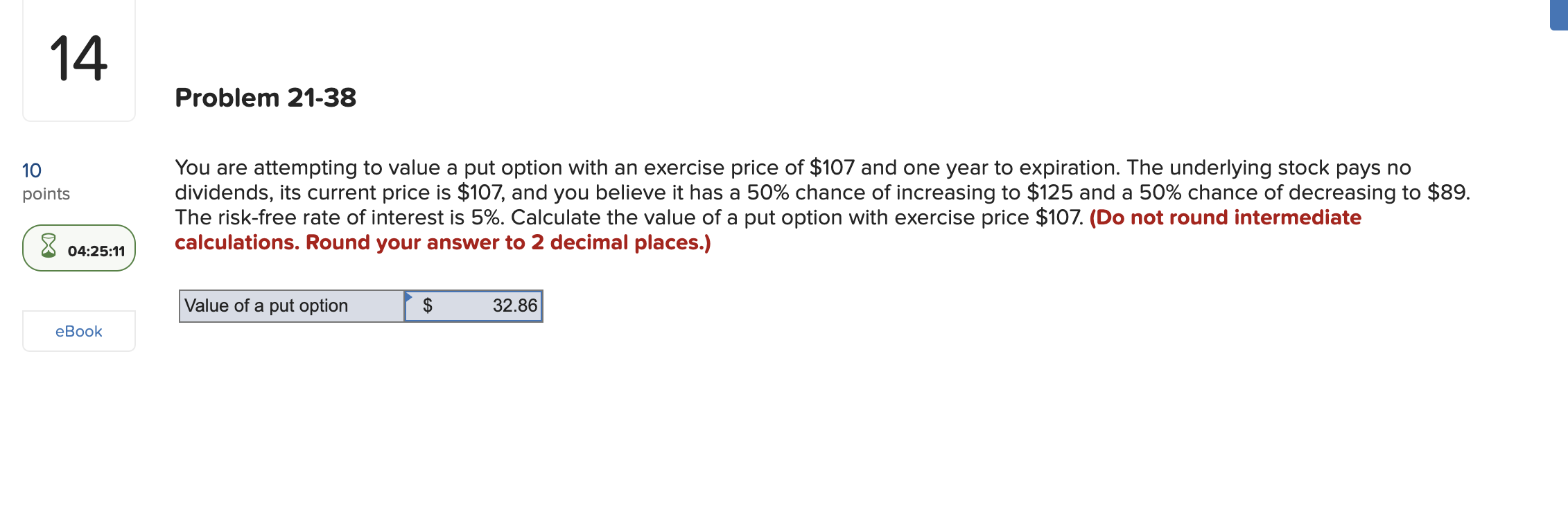

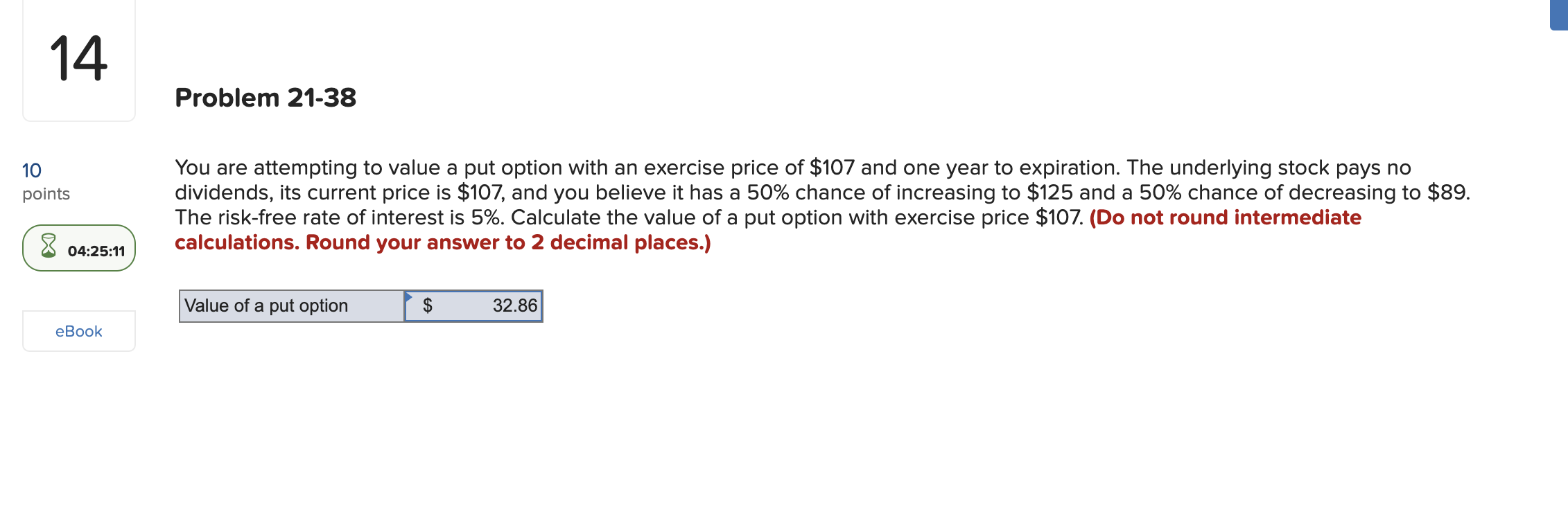

Question: 14 Problem 21-38 10 points You are attempting to value a put option with an exercise price of $107 and one year to expiration. The

14 Problem 21-38 10 points You are attempting to value a put option with an exercise price of $107 and one year to expiration. The underlying stock pays no dividends, its current price is $107, and you believe it has a 50% chance of increasing to $125 and a 50% chance of decreasing to $89. The risk-free rate of interest is 5%. Calculate the value of a put option with exercise price $107. (Do not round intermediate calculations. Round your answer to 2 decimal places.) 8 04:25:11 Value of a put option 32.86 eBook 14 Problem 21-38 10 points You are attempting to value a put option with an exercise price of $107 and one year to expiration. The underlying stock pays no dividends, its current price is $107, and you believe it has a 50% chance of increasing to $125 and a 50% chance of decreasing to $89. The risk-free rate of interest is 5%. Calculate the value of a put option with exercise price $107. (Do not round intermediate calculations. Round your answer to 2 decimal places.) 8 04:25:11 Value of a put option 32.86 eBook

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts