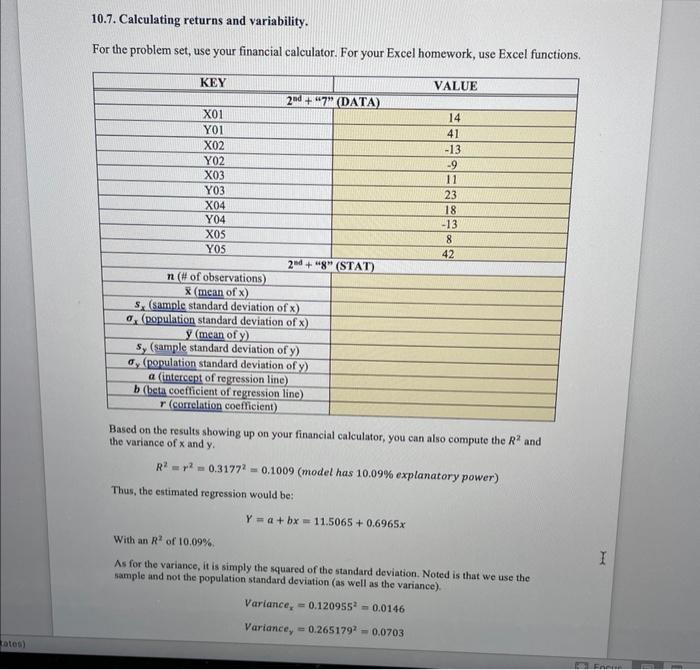

Question: 10.7. Calculating returns and variability. For the problem set, use your financial calculator. For your Excel homework, use Excel functions. Based on the results showing

10.7. Calculating returns and variability. For the problem set, use your financial calculator. For your Excel homework, use Excel functions. Based on the results showing up on your financial calculator, you can also compute the R2 and the variance of x and y. R2=r2=0.31772=0.1009( model has 10.09% explanatory power) Thus, the estimated regression would be: Y=a+bx=11.5065+0.6965x With an R2 of 10.09%. As for the variance, it is simply the squared of the standard deviation. Noted is that we use the sample and not the population standard deviation (as well as the variance). Variancex=0.1209552=0.0146Variancey=0.2651792=0.0703

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts