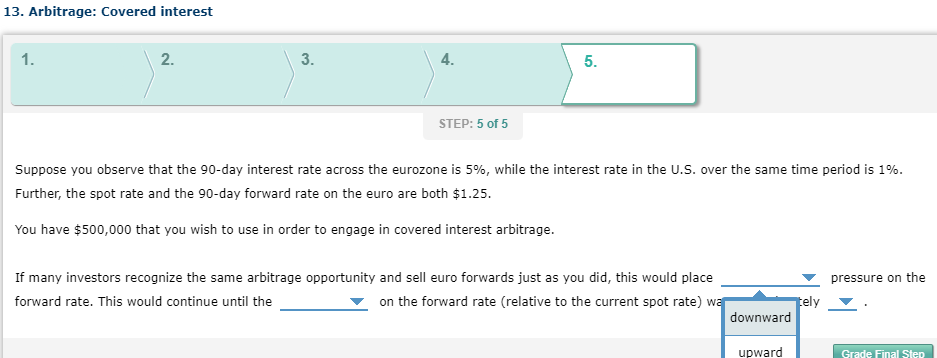

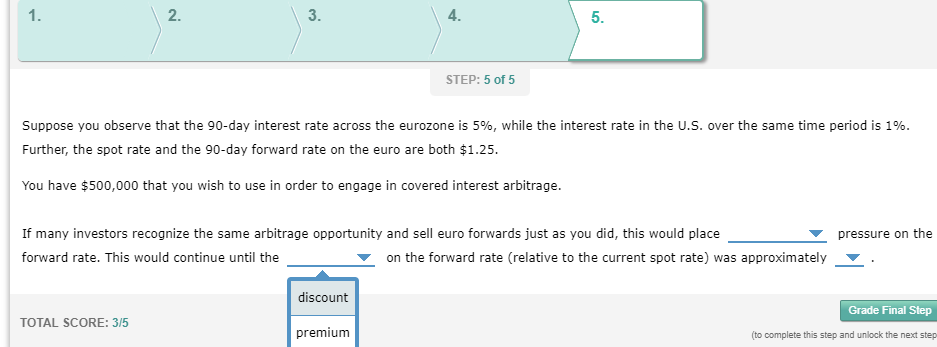

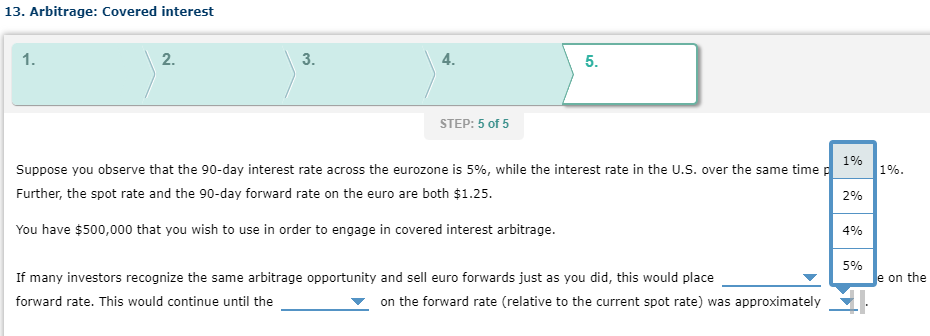

Question: 13. Arbitrage: Covered interest 1. 2. 3. 4. 5. STEP: 5 of 5 Suppose you observe that the 90-day interest rate across the eurozone is

13. Arbitrage: Covered interest 1. 2. 3. 4. 5. STEP: 5 of 5 Suppose you observe that the 90-day interest rate across the eurozone is 5%, while the interest rate in the U.S. over the same time period is 1%. Further, the spot rate and the 90-day forward rate on the euro are both $1.25. You have $500,000 that you wish to use in order to engage in covered interest arbitrage. pressure on the If many investors recognize the same arbitrage opportunity and sell euro forwards just as you did, this would place forward rate. This would continue until the on the forward rate (relative to the current spot rate) wa tely downward upward Grade Final Step 1. 2. 3 . 4. 5. STEP: 5 of 5 Suppose you observe that the 90-day interest rate across the eurozone is 5%, while the interest rate in the U.S. over the same time period is 1%. Further, the spot rate and the 90-day forward rate on the euro are both $1.25. You have $500,000 that you wish to use in order to engage in covered interest arbitrage. pressure on the If many investors recognize the same arbitrage opportunity and sell euro forwards just as you did, this would place forward rate. This would continue until the on the forward rate (relative to the current spot rate) was approximately discount Grade Final Step TOTAL SCORE: 3/5 premium (to complete this step and unlock the next step 13. Arbitrage: Covered interest 1. 2 . 3. 4. 5. STEP: 5 of 5 1% 1%. Suppose you observe that the 90-day interest rate across the eurozone is 5%, while the interest rate in the U.S. over the same time Further, the spot rate and the 90-day forward rate on the euro are both $1.25. 2% You have $500,000 that you wish to use in order to engage in covered interest arbitrage. 4% 5% le on the If many investors recognize the same arbitrage opportunity and sell euro forwards just as you did, this would place forward rate. This would continue until the on the forward rate (relative to the current spot rate) was approximately

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts