Question: 1a) Graph the final payoff and value prior to expiry of the following portfolio: Long underlying stock purchased at price S0=100 Long put option at

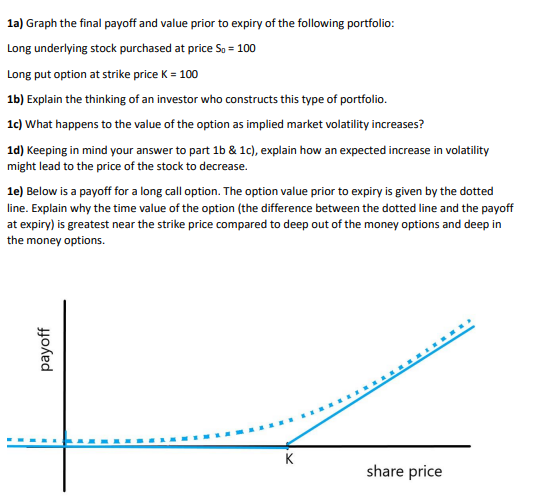

1a) Graph the final payoff and value prior to expiry of the following portfolio: Long underlying stock purchased at price S0=100 Long put option at strike price K=100 1b) Explain the thinking of an investor who constructs this type of portfolio. 1c) What happens to the value of the option as implied market volatility increases? 1d) Keeping in mind your answer to part 1b \& 1c), explain how an expected increase in volatility might lead to the price of the stock to decrease. 1e) Below is a payoff for a long call option. The option value prior to expiry is given by the dotted line. Explain why the time value of the option (the difference between the dotted line and the payoff at expiry) is greatest near the strike price compared to deep out of the money options and deep in the money options

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts