Question: (18-II-3) Please help me correct this problem and provide and explanation. The fields with a red x to the right are incorrect. Recording and Reporting

(18-II-3) Please help me correct this problem and provide and explanation. The fields with a red x to the right are incorrect.

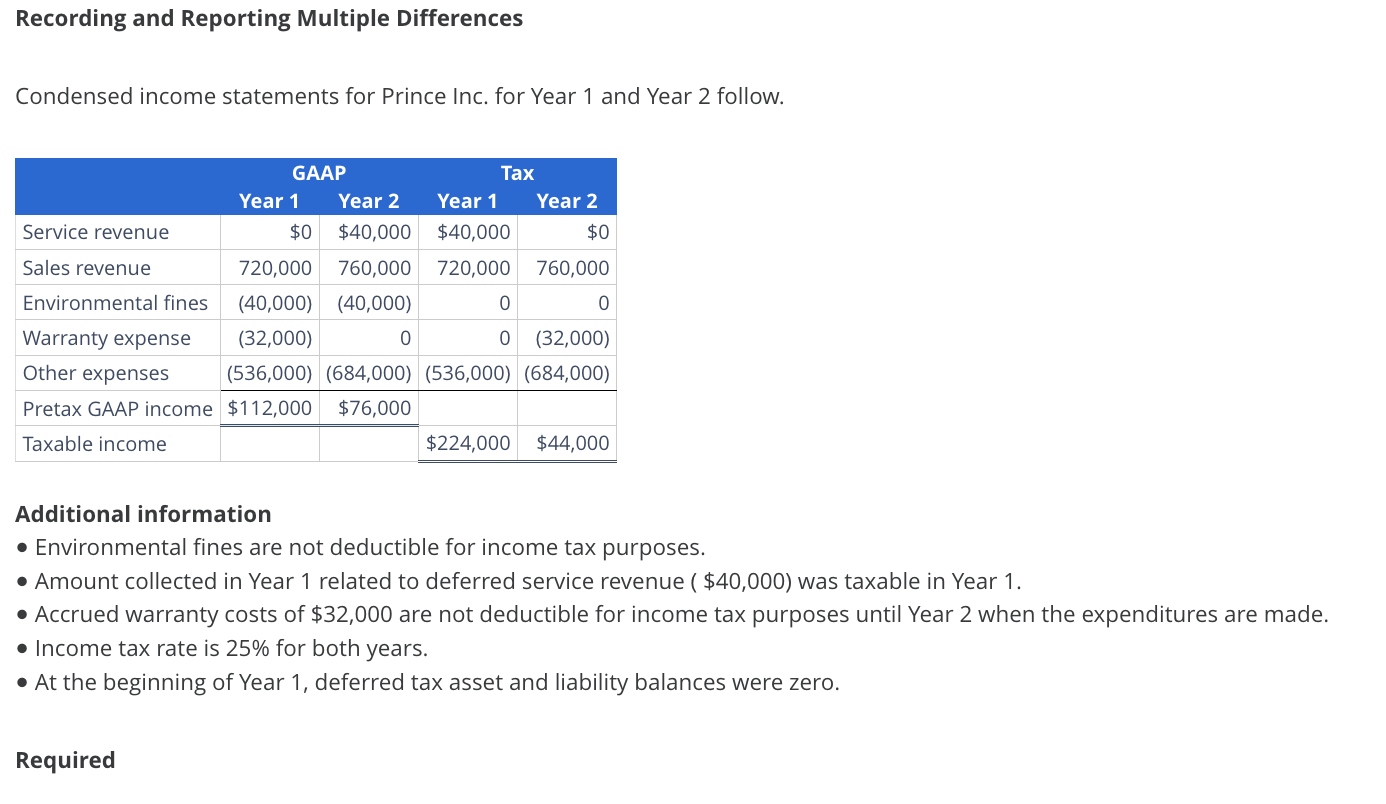

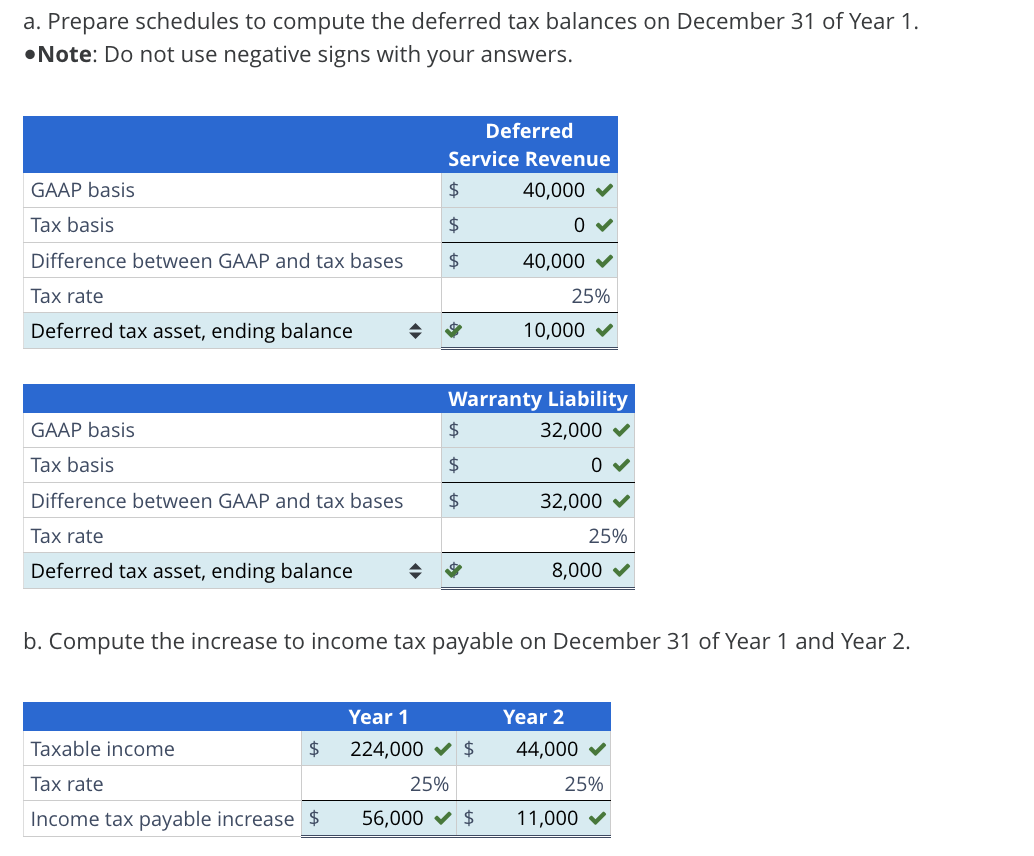

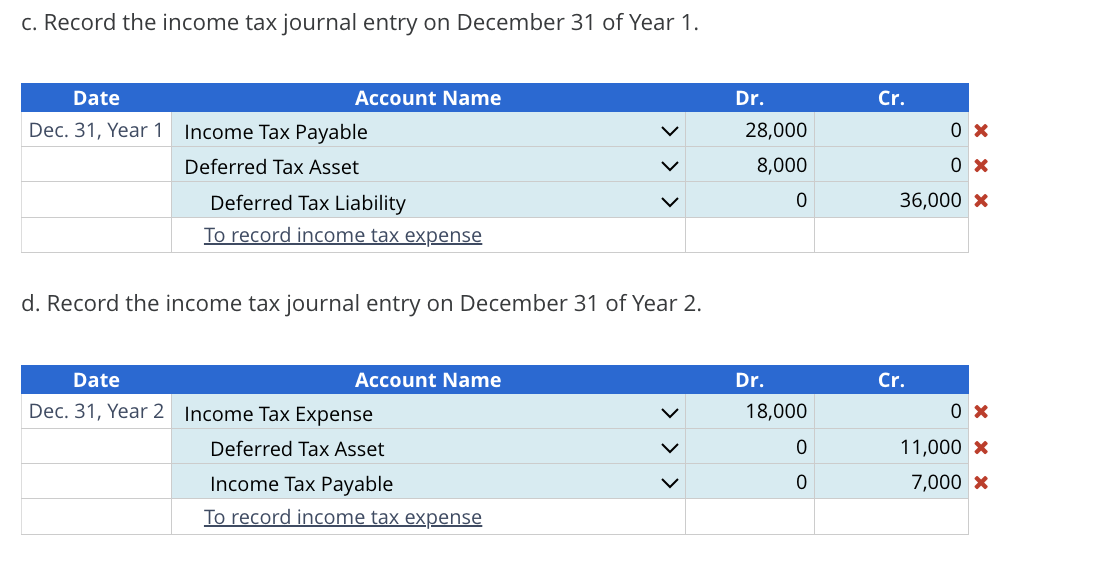

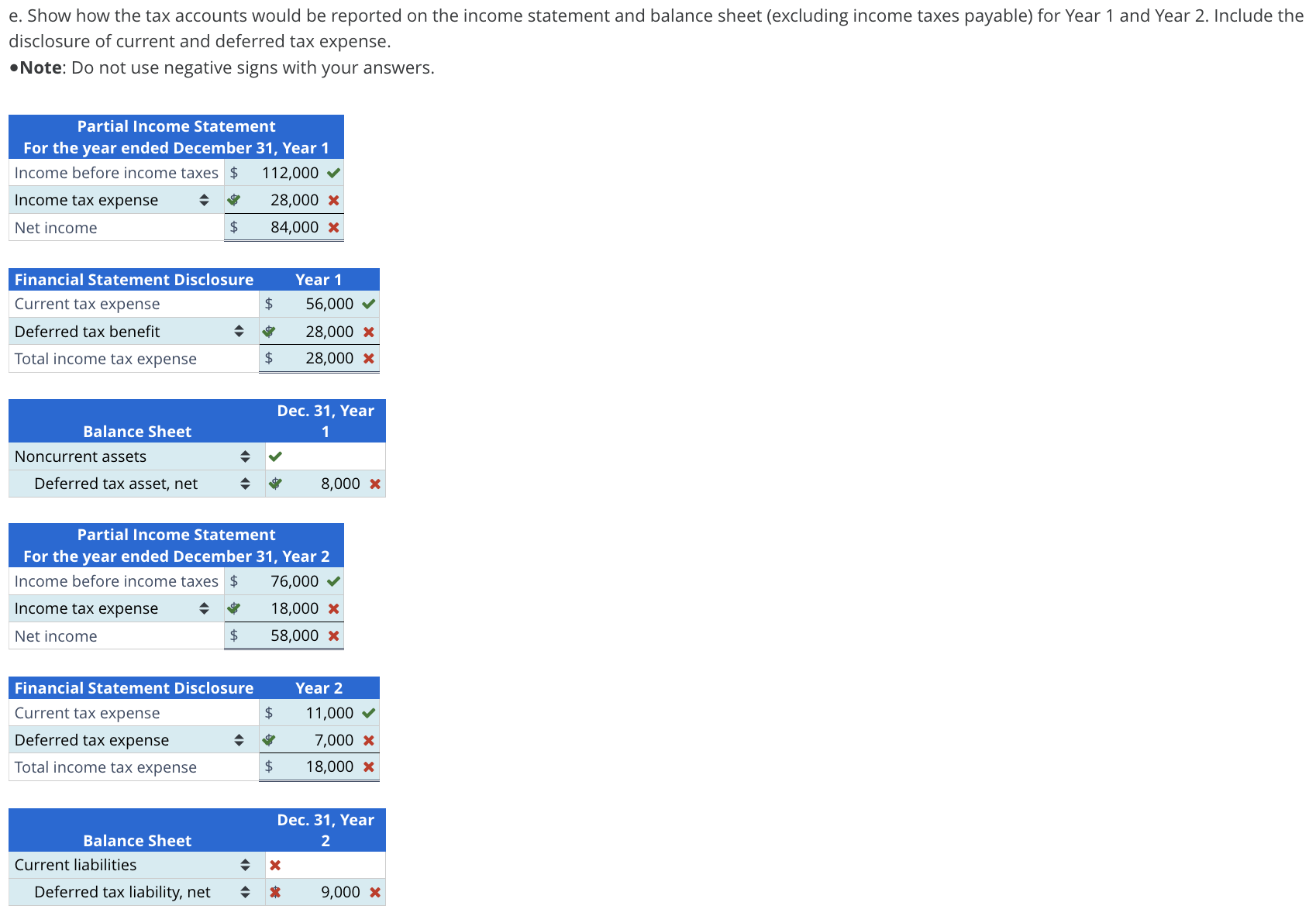

Recording and Reporting Multiple Differences Condensed income statements for Prince Inc. for Year 1 and Year 2 follow. GAAP Tax Year 1 Year 2 Year 1 Year 2 Service revenue $0 $40,000 $40,000 $0 Sales revenue 720,000 760,000 720,000 760,000 Environmental fines = (40,000) (40,000) 0 0 Warranty expense (32,000) 0 0 (32,000) Other expenses (536,000) (684,000) (536,000) (684,000) Pretax GAAP income $112,000 $76,000 Taxable income $224,000 $44,000 Additional information e Environmental fines are not deductible for income tax purposes. * Amount collected in Year 1 related to deferred service revenue ( $40,000) was taxable in Year 1. e Accrued warranty costs of $32,000 are not deductible for income tax purposes until Year 2 when the expenditures are made. [ncome tax rate is 25% for both years. e At the beginning of Year 1, deferred tax asset and liability balances were zero. Required a. Prepare schedules to compute the deferred tax balances on December 31 of Year 1. eNote: Do not use negative signs with your answers. Deferred Service Revenue GAAP basis $ 40,000 v Tax basis $ 0v Difference between GAAP and tax bases $ 40,000 v Tax rate 25% Deferred tax asset, ending balance s & 10,000 v GAAP basis $ 32,000 v Tax basis $ 0v Difference between GAAP and tax bases $ 32,000 v Tax rate 25% Deferred tax asset, ending balance s & 8,000 v b. Compute the increase to income tax payable on December 31 of Year 1 and Year 2. Year 1 Year 2 Taxable income $ 224000 v $ 44,000 v Tax rate 25% 25% Income tax payable increase | $ 56,000 v $ 11,000 v c. Record the income tax journal entry on December 31 of Year 1. (D] (] Account Name b (o Dec. 31, Year 1 Income Tax Payable v 28,000 0 % Deferred Tax Asset v 8,000 0 x Deferred Tax Liability v 0 36,000 % To record income tax expense d. Record the income tax journal entry on December 31 of Year 2. (DE] (] Account Name b (o Dec. 31, Year 2 Income Tax Expense v 18,000 0 x Deferred Tax Asset v 0 11,000 x Income Tax Payable v 0 7,000 % To record income tax expense e. Show how the tax accounts would be reported on the income statement and balance sheet (excluding income taxes payable) for Year 1 and Year 2. Include the disclosure of current and deferred tax expense. eNote: Do not use negative signs with your answers. Partial Income Statement For the year ended December 31, Year 1 Income before income taxes $ 112,000 + Income tax expense s 28,000 % Net income $ 84,000 % Current tax expense $ 56,000 v Deferred tax benefit $ & 28000 x Total income tax expense $ 28,000 x Dec. 31, Year Balance Sheet 1 Noncurrent assets s Vv Deferred tax asset, net s @ 8,000 x Partial Income Statement For the year ended December 31, Year 2 Income before income taxes $ 76,000 v Income tax expense $ 18,000 % Net income $ 58,000 % Current tax expense $ 11,000 + Deferred tax expense s @ 7,000 x Total income tax expense $ 18,000 % Dec. 31, Year Balance Sheet 2 Current liabilities s % Deferred tax liability, net & % 9,000 x f. Compute the effective tax rate for Year 1. Ratio Numerator Denominator Result Effective tax rate, Year 1 $ 28,000 x 112,000 V 25%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!