Question: 1) Using the data provided in this case, fill in the Excel worksheet template provided with this assignment. 2) Calculate the Net Present Value. 3)

1) Using the data provided in this case, fill in the Excel worksheet template provided with this assignment. 2) Calculate the Net Present Value. 3) Respond to Mr. Cruz's question, "Does Newton Community have sufficient cash balances to cover the forecast risks in the initial three years before ASC operations reach full capacity?" Note, the data used for the NPV analysis are estimates. Therefore, your answer should incorporate the risk associated with forecasting errors. 4) Is the trend in contribution margin a source of concern for the team? Explain why. 5) Based on your analysis offer your recommendation of whether Newtown Community Hospital would rationally invest in the ASC. 6) Respond to Mr. Cruz's question, "What crucial assumption if altered, could change the outcome of the analysis", by a) identifying one crucial assumption underlying the analysis, b) changing that assumption to a more realistic value and c) recalculating the Net Present Value based on the altered assumption.

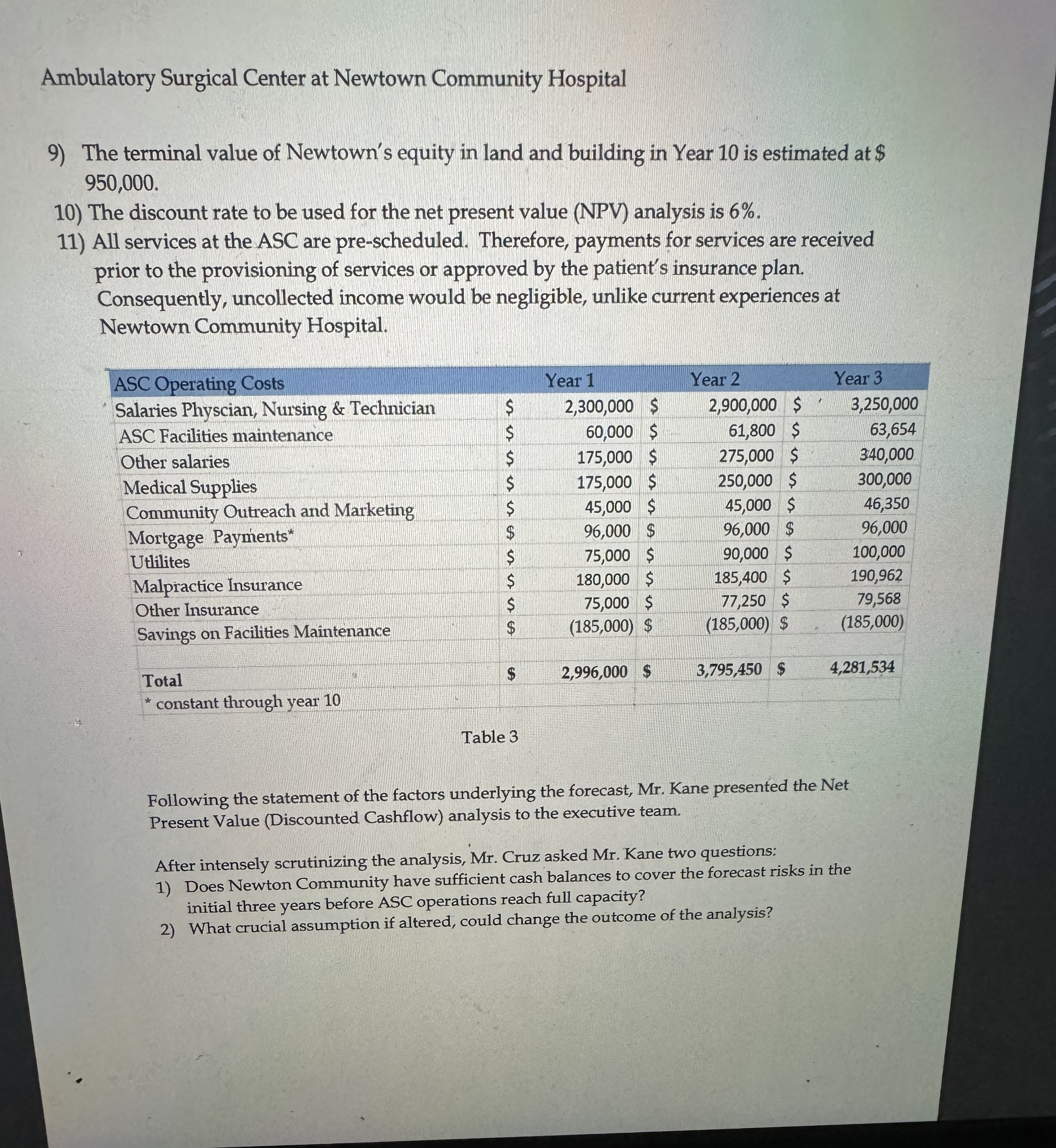

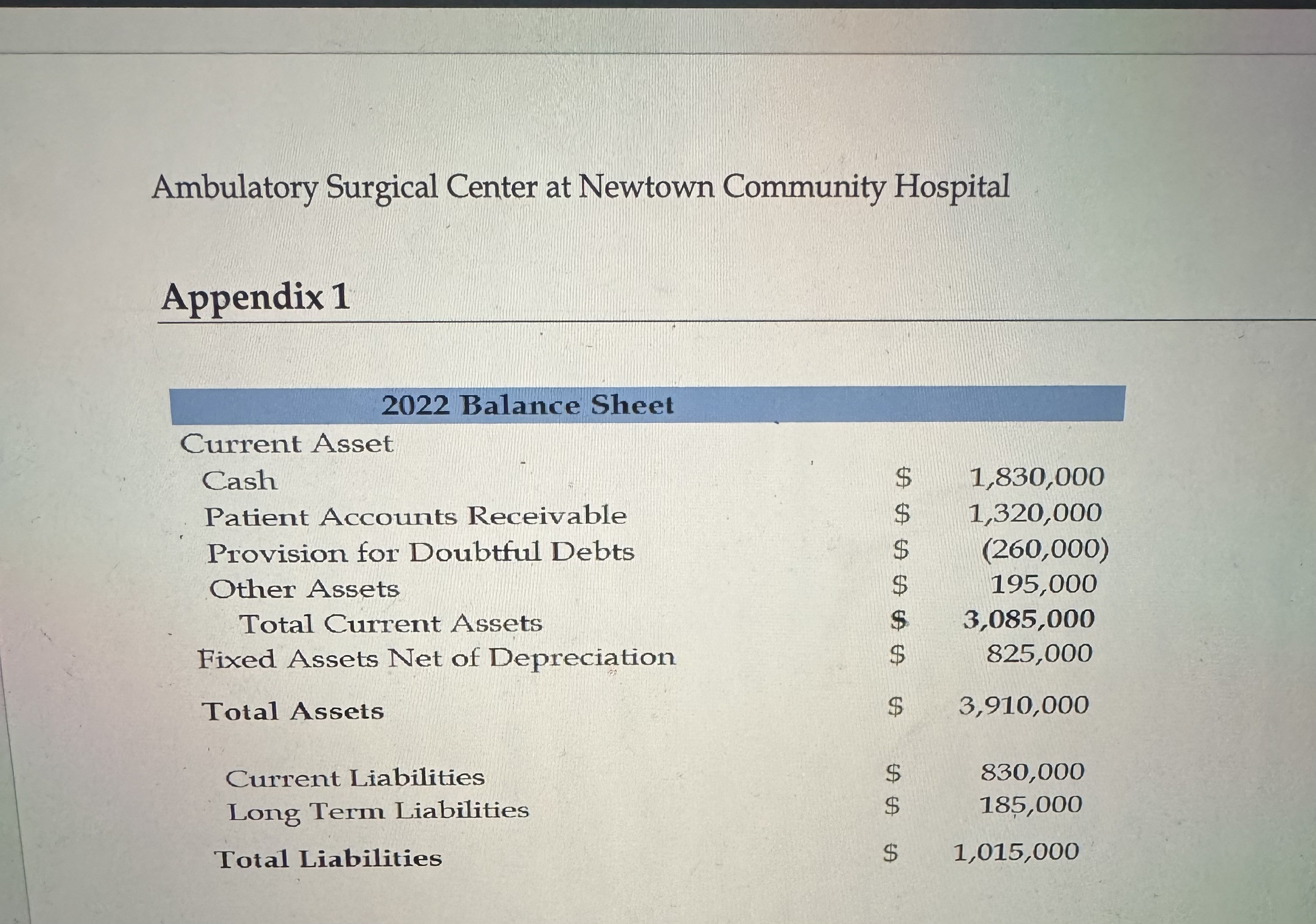

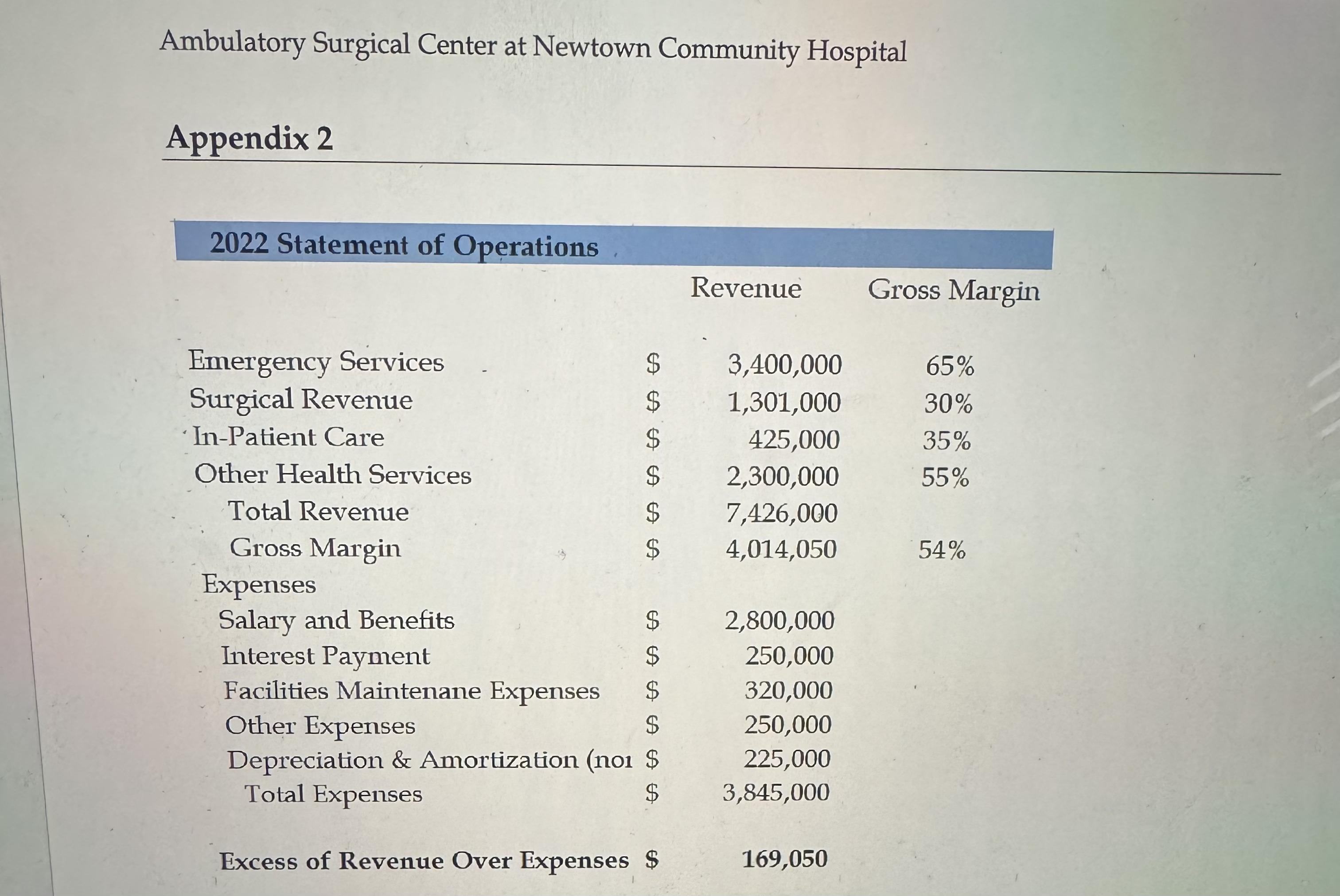

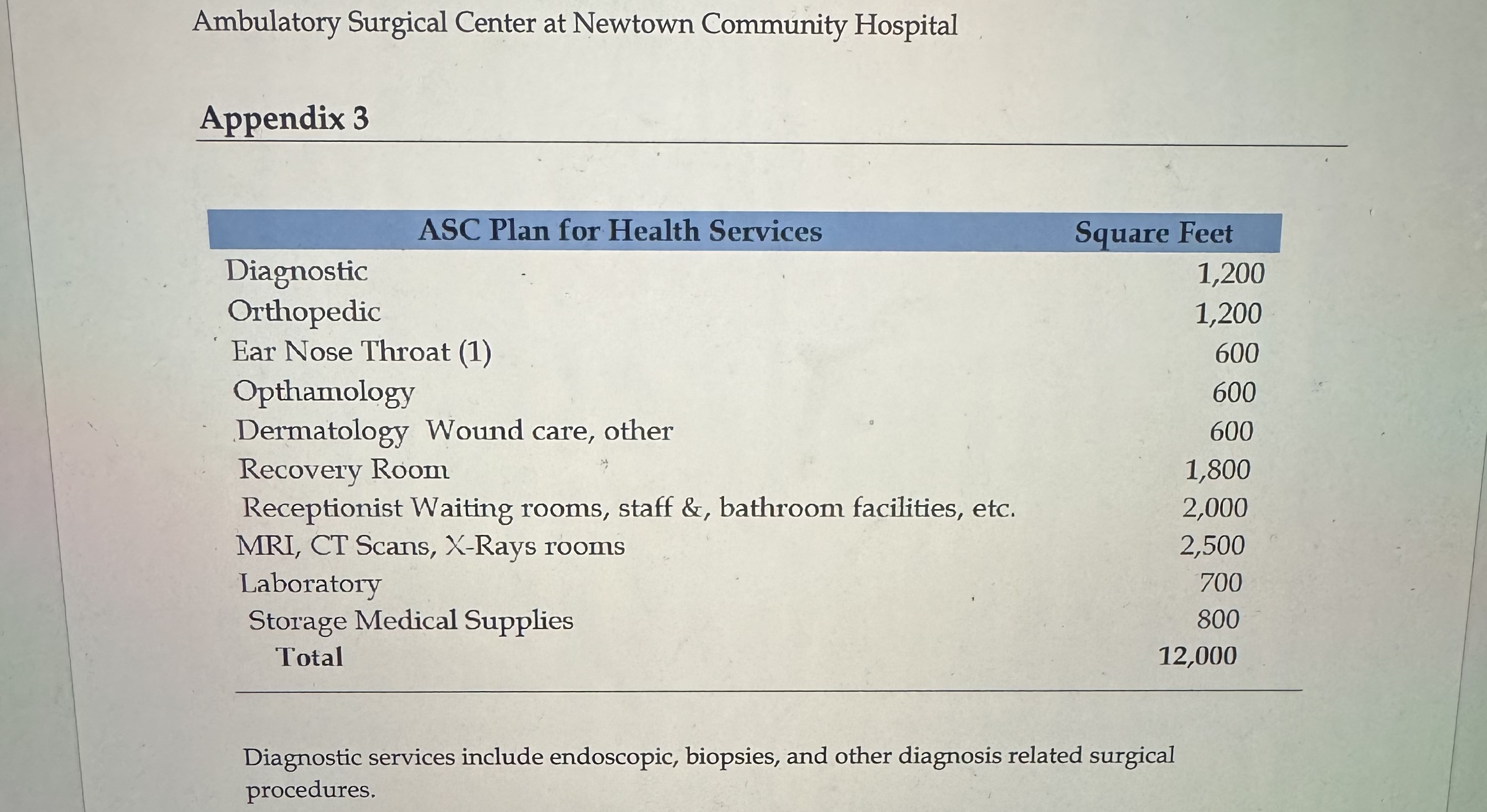

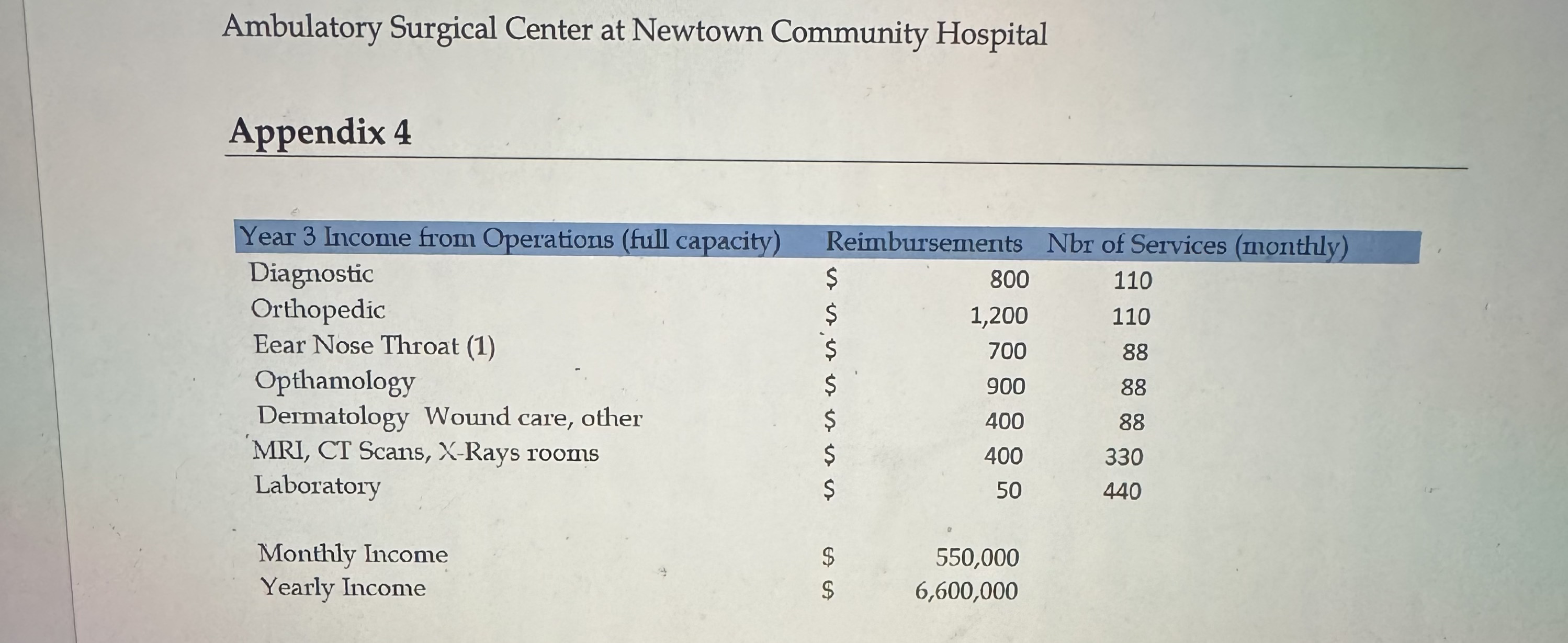

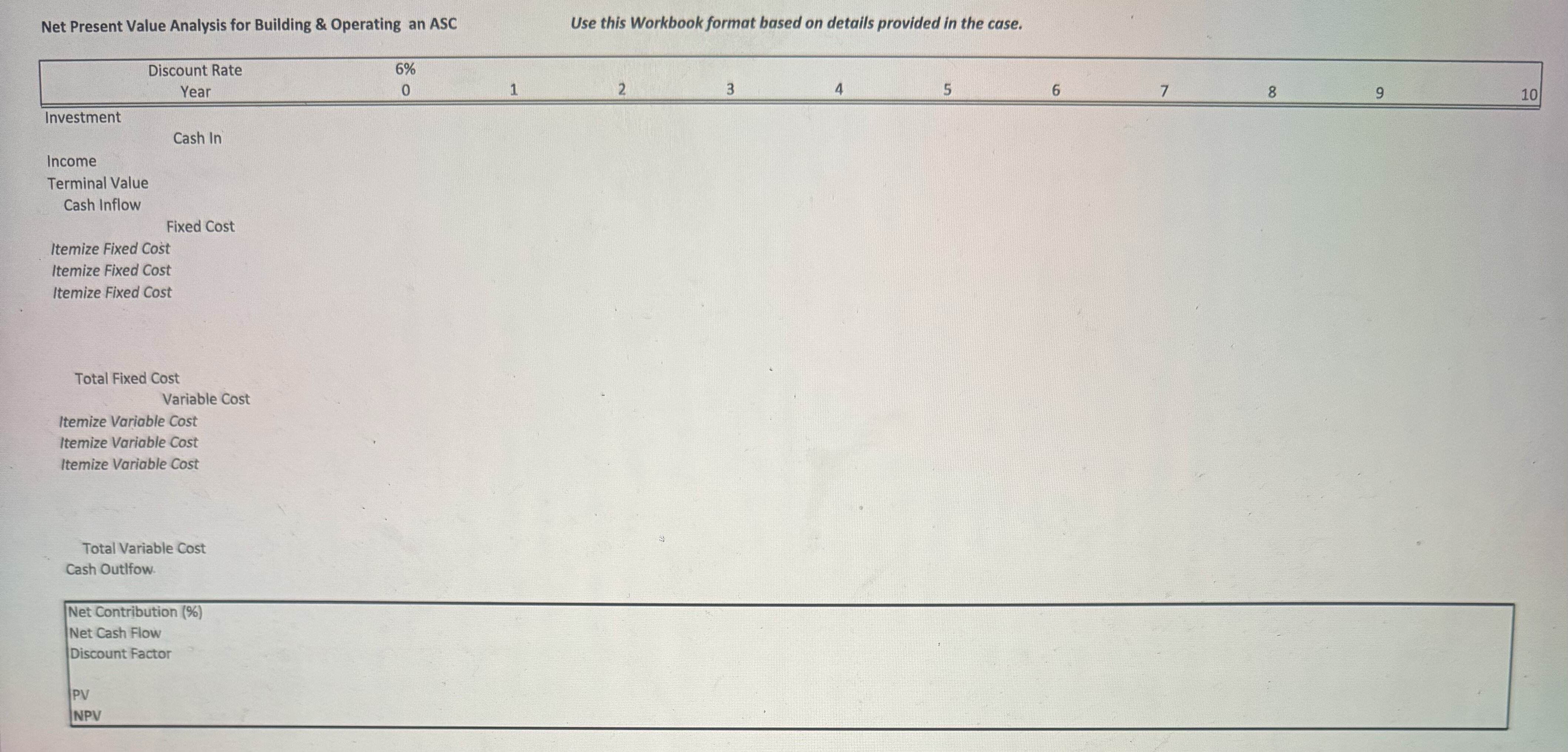

Awmowarory Surgical Center at Newton Community Hospital Author: Dr. Vinita Ittoop Pub. Date: 2022 Unpublished Product: Keywords: Marginal analysis, Sunk Cost, Free cash flow, Net Present Value analysis, Project assumptions, Scenario analysis Disciplines: Business & Management, Decision Making Abstract Like other rural non-profit hospitals, Newtown Community Hospital in Desert County, Nevada (fictional) faces major challenges to its financial viability due to low reimbursements, affordability of care, and the resultant low patient volume. In response to these long-standing pressures, Newtown Community shuttered many health services over time to reduce costs, Now, it is evaluating a plan to dramatically cut back its in-hospital operating capabilities and build an Ambulafory Surgical Center (ASC) for same-day surgical care, Management is hopeful that the shift from in-hospital surgical care to an ASC will improve operating margins while allowing Newtown Community to continue effectively serving its rural community. CASE Learning Outcomes 1) Apply the theories of marginal analysis for project evaluation 2) Make realistic assumptions about future Income from Operations and cost in preparation for discounted cash flow analysis (DCF). 3) Perform DCF analysis by calculating the net present value based on future free cash flow estimates. i 4) Perform scenario analysis based on a varying one of the key assumptions. 5) Use a Spreadsheet tool for DCF analysis Introduction Newton Community Hospital is a non-profit community hospital in Desert Cour}ty, Ne}rada. It is designated as a Critical Access Hospital by the Centers for Medicaid & Medicaid. This designation is given to a hospital that 1) provides 24/7 care to the community, 2) Has fewer than 25 acute (in-hospital) beds 3) Is located more than 35 miles from another hospital Ambulatory Surgical Center at Newtown Community Hospital 4) Has an average length of in-patient care of 96 hours (4 days) CAH designation is important for obtaining cost-based reimbursement from Medicare, instead of th.e standard fixed-amount reimbursement. Congress created the CAH program in 1997 to explicitly address the financial vulnerabilities of rural hospitals, However, the Medicare payment rate is low, around 105% over cost, and covers only the services provided to patients with Medicare, The Community Desert County is a prototype of other rural communities in Nevada, 1) Desert County has a population of 800,000 people. It is 55% White, 10% Black, 20% Native American, and 15% Hispanic, The median income is $65,000. : 2) 20% of the population is below 18 years of age, 65% between 18 and 64, and 15% over 65. 3) 85 % of the\\populah'on has medical insurance of various degrees of quality, from private insurance to Medicaid, and Medicare. 15% are uninsured. Financial Analysis of Newtown Community Hospital Mr. Robert Cruz mulled over the most recent financial reports. (See Figure 2, Appendix 1 and 2) The numbers did not help relieve his anxiety about how the management team would be able to sustain the hospital and support new investments. Robert was particularly concerned about the cash flow statement. The hospital was only able to generate $164,050 of free cash flow in 2022, The short-term debt of $ 825,000 (see Appendix 1) would come due over the course of 12 to 18 months. Consequently, cash balances would plummet significantly. He scheduled a meeting with his Chief Financial Officer, Mr. Kane, and Director of Health Services Dr. Lyons, to discuss their progress on a longer-term plan for financial viability. 7 \"?F?f\"y Otat Cash Flow from Opera Zplag $ 169,050 Depreciation & Amortization (non cash) $ 225,000 Change in Assets $ (105,000) Net Cash Provided by Operations $ 289,050 Repayment of Liabilities $ 125,000 Free Cash Flow $ 164,050 Cash at Hand (end of 2022) 1,994,050 x : i Table 1 The Meeting - At the start of the meeting, Mr. Cruz asked Mr. Kane if no strategic investments were initiated, then how long can Newton Community continue operations. ' Mr. Kane paused for a moment before responding, 1) \"If no strategic and operational changes were made very soon, the hospital will not be able to continue operations beyond two to three years as cash balance runs down\". 2) He stated that the low free cash flows were a result of multiple factors - a) low reimbursements from insurance providers, b) surgical and in-patient services were unprofitable (see Appendix 2), c) excessive costs for maintaining and operating old building structures, and d) low patient volume because of high hospital charge. 3) He noted that eliminating surgical and in-patient services would improve cash balances, but that would imply that the hospital was deficient in fulling its mission to serve the community. 4) Tf the hospital had a viable plan to improve its financial situation significantly over the next five years, then creditors would be willing to restructure its short-term debt into longer-term obligations, thereby easing pressure on cash balances. ' Then Mr. Cruz turned to Dr. Lyons about her progress on the strategic plan for building an Ambulatory Care Center (ASC), Dr. Lyons noted that her plan would substantially change the hospital's profile. She also added that from a community health perspective, the ASC would be providing much-neded surgical and diagnostic services to the community at affordable rates. With that, Dr. Lyons offered the following recommendations. 1) The analysis of in-hospital surgical procedures over the last two years indicated that 70% of the procedures could be accomplished in an ASC. 2) She recommended the closure of all in-hospital surgical units. Surgical cases that could not be done at the ASC shouldsbe transferred to the larger hospital center 40 miles away. 3) She recommended the closure of 20 of the 22 in-hospital acute. The remaining two beds would be repositioned for emergency care to be used for stabilizing seriously ill patients. 4) This plan would not require the downsizing of current staff. They would be redirected to the emergency department and to the ASC. Similarly, suitable surgical equipment and - furniture currently in use would be reused at the ASC. : 5) The range of health services to be provided at the ASC is shown in Appendix 3. The Financial Plan Mr. Kane outlined that Dr, Lyons' plan eliminated the two low-margin services that Newton Community currently provides - in-hospital surgical and in-patient care services. He noted that the current facility maintenance costs would be dramatically reduced because these two services consumed most of the maintenance costs. Mr. Kane stated that the plan estimates were based on the following 1) Purchasing $300,000 for the 2.5 acres of adjacent land. 2) Constructing a new 12,000-square-foot ASC facility on the adjacent land. : Initial Investment and Financing Estimation In 2022 Newton Community paid $75,000 to civil engineering and construction firms for detailed construction blueprints consistent with Dr. Lyons' recommended layout (see Appendix 3). Consequently, the purchase of the land and construction could begin immediately following management's goo-go decision on the ASC. Construction can be completed in 12 months. Construction and building costs are shown in Table 2 below. Intial Investment & Financing Investment ($) Land 300,000 Building Construction 730,000 Addl Equipment & Furnishing 700,000 Moving Costs 130,000 Total Investment 1,860,000 Mortage at 5% Rate 1,110,000 Federal &. State Grants 300,000 Cash 450,000 Total Financing 1,860,000 Table 2 Estimation of Future Cash Flows Mr. Kane acknowledged that forecasting the future is challenging, especially 10 years out. He stated that he used conservative assumptions to build the financial plan. However, forecast risks still remain. 1) The building construction would be completed in 12 months and ASC operations can begin within 15 months 2) The ASC is expected to operate at full capacity in Year 3. Year 3 Income from Operations is estimated to be $6,600,000 (see Appendix 4 for more details.) 3) Income from Operations in Year 1 and Year 2 are estimated at 30% and 75% of Year 3 income respectively. 4) Operational Costs in Years 1 and 2 gradually grow to reach full operational levels by Year 3. (See Table 3.) 5) Income from Operations from years 4 through 10 will rise annually by 1.25%, relative to the previous year. 6) Operating costs from Year 3 are forecast to increase by 3% annually, relative to the previous year. 7) Additional fixed investment in medical equipment of $750,000 is scheduled in Year 5 8) Marginal savings from closing current surgical and acute care facilities is estimated at $185,000 per year for 5 years following ASC opening, after which the shuttered square footage will be fully depreciated.Ambulatory Surgical Center at Newtown Community Hospital 9) The terminal value of Newtown's equity in land and building in Year 10 is estimated at $ 950,000. 10) The discount rate to be used for the net present value (NPV) analysis is 6%. 11) All services at the ASC are pre-scheduled. Therefore, payments for services are received prior to the provisioning of services or approved by the patient's insurance plan. Consequently, uncollected income would be negligible, unlike current experiences at Newtown Community Hospital. ASC Operating Costs Year 1 Year 2 Year 3 Salaries Physcian, Nursing & Technician 2,300,000 $ 2,900,000 $ 3,250,000 ASC Facilities maintenance 60,000 61,800 $ 63,654 Other salaries 175,000 275,000 $ 3:40,000 Medical Supplies 175,000 250,000 300,000 Community Outreach and Marketing 45,000 45,000 $ 16,350 Mortgage Payments* 96,000 $ 96,000 $ 96,000 Utlilites 75,000 $ 90,000 $ 100,000 Malpractice Insurance 180,000 S 185,400 $ 190,962 Other Insurance 75,000 $ 77,250 $ 79,568 Savings on Facilities Maintenance (185,000) $ (185,000) $ (185,000) Total $ 2,996,000 $ 3,795,450 $ 4,281,534 * constant through year 10 Table 3 Following the statement of the factors underlying the forecast, Mr. Kane presented the Net Present Value (Discounted Cashflow) analysis to the executive team. After intensely scrutinizing the analysis, Mr. Cruz asked Mr. Kane two questions: 1) Does Newton Community have sufficient cash balances to cover the forecast risks in the initial three years before ASC operations reach full capacity? 2) What crucial assumption if altered, could change the outcome of the analysis?Ambulatory Surgical Center at Newtown Community Hospital Appendix 1 2022 Balance Sheet Current Asset Cash 1,830,000 Patient Accounts Receivable 1,320,000 Provision for Doubtful Debts (260,000) Other Assets 195,000 Total Current Assets 3,085,000 Fixed Assets Net of Depreciation 825,000 Total Assets $ 3,910,000 Current Liabilities 830,000 Long Term Liabilities $ 185,000 Total Liabilities 1,015,000Ambulatory Surgical Center at Newtown Community Hospital Appendix 2 2022 Statement of Operations Revenue Gross Margin Emergency Services 3,400,000 65% EA Surgical Revenue $ 1,301,000 30% In-Patient Care 425,000 35% EA to Other Health Services 2,300,000 55% Total Revenue $ 7,426,000 Gross Margin $ 4,014,050 54% Expenses Salary and Benefits 2,800,000 Interest Payment 250,000 Facilities Maintenane Expenses 320,000 Other Expenses $ 250,000 Depreciation & Amortization (no1 $ 225,000 Total Expenses $ 3,845,000 Excess of Revenue Over Expenses $ 169,050Ambulatory Surgical Center at Newtown Community Hospital Appendix 3 ASC Plan for Health Services Square Feet Diagnostic 1,200 Orthopedic 1,200 Ear Nose Throat (1) 600 Opthamolog 600 Dermatology Wound care, other 600 Recovery Room 1,800 Receptionist Waiting rooms, staff &, bathroom facilities, etc. 2,000 MRI, CT Scans, X-Rays rooms 2,500 Laboratory 700 Storage Medical Supplies 800 Total 12,000 Diagnostic services include endoscopic, biopsies, and other diagnosis related surgical procedures.Ambulatory Surgical Center at Newtown Community Hospital Appendix 4 Year 3 Income from Operations (full capacity) Reimbursements Nbr of Services (monthly) Diagnostic 800 110 Orthopedic 1,200 110 Eear Nose Throat (1) 700 88 Opthamolog 900 88 Dermatology Wound care, other 400 88 MRI, CT Scans, X-Rays rooms 400 330 Laboratory 50 440 Monthly Income 550,000 Yearly Income 6,600,000Net Present Value Analysis for Building & Operating an ASC Use this Workbook format based on details provided in the case. Discount Rate 6% Year 0 2 3 4 5 6 7 8 9 10 Investment Cash In Income Terminal Value Cash Inflow Fixed Cost Itemize Fixed Cost Itemize Fixed Cost Itemize Fixed Cost Total Fixed Cost Variable Cost Itemize Variable Cost Itemize Variable Cost Itemize Variable Cost Total Variable Cost Cash Outlfow Net Contribution (%) Net Cash Flow Discount Factor PV NPV

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!