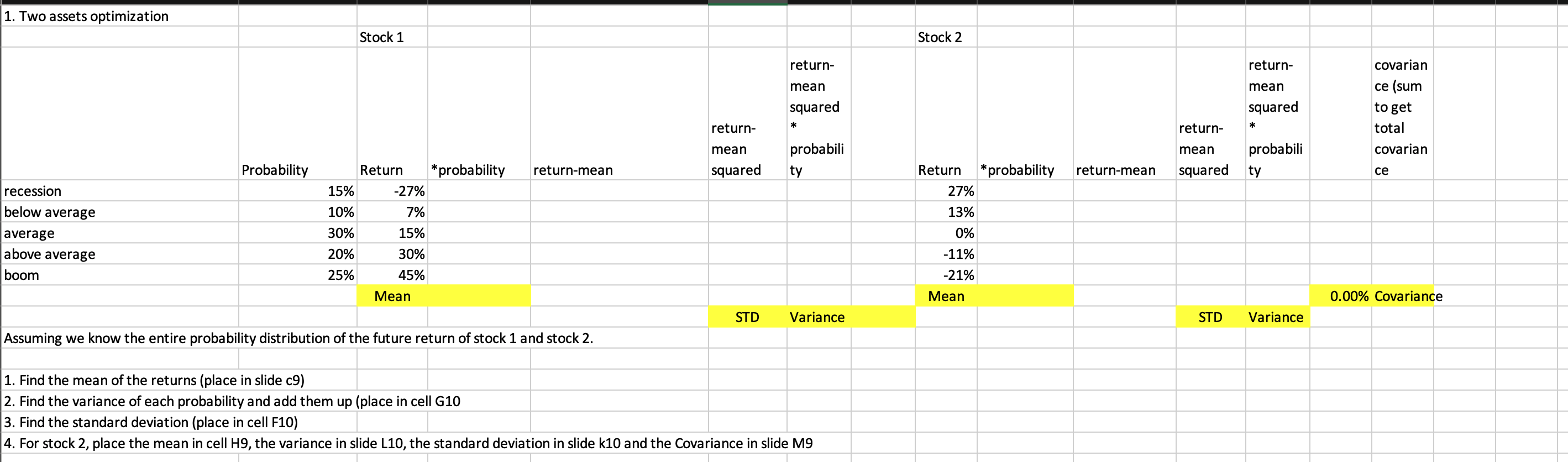

Question: 1. Two assets optimization Stock 1 Stock 2 return- return- mean mean squared squared covarian ce (sum to get total covarian * return- return- mean

1. Two assets optimization Stock 1 Stock 2 return- return- mean mean squared squared covarian ce (sum to get total covarian * return- return- mean mean probabili ty probabili ty Probability return-mean squared return-mean squared ce Return *probability 15% -27% 10% 7% Return *probability 27% 13% recession below average average above average boom 0% 30% 20% 25% 15% 30% -11% -21% 45% Mean Mean 0.00% Covariance STD Variance STD Variance Assuming we know the entire probability distribution of the future return of stock 1 and stock 2. 1. Find the mean of the returns (place in slide c9) 2. Find the variance of each probability and add them up (place in cell G10 3. Find the standard deviation (place in cell F10) 4. For stock 2, place the mean in cell H9, the variance in slide L10, the standard deviation in slide k10 and the Covariance in slide M9

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts