Question: 10 A theme park operator is considering building a new theme park in Spain. The operator is an experienced theme park operator but does not

![options likely to be contained in the project. [3] (ii) Describe the](https://s3.amazonaws.com/si.experts.images/answers/2024/07/6686bee4459a0_7246686bee422285.jpg)

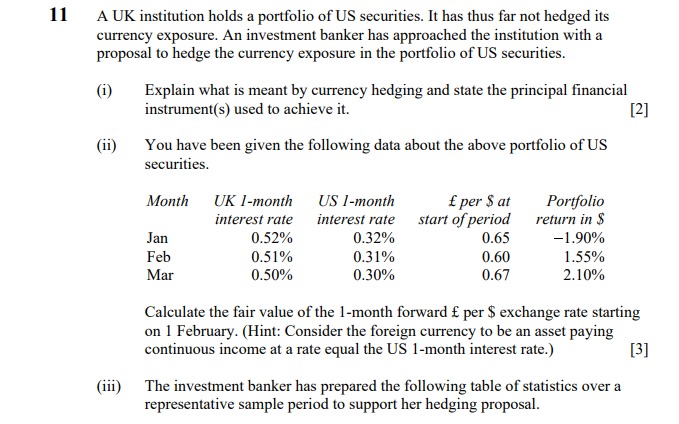

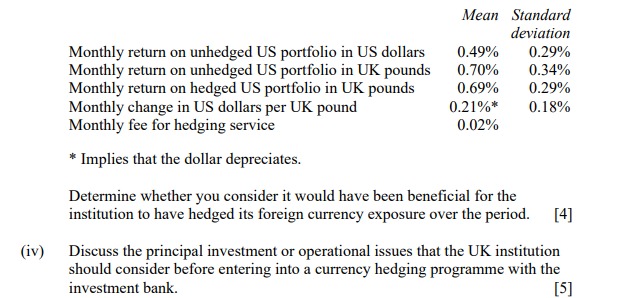

10 A theme park operator is considering building a new theme park in Spain. The operator is an experienced theme park operator but does not have any experience of Spain. (i) Describe with reasons the options likely to be contained in the project. [3] (ii) Describe the most likely valuation approach for the options. [3] (iii) State with reasons which option is likely to be the most valuable to the theme park operator. [2]11 A UK institution holds a portfolio of US securities. It has thus far not hedged its currency exposure. An investment banker has approached the institution with a proposal to hedge the currency exposure in the portfolio of US securities. (i) Explain what is meant by currency hedging and state the principal financial instrument(s) used to achieve it. [2] (ii) You have been given the following data about the above portfolio of US securities. Month UK 1-month US I-month f per $ at Portfolio interest rate interest rate start of period return in $ Jan 0.52% 0.32% 0.65 -1.90% Feb 0.51% 0.31% 0.60 1.55% Mar 0.50% 0.30% 0.67 2.10% Calculate the fair value of the 1-month forward f per $ exchange rate starting on 1 February. (Hint: Consider the foreign currency to be an asset paying continuous income at a rate equal the US 1-month interest rate.) [3] (iii) The investment banker has prepared the following table of statistics over a representative sample period to support her hedging proposal.Mean Standard deviation Monthly return on unhedged US portfolio in US dollars 0.49% 0.29% Monthly return on unhedged US portfolio in UK pounds 0.70% 0.34% Monthly return on hedged US portfolio in UK pounds 0.69% 0.29% Monthly change in US dollars per UK pound 0.21%* 0.18% Monthly fee for hedging service 0.02% * Implies that the dollar depreciates. Determine whether you consider it would have been beneficial for the institution to have hedged its foreign currency exposure over the period. [4] (iv) Discuss the principal investment or operational issues that the UK institution should consider before entering into a currency hedging programme with the investment bank. [5]12 DEF Co. is a BBB rated property company which currently has no debt. The company is about to raise a f100m 10-year bond in the public bond markets. The bond will be issued at par and the expected coupon on the bond is 9% p.a. DEF Co. has $50m shareholder's funds and has made a 10% p.a. return on equity over recent years. You should assume that return on equity equals net profit divided by shareholders' funds. (i) Stating any assumptions, calculate the expected return on equity of DEF Co. after the bond issue. [3] (ii) Now assume that the issue has been made. It was fully subscribed but at a 15% p.a. coupon. Calculate the revised expected return on equity of DEF Co. after the bond issue. [1] (iii) State what the impact of the issue has been on shareholder value. [1] (iv) Following the issue at a 15% p.a. coupon a bank has suggested that DEF Co. repurchases the bond in the market using the proceeds raised from a securitisation of various property assets. Outline the advantages and disadvantages to DEF Co. of this suggestion. [10]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts