Question: 1. Return Analysis (20 points) Use the provided data to answer the following questions. a. Calculate the period capital gain rate, dividend Date A HARMAAN

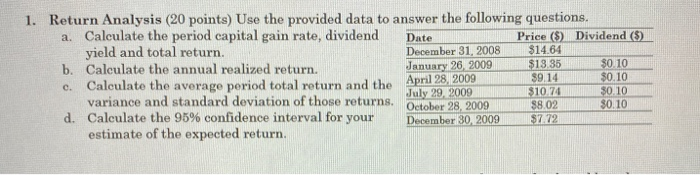

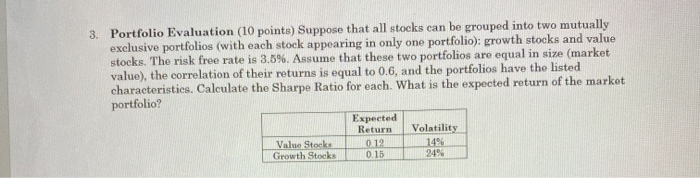

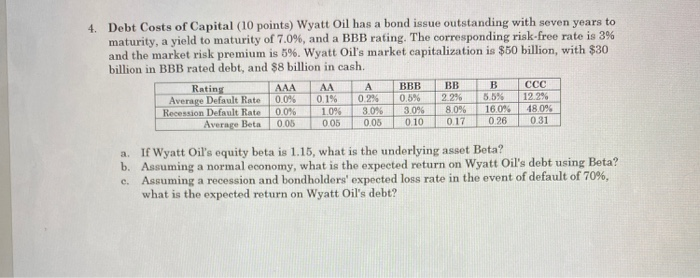

1. Return Analysis (20 points) Use the provided data to answer the following questions. a. Calculate the period capital gain rate, dividend Date A HARMAAN Price ($) Dividend (5) yield and total return. December 31, 2008 $14.64 b. Calculate the annual realized return. January 26, 2009 $13.35 $0.10 $9.14 $0.10 c. Calculate the average period total return and the July 29, 2009 $10.74 $0.10 variance and standard deviation of those returns. O ber 28, 2009 $8.02 $0.10 d. Calculate the 95% confidence interval for your December 30, 2009 $7.72 estimate of the expected return. 2. Portfolio Analysis (10 points) You are presently invested in the Luther Fund, a broad based mutual fund that invests in stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of 20 with the Luther Fund. Will adding the precious metals fund improve your portfolio? 3. Portfolio Evaluation (10 points) Suppose that all stocks can be grouped into two mutually exelusive portfolios (with each stock appearing in only one portfolio): growth stocks and value stocks. The risk free rate is 3.5%. Assume that these two portfolios are equal in size (market value), the correlation of their returns is equal to 0.6, and the portfolios have the listed characteristics. Calculate the Sharpe Ratio for each. What is the expected return of the market portfolio? Expected Return Volatility Value Stock 1012 14% 249 Growth Stock 015 4. Debt Costs of Capital (10 points) Wyatt Oil has a bond issue outstanding with seven years to maturity, a yield to maturity of 7.0%, and a BBB rating. The corresponding risk-free rate is 3% and the market risk premium is 5%. Wyatt Oil's market capitalization is $50 billion, with $30 billion in BBB rated debt, and $8 billion in cash. RatingAAAAAABBBBB B Average Default Rate 009 10.1% 0.2% 0.5% 2.2% 5.5% Recession Default Rate 0.09 10 30 30 8.0 16.0 Average Beta 0.05 0.05 0.05 0.10 0.17 0.26 CCC 12.2% 4800 031 a. If Wyatt Oil's equity beta is 1.15, what is the underlying asset Beta? b. Assuming a normal economy, what is the expected return on Wyatt Oil's debt using Beta? e. Assuming a recession and bondholders' expected loss rate in the event of default of 70%, what is the expected return on Wyatt Oil's debt? 1. Return Analysis (20 points) Use the provided data to answer the following questions. a. Calculate the period capital gain rate, dividend Date A HARMAAN Price ($) Dividend (5) yield and total return. December 31, 2008 $14.64 b. Calculate the annual realized return. January 26, 2009 $13.35 $0.10 $9.14 $0.10 c. Calculate the average period total return and the July 29, 2009 $10.74 $0.10 variance and standard deviation of those returns. O ber 28, 2009 $8.02 $0.10 d. Calculate the 95% confidence interval for your December 30, 2009 $7.72 estimate of the expected return. 2. Portfolio Analysis (10 points) You are presently invested in the Luther Fund, a broad based mutual fund that invests in stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of 20 with the Luther Fund. Will adding the precious metals fund improve your portfolio? 3. Portfolio Evaluation (10 points) Suppose that all stocks can be grouped into two mutually exelusive portfolios (with each stock appearing in only one portfolio): growth stocks and value stocks. The risk free rate is 3.5%. Assume that these two portfolios are equal in size (market value), the correlation of their returns is equal to 0.6, and the portfolios have the listed characteristics. Calculate the Sharpe Ratio for each. What is the expected return of the market portfolio? Expected Return Volatility Value Stock 1012 14% 249 Growth Stock 015 4. Debt Costs of Capital (10 points) Wyatt Oil has a bond issue outstanding with seven years to maturity, a yield to maturity of 7.0%, and a BBB rating. The corresponding risk-free rate is 3% and the market risk premium is 5%. Wyatt Oil's market capitalization is $50 billion, with $30 billion in BBB rated debt, and $8 billion in cash. RatingAAAAAABBBBB B Average Default Rate 009 10.1% 0.2% 0.5% 2.2% 5.5% Recession Default Rate 0.09 10 30 30 8.0 16.0 Average Beta 0.05 0.05 0.05 0.10 0.17 0.26 CCC 12.2% 4800 031 a. If Wyatt Oil's equity beta is 1.15, what is the underlying asset Beta? b. Assuming a normal economy, what is the expected return on Wyatt Oil's debt using Beta? e. Assuming a recession and bondholders' expected loss rate in the event of default of 70%, what is the expected return on Wyatt Oil's debt

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts