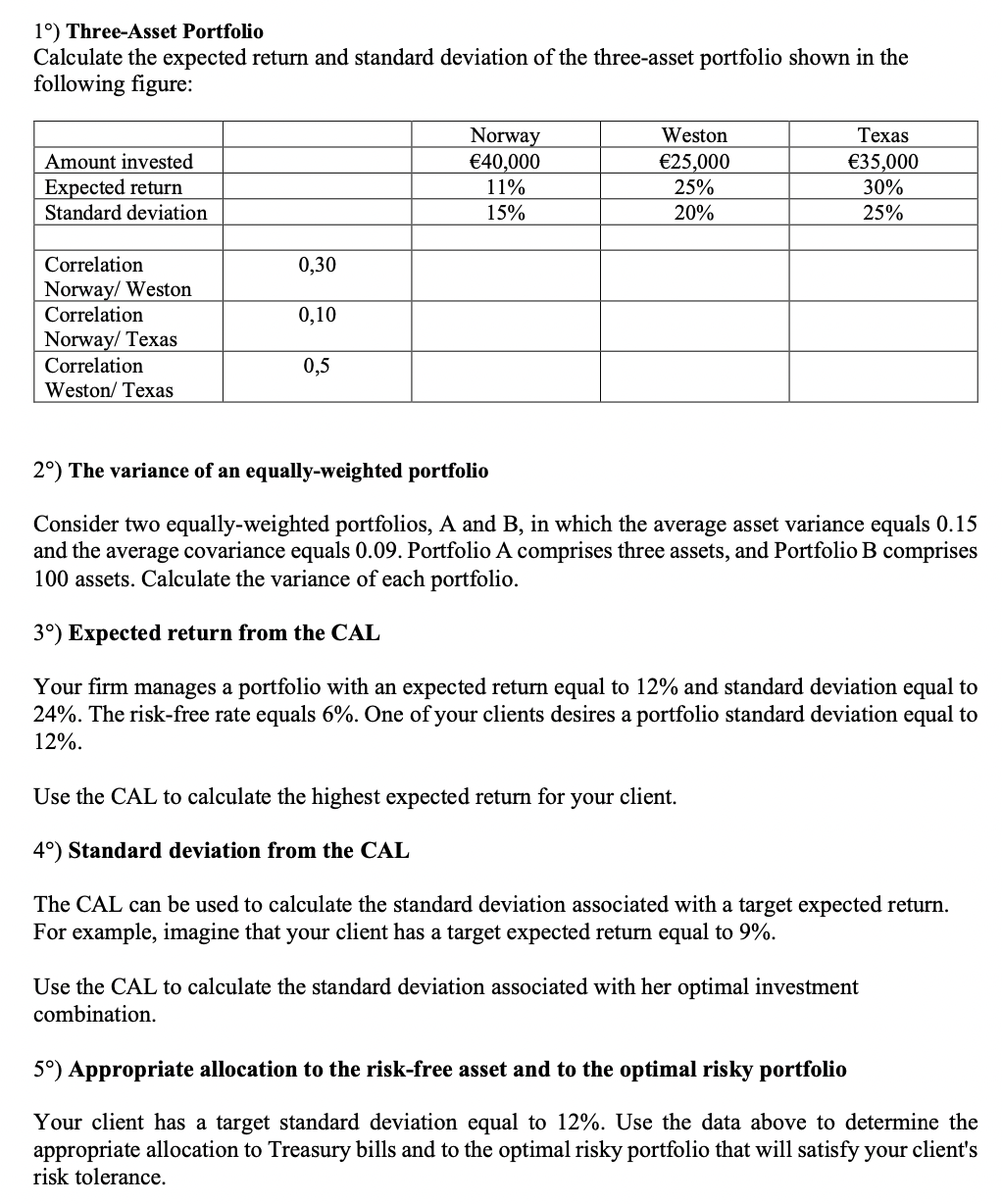

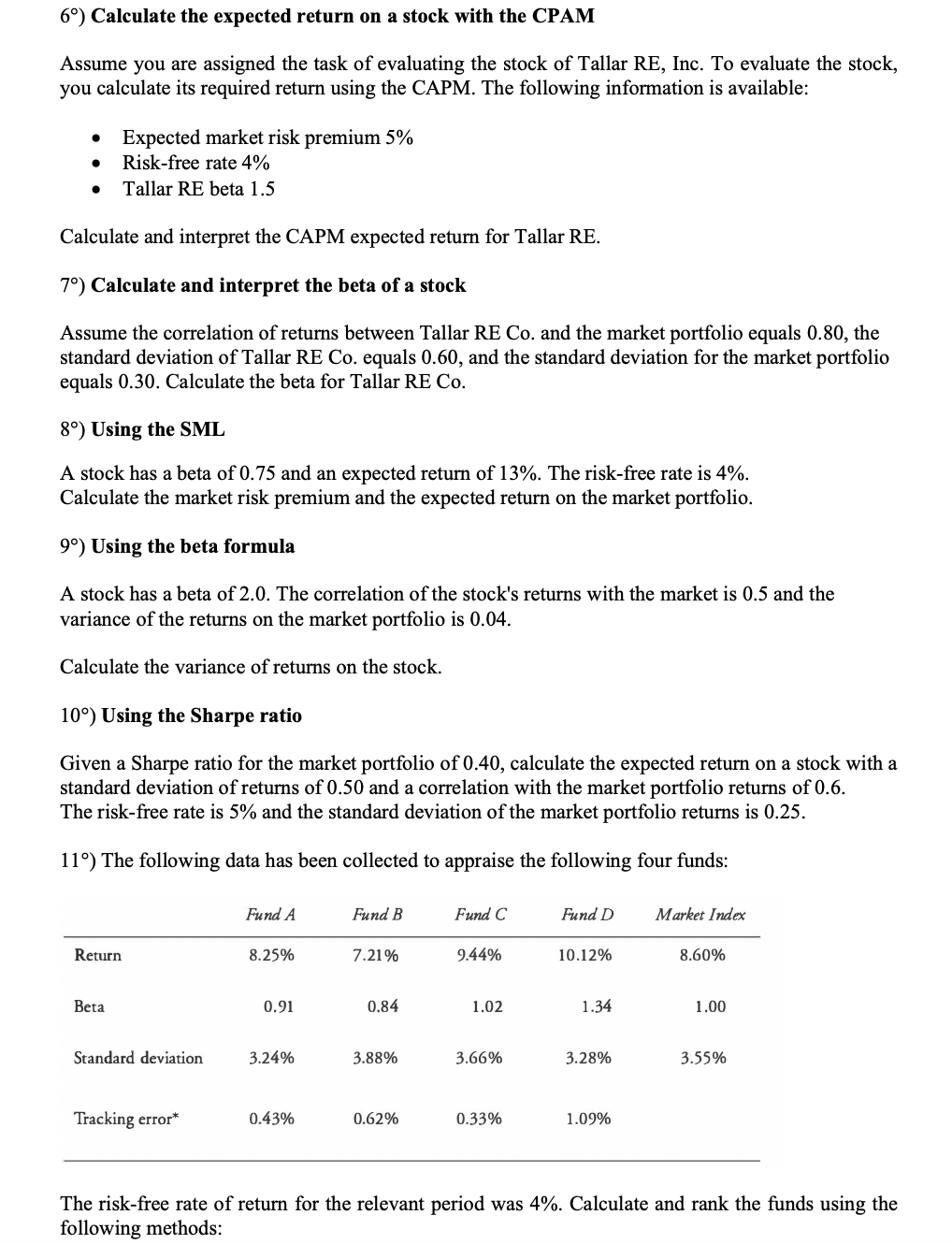

1) Three-Asset Portfolio Calculate the expected return and standard deviation of the three-asset portfolio shown in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

1 ThreeAsset Portfolio Expected return of the portfolio Weight Expected return 40000100000 11 25000100000 20 35000100000 25 155 Standard deviation of the portfolio Weight2 Variance WeightWeightCovaria... View the full answer

Related Book For

Posted Date: