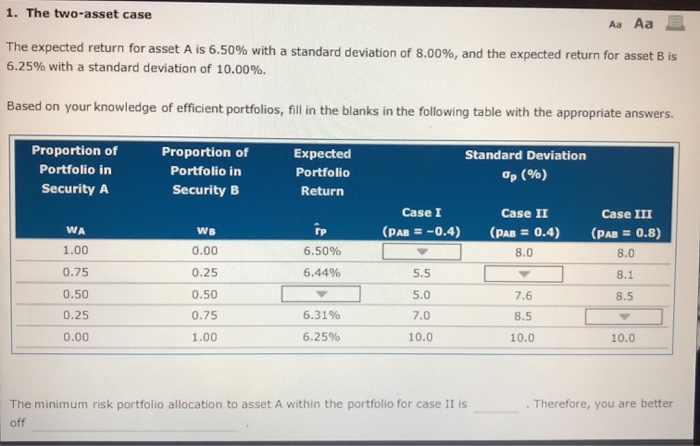

Question: 1. The two-asset case Aa Aa The expected return for asset A is 6.50% with a standard deviation of 8.00%, and the expected return for

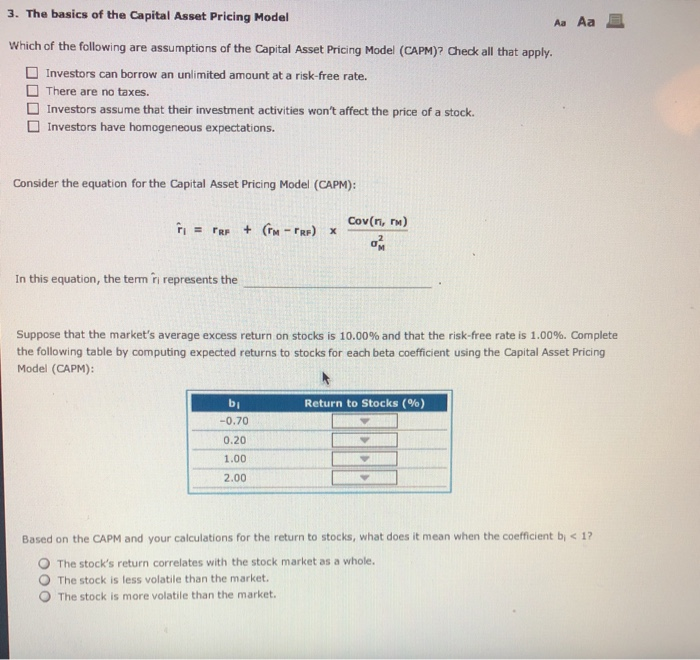

1. The two-asset case Aa Aa The expected return for asset A is 6.50% with a standard deviation of 8.00%, and the expected return for asset B is 6.25% with a standard deviation of 10.00%. Based on your knowledge of efficient portfolios, fill in the blanks in the following table with the appropriate answers. Standard Deviation Proportion of Portfolio in Security A Proportion of Portfolio in Security B Expected Portfolio Return Op (%) Case I (PAB = -0.4) WA 1.00 WB 0.00 6.50% Case II (PAB = 0.4) 8.0 Case III (PAB = 0.8) 8.0 0.75 0.25 6.44% 5.5 8.1 5.0 7.6 8.5 0.50 0.25 0.50 0.75 6.31% 7.0 8.5 0.00 1.00 6.25% 10.0 10.0 10.0 Therefore, you are better The minimum risk portfolio allocation to asset A within the portfolio for case II is off Aa Aa 3. The basics of the Capital Asset Pricing Model Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. Investors can borrow an unlimited amount at a risk-free rate. There are no taxes. Investors assume that their investment activities won't affect the price of a stock. Investors have homogeneous expectations. Consider the equation for the Capital Asset Pricing Model (CAPM): Cov(n,r) = re + CM - TRE) In this equation, the term in represents the Suppose that the market's average excess return on stocks is 10.00% and that the risk-free rate is 1.00%. Complete the following table by computing expected returns to stocks for each beta coefficient using the Capital Asset Pricing Model (CAPM): Return to Stocks (%) bi -0.70 0.20 1.00 2.00 Based on the CAPM and your calculations for the return to stocks, what does it mean when the coefficient b

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts