Question: 1. There are two mutual funds, A and B with the following information, where i is the standard deviation, and i,m is the correlation with

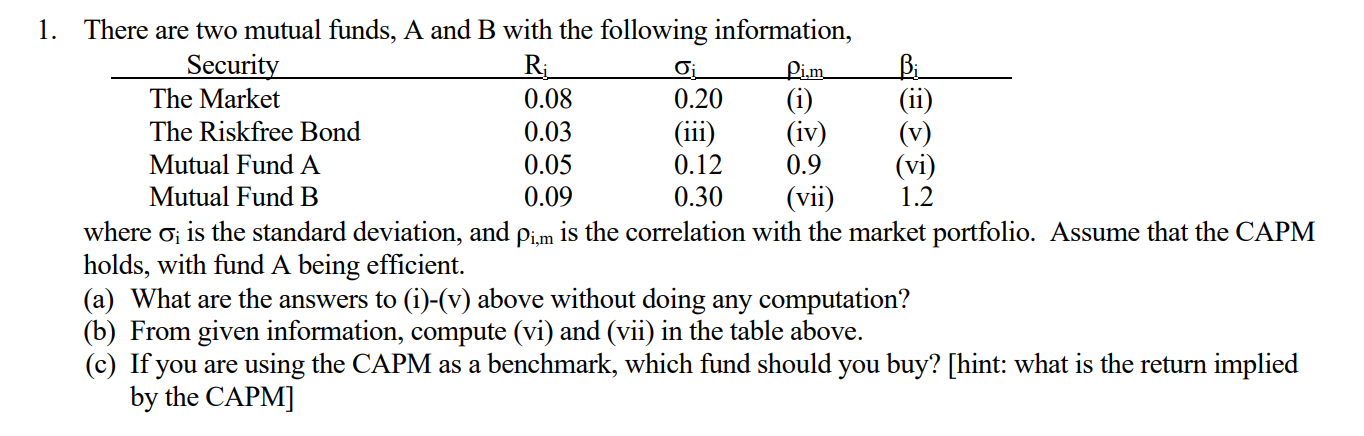

1. There are two mutual funds, A and B with the following information, where i is the standard deviation, and i,m is the correlation with the market portfolio. Assume that the CAPM holds, with fund A being efficient. (a) What are the answers to (i)-(v) above without doing any computation? (b) From given information, compute (vi) and (vii) in the table above. (c) If you are using the CAPM as a benchmark, which fund should you buy? [hint: what is the return implied by the CAPM] 1. There are two mutual funds, A and B with the following information, where i is the standard deviation, and i,m is the correlation with the market portfolio. Assume that the CAPM holds, with fund A being efficient. (a) What are the answers to (i)-(v) above without doing any computation? (b) From given information, compute (vi) and (vii) in the table above. (c) If you are using the CAPM as a benchmark, which fund should you buy? [hint: what is the return implied by the CAPM]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts