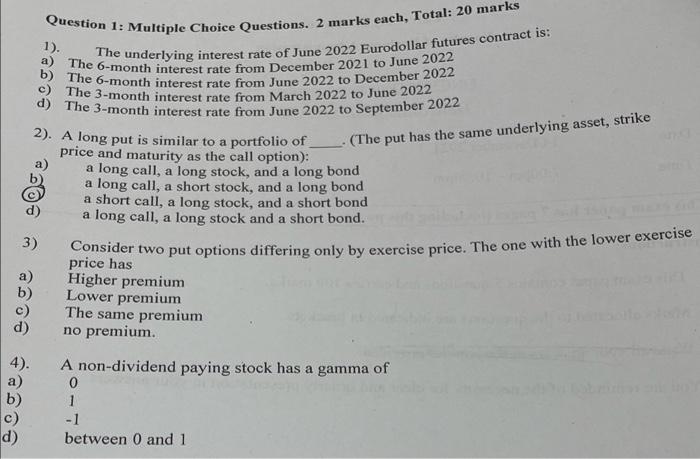

Question: 1). Question 1: Multiple Choice Questions. 2 marks each, Total: 20 marks a) The 6-month interest rate from December 2021 to June 2022 The underlying

1). Question 1: Multiple Choice Questions. 2 marks each, Total: 20 marks a) The 6-month interest rate from December 2021 to June 2022 The underlying interest rate of June 2022 Eurodollar futures contract is: b) The 6-month interest rate from June 2022 to December 2022 c) The 3-month interest rate from March 2022 to June 2022 d) The 3-month interest rate from June 2022 to September 2022 (The put has the same underlying asset, strike coce coce w ene es 2). A long put is similar to a portfolio of price and maturity as the call option): a) a long call, a long stock, and a long bond a long call, a short stock, and a long bond a short call, a long stock, and a short bond a long call, a long stock and a short bond. Consider two put options differing only by exercise price. The one with the lower exercise Higher premium Lower premium The same premium no premium. 4). A non-dividend paying stock has a gamma of 0 1 -1 between 0 and 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts