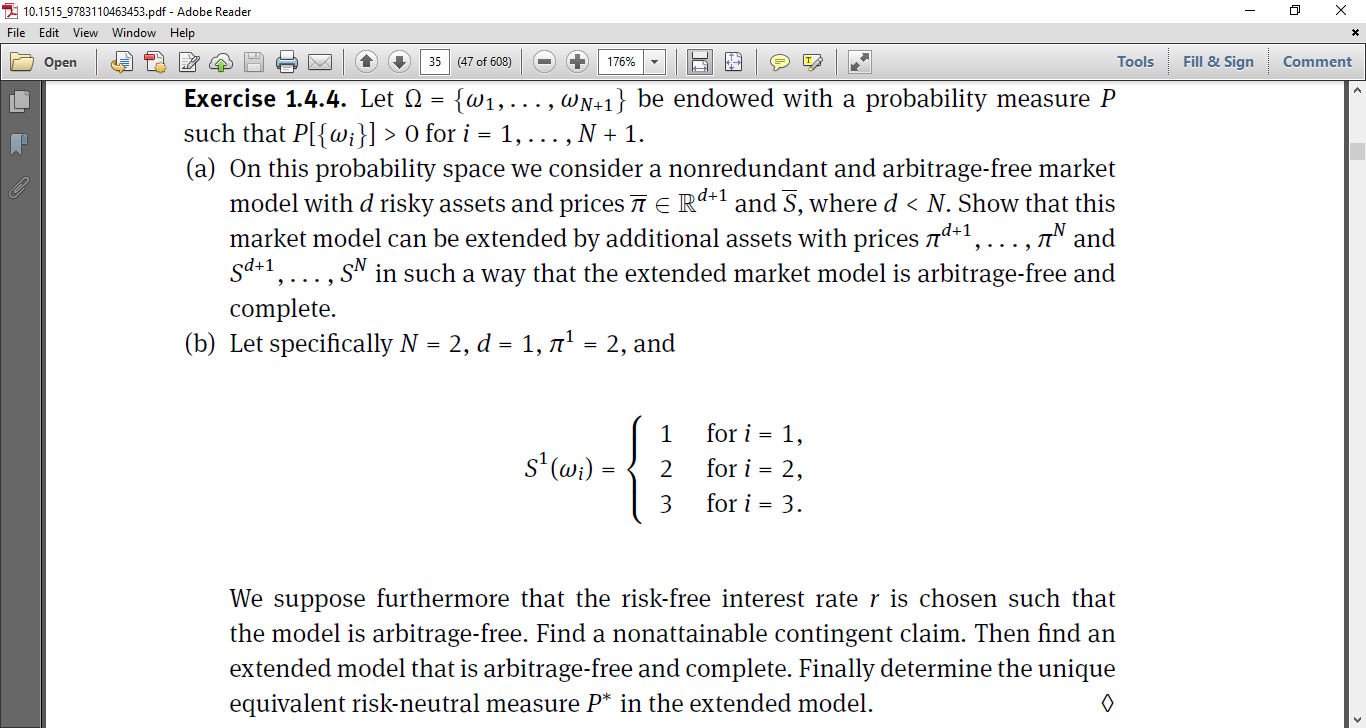

Question: 10.1515_9783110463453.pdf - Adobe Reader X File Edit View Window Help Open 35 (47 of 608) + 176% Tools Fill & Sign Comment Exercise 1.4.4. Let

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock