Question: ( 17 ) Suppose YOU are the Pay fixed counterparty in a plain vanilla fixed vs . floating swap , having a notional

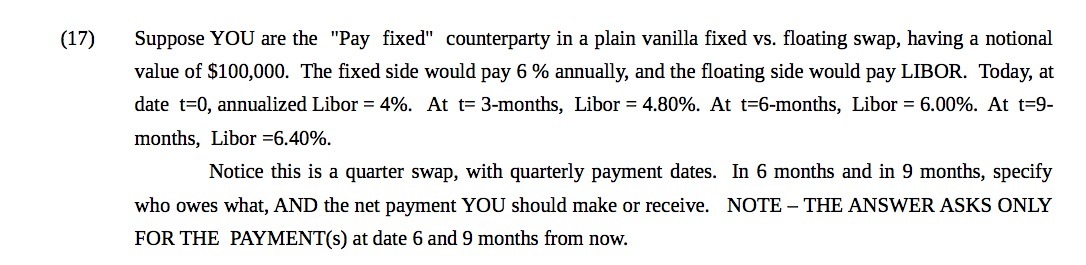

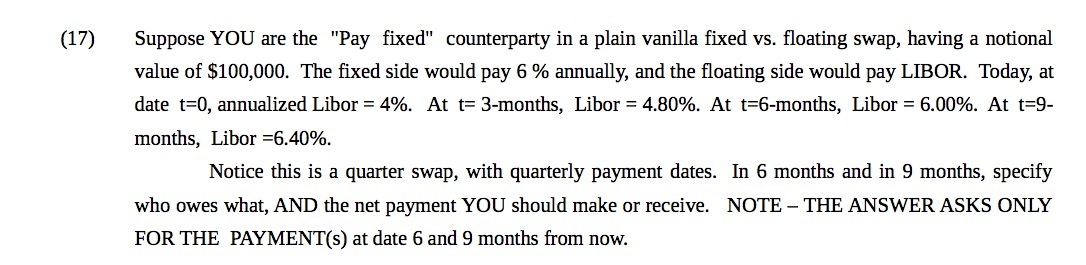

( 17 ) Suppose YOU are the " Pay fixed " counterparty in a plain vanilla fixed vs . floating swap , having a notional value of $100, 000 . The fixed side would pay 6 %/0 annually , and the floating side would pay LIBOR. Today , at date 1 = 0 , annualized Libor = 4%/0 . At 1 = 3 - months , Libor = 4.80% . At 1 = 6 - months , Libor = 6.00% . At 1 = 9 - months , Libor = 6.40% . Notice this is a quarter swap , with quarterly payment dates . In 6 months and in 9 months , specify who owes what , AND the net payment YOU should make or receive . NOTE _ THE ANSWER ASKS ONLY FOR THE PAYMENT ( s ) at date 6 and 9 months from now

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock