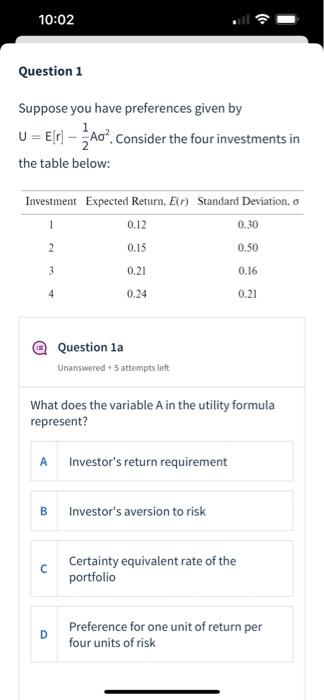

Question: 10:02 Question 1 Suppose you have preferences given by U = E[r) Ao? Consider the four investments in the table below: Investment Expected Return. Ein)

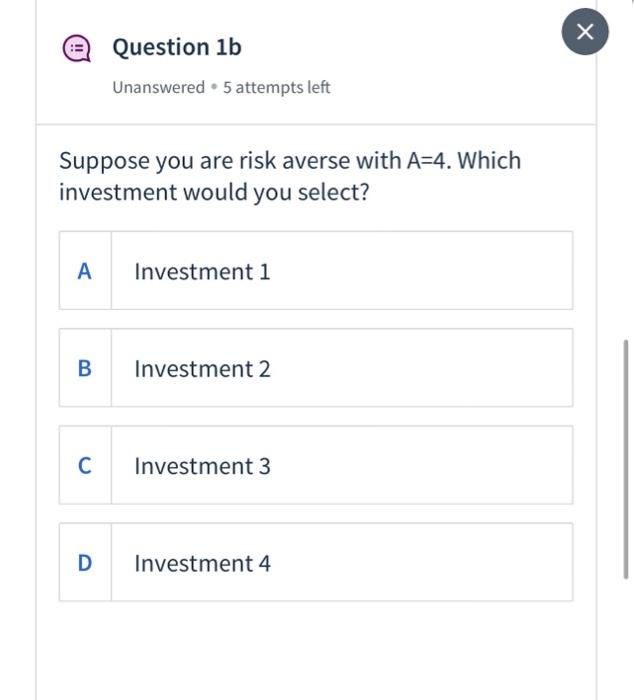

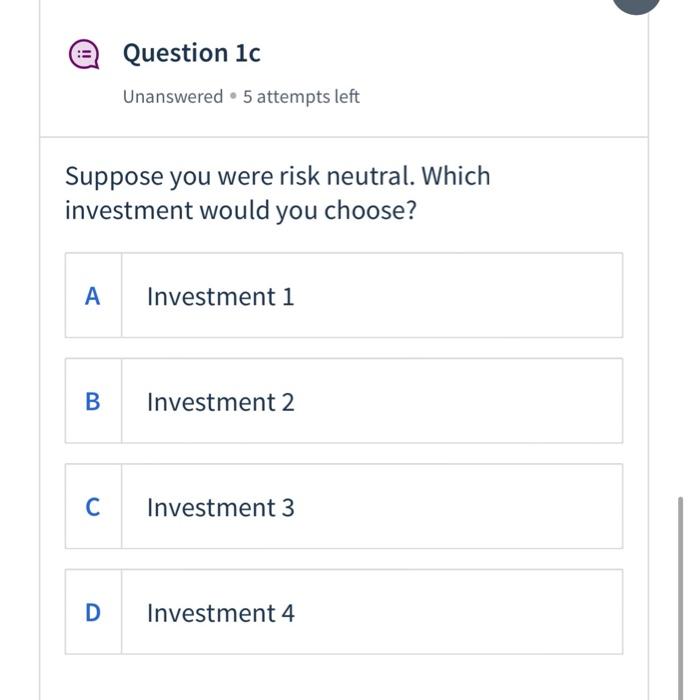

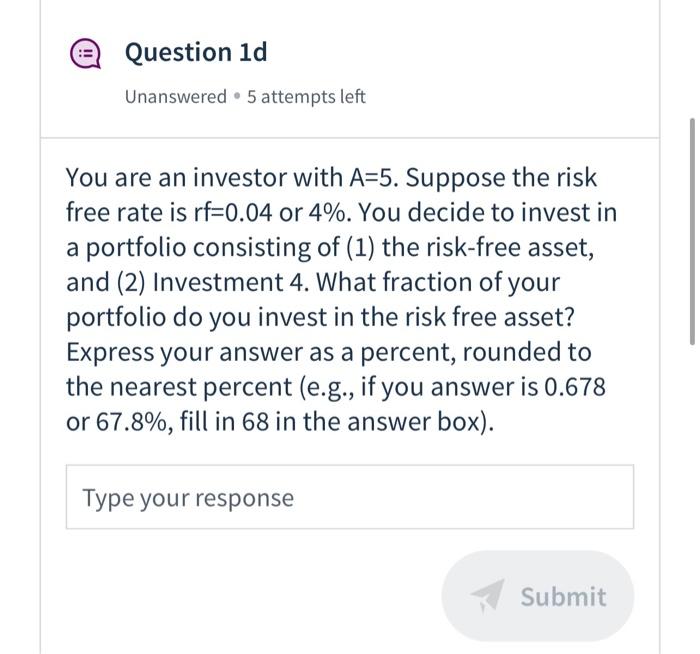

10:02 Question 1 Suppose you have preferences given by U = E[r) Ao? Consider the four investments in the table below: Investment Expected Return. Ein) Standard Deviation. 1 0.12 0.30 2 0.15 0.50 3 0.21 0.16 4 0.24 0.21 @ Question la Unanswered 5 attempts left What does the variable A in the utility formula represent? A Investor's return requirement B Investor's aversion to risk C Certainty equivalent rate of the portfolio D Preference for one unit of return per four units of risk Question 1b Unanswered 5 attempts left Suppose you are risk averse with A=4. Which investment would you select? A Investment 1 B Investment 2 Investment 3 D Investment 4 Question 1c Unanswered 5 attempts left Suppose you were risk neutral. Which investment would you choose? A Investment i B Investment 2 Investment 3 D D Investment 4 Question 1d Unanswered . 5 attempts left You are an investor with A=5. Suppose the risk free rate is rf=0.04 or 4%. You decide to invest in a portfolio consisting of (1) the risk-free asset, and (2) Investment 4. What fraction of your portfolio do you invest in the risk free asset? Express your answer as a percent, rounded to the nearest percent (e.g., if you answer is 0.678 or 67.8%, fill in 68 in the answer box). Type your response Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts