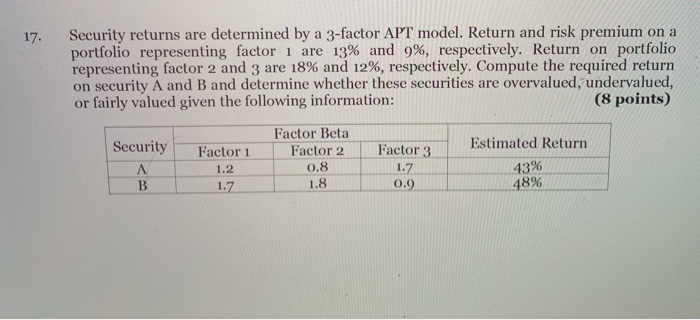

Question: 17 . Security returns are determined by a 3-factor APT model. Return and risk premium on a portfolio representing factor 1 are 13% and 9%,

17 . Security returns are determined by a 3-factor APT model. Return and risk premium on a portfolio representing factor 1 are 13% and 9%, respectively. Return on portfolio representing factor 2 and 3 are 18% and 12%, respectively. Compute the required return on security A and B and determine whether these securities are overvalued, undervalued, or fairly valued given the following information: (8 points) Factor 3 Estimated Return Security A B Factor Beta Factor 2 0.8 1.8 Factor 1 1.2 1.7 1.7 43% 48% 0.9

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock