Question: 10. Use mathematical expressions when estimates of Component GARCH models are shown below. Use the example below to express statistical significance information in ( )

10. Use mathematical expressions when estimates of Component GARCH models are shown below. Use the example below to express statistical significance information in ( ) but indicate * if significant at 1% significance level, ** at 5% significance level, ** at 10% significance level.

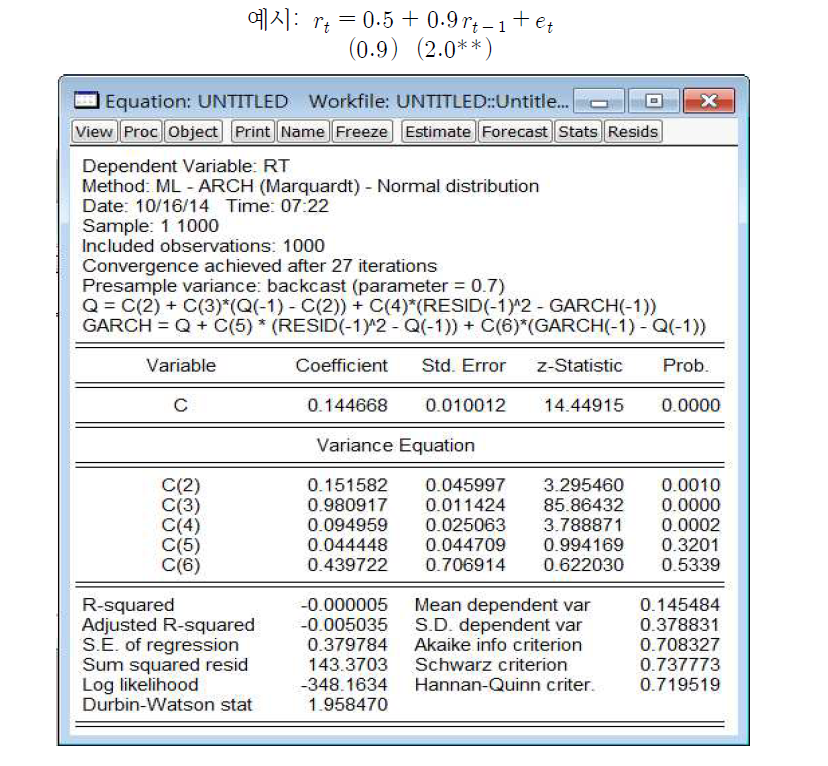

x1: rt = 0.5 + 0.9rt-1+ et (0.9) (2.0* * ) Equation: UNTITLED Workfile: UNTITLED::Untitle... X View Proc Object Print Name Freeze Estimate Forecast Stats Resids Dependent Variable: RT Method: ML - ARCH (Marquardt) - Normal distribution Date: 10/16/14 Time: 07:22 Sample: 1 1000 Included observations: 1000 Convergence achieved after 27 iterations Presample variance: backcast (parameter = 0.7) Q = C(2) + C(3)*(Q(-1) - C(2)) + C(4)*(RESID 1)^2 - GARCH(-1)) GARCH = Q + C(5) * (RESIDY2 - Q(-1)) + C(6)*(GARCH(-1) - Q(-1)) Variable Coefficient Std. Error z-Statistic Prob C 0.144668 0.010012 14.44915 0.0000 Variance Equation C(2) 0. 151582 0.045997 3.295460 0.0010 C(3) 0.980917 0.011424 85.86432 0.0000 C(4) 0.094959 0.025063 3.788871 0.0002 C(5) 0.044448 0.044709 0.994169 0.3201 C(6) 0.439722 0.706914 0.622030 0.5339 R-squared -0.000005 Mean dependent var 0.145484 Adjusted R-squared -0.005035 S.D. dependent var 0.378831 S.E. of regression 0.379784 Akaike info criterion 0.708327 Sum squared resid 143.3703 Schwarz criterion 0.737773 Log likelihood -348.1634 Hannan-Quinn criter. 0.719519 Durbin-Watson stat 1.958470

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts