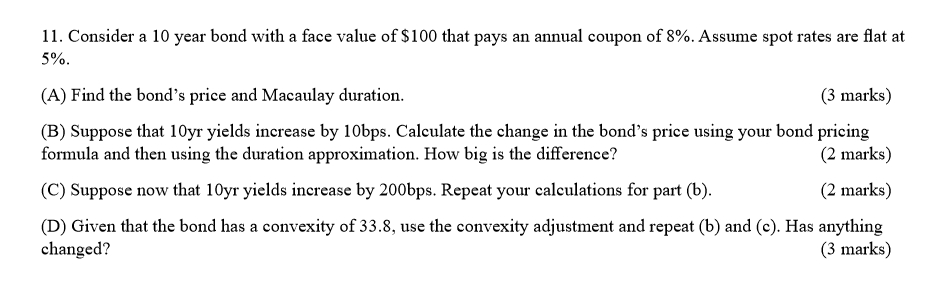

Question: 11. Consider a 10 year bond with a face value of $100 that pays an annual coupon of 8%. Assume spot rates are flat at

11. Consider a 10 year bond with a face value of $100 that pays an annual coupon of 8%. Assume spot rates are flat at 5%. (A) Find the bond's price and Macaulay duration (3 marks) (B) Suppose that 10yr yields increase by 10bps. Calculate the change in the bond's price using your bond pricing formula and then using the duration approximation. How big is the difference? (2 marks) (C) Suppose now that 10yr yields increase by 200bps. Repeat your calculations for part (b) (2 marks) (D) Given that the bond has a convexity of 33.8, use the convexity adjustment and repeat (b) and (e). Has anything changed

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock