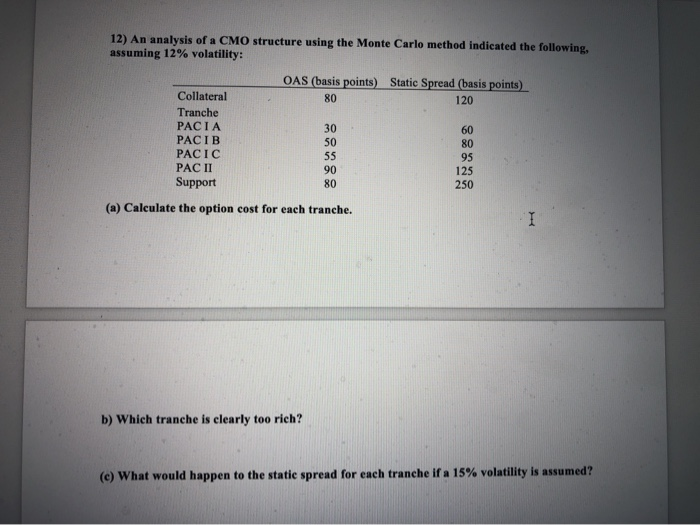

Question: 12) An analysis of a CMO structure using the Monte Carlo method indicated the following, assuming 12% volatility: OAS (basis points) Static Spread (basis points)

12) An analysis of a CMO structure using the Monte Carlo method indicated the following, assuming 12% volatility: OAS (basis points) Static Spread (basis points) 80 Collateral 120 Tranche PACIA PACIB PACIC PAC II Support 30 50 60 80 95 90 125 250 80 (a) Calculate the option cost for each tranche. b) Which tranche is elearly too rich? (c) what would happen to the static spread for each tranche if a 15% volatility is assumed? 12) An analysis of a CMO structure using the Monte Carlo method indicated the following, assuming 12% volatility: OAS (basis points) Static Spread (basis points) 80 Collateral 120 Tranche PACIA PACIB PACIC PAC II Support 30 50 60 80 95 90 125 250 80 (a) Calculate the option cost for each tranche. b) Which tranche is elearly too rich? (c) what would happen to the static spread for each tranche if a 15% volatility is assumed

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts