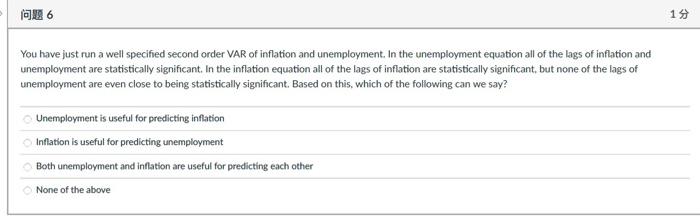

Question: 19 You have just run a well specified second order VAR of inflation and unemployment. In the unemployment equation all of the lags of inflation

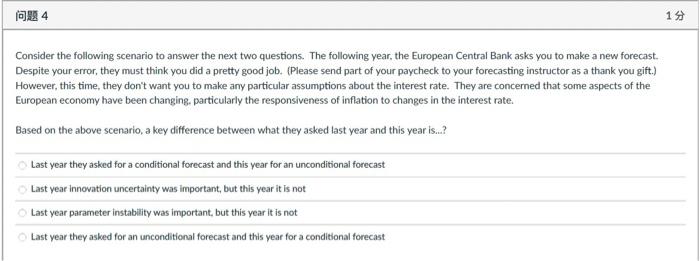

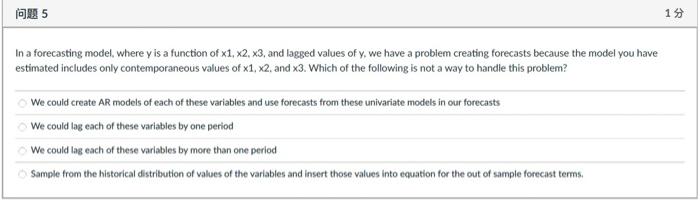

19 You have just run a well specified second order VAR of inflation and unemployment. In the unemployment equation all of the lags of inflation and unemployment are statistically significant. In the inflation equation all of the lags of inflation are statistically significant, but none of the lags of unemployment are even close to being statistically significant. Based on this, which of the following can we say? Unemployment is useful for predicting inflation Inflation is useful for predicting unemployment Both unemployment and inflation are useful for predicting each other None of the above34 4 19 Consider the following scenario to answer the next two questions. The following year, the European Central Bank asks you to make a new forecast. Despite your error, they must think you did a pretty good job. (Please send part of your paycheck to your forecasting instructor as a thank you gift.) However, this time, they don't want you to make any particular assumptions about the interest rate. They are concerned that some aspects of the European economy have been changing. particularly the responsiveness of inflation to changes in the interest rate. Based on the above scenario, a key difference between what they asked last year and this year is...? Last year they asked for a conditional forecast and this year for an unconditional forecast Last year Innovation uncertainty was important, but this year it is not Last year parameter instability was important. but this year it is not Last year they asked for an unconditional forecast and this year for a conditional forecast19 In a forecasting model, where y is a function of x1, x2. x3, and lagged values of y. we have a problem creating forecasts because the model you have estimated includes only contemporaneous values of x1, x2. and x3. Which of the following is not a way to handle this problem? We could create AR models of each of these variables and use forecasts from these univariate models in our forecasts We could lag each of these variables by one period We could lag each of these variables by more than one period Sample from the historical distribution of values of the variables and insert those values into equation for the out of sample forecast terms

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts