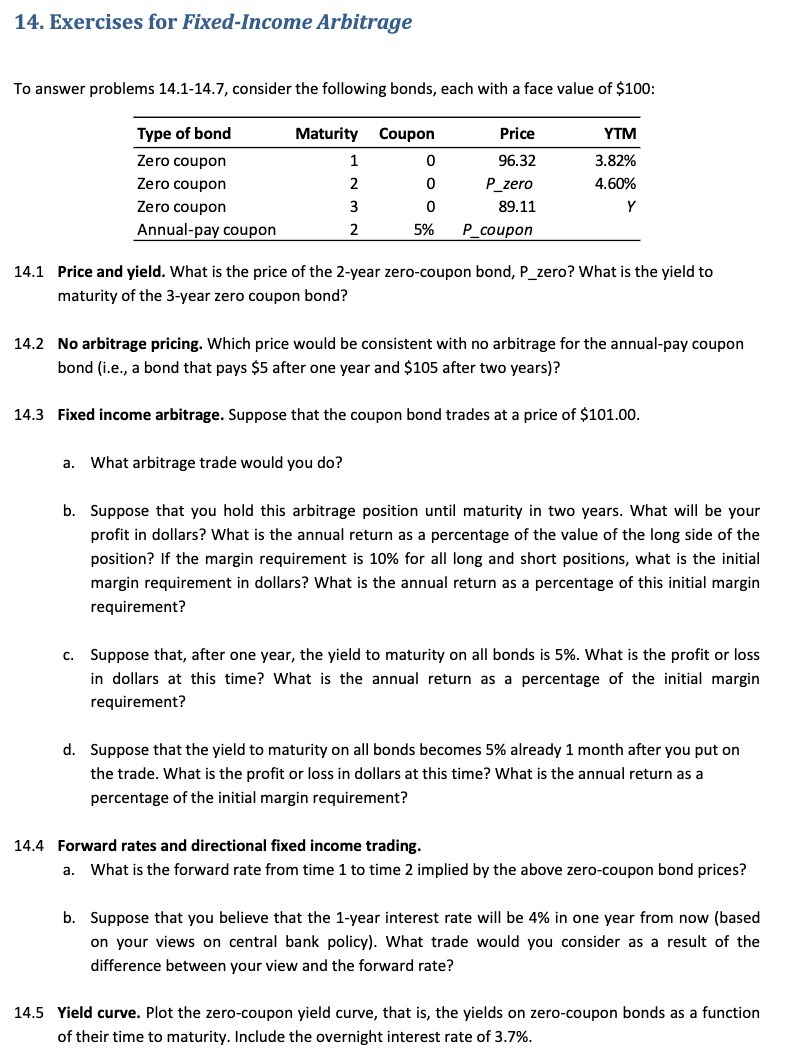

Question: 14. Exercises for Fixed-Income Arbitrage To answer problems 141-14.?r consider the following bonds, each with a face value of 5100: Type of bond Maturity Coupon

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock