Question: 12:14 LTE Expert Q&A Done Please solve for question d only. 1. You are given the following data for a bond. The Coupon Payment is

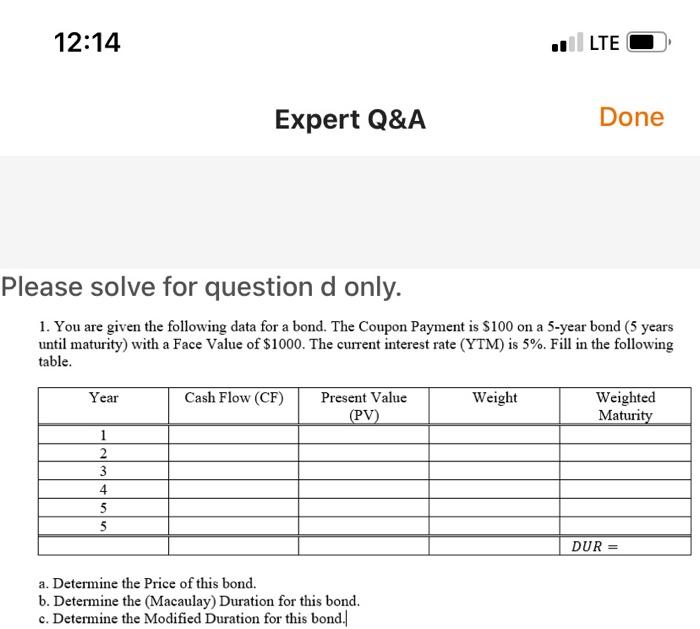

12:14 LTE Expert Q&A Done Please solve for question d only. 1. You are given the following data for a bond. The Coupon Payment is $100 on a 5-year bond (5 years until maturity) with a Face Value of $1000. The current interest rate (YTM) is 5%. Fill in the following table. Cash Flow (CF) Present Value Weight Weighted (PV) Maturity 1 Year 2 3 4 5 5 DUR = a. Determine the Price of this bond. b. Determine the (Macaulay) Duration for this bond. c. Determine the Modified Duration for this bond. d. (FILL IN THE TABLE BELOW) Calculate the APPROXIMATE new price of the bond using your measure of modified duration and the percentage change in the price of the bond for the following interest rates (Columns 2 and 3). Calculate the exact new price of the bond (above) and the exact percentage change in the price of the bond for the following interest rates (Columns for and 5). (NOTE: DO NOT UPDATE "n" FOR THE PROBLEMS BELOW; n=5). %AP - MDAI Pr+1-P- (P.MDAL Pe+1 = (1 +MDI.P. - MDP iz+1 F (1 + i)" Pon - c[:(1-6 +)))+ a time YTM New Price Pt+1 (Approx) Percentage Change in the Price %AP (Approx) New Price Pe 1 (Actual) Percentage Change in the Price %AP (Actual) 0.02 0.03 0.04 0.05 0.06 0.07 0.08

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts