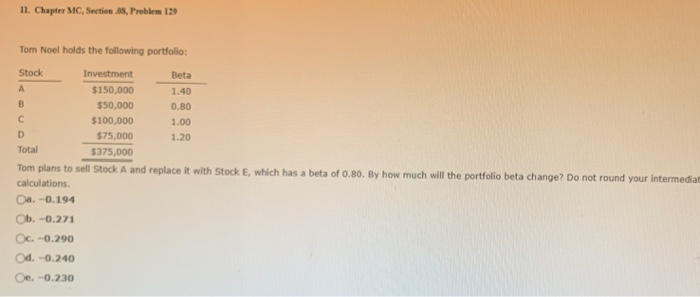

Question: 11. Chapter MC, Section 68, Problem 129 Stock Tom Noel holds the following portfolio: Investment Beta $150,000 1.40 B $50,000 0.80 $100,000 1.00 D $75,000

11. Chapter MC, Section 68, Problem 129 Stock Tom Noel holds the following portfolio: Investment Beta $150,000 1.40 B $50,000 0.80 $100,000 1.00 D $75,000 1.20 Total $375,000 Tom plans to sell Stock A and replace it with Stock E, which has a beta of 0.80. By how much will the portfolio beta change? Do not round your intermediat calculations Oa. -0.194 Ob -0.271 OC -0.290 Od. -0.240 Oe. -0.230

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock