Question: 1. The file entitled SIM 2.xls contains the simulated data sets used in this chapter. The first series, denoted Y1, contains the 100 values of

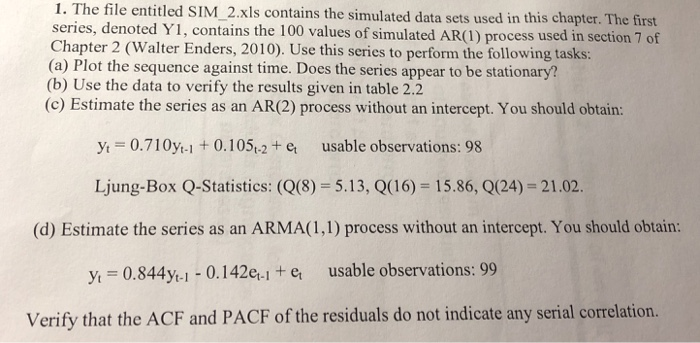

1. The file entitled SIM 2.xls contains the simulated data sets used in this chapter. The first series, denoted Y1, contains the 100 values of simulated AR(1) process used in section 7 of Chapter 2 (Walter Enders, 2010). Use this series to perform the following tasks: (a) Plot the sequence against time. Does the series appear to be stationary? (b) Use the data to verify the results given in table 2.2 (c) Estimate the series as an AR(2) process without an intercept. You should obtain: y 0.710y-1 0.105t-2+ e usable observations: 98 Ljung-Box Q-Statistics: (Q(8) 5.13, Q(16) 15.86, Q(24) 21.02. (d) Estimate the series as an ARMA(1,1) process without an intercept. You should obtain: y 0.844y1- 0.142ee usable observations: 99 Verify that the ACF and PACF of the residuals do not indicate any serial correlation. 1. The file entitled SIM 2.xls contains the simulated data sets used in this chapter. The first series, denoted Y1, contains the 100 values of simulated AR(1) process used in section 7 of Chapter 2 (Walter Enders, 2010). Use this series to perform the following tasks: (a) Plot the sequence against time. Does the series appear to be stationary? (b) Use the data to verify the results given in table 2.2 (c) Estimate the series as an AR(2) process without an intercept. You should obtain: y 0.710y-1 0.105t-2+ e usable observations: 98 Ljung-Box Q-Statistics: (Q(8) 5.13, Q(16) 15.86, Q(24) 21.02. (d) Estimate the series as an ARMA(1,1) process without an intercept. You should obtain: y 0.844y1- 0.142ee usable observations: 99 Verify that the ACF and PACF of the residuals do not indicate any serial correlation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts