Question: 1.(i) Describe why the raw data gathered from a mortality investigation need to be graduated. [3] (ii) Explain which method of graduation would be most

Explain which method of graduation would be most](https://s3.amazonaws.com/si.experts.images/answers/2024/06/6677ca029a89c_5306677ca027d5af.jpg)

1.(i) Describe why the raw data gathered from a mortality investigation need to be

graduated. [3]

(ii) Explain which method of graduation would be most suitable for each of the

following mortality investigations:

(a) the female population of a large European country

(b) a study of the mortality of rhinoceroses in the safari parks of South

Africa

(c) the pension scheme of a large company [3]

2.

![safari parks of SouthAfrica(c) the pension scheme of a large company [3]](https://s3.amazonaws.com/si.experts.images/answers/2024/06/6677ca03a588b_5316677ca038deee.jpg)

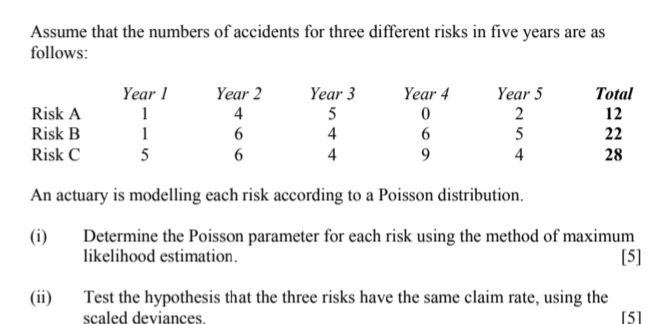

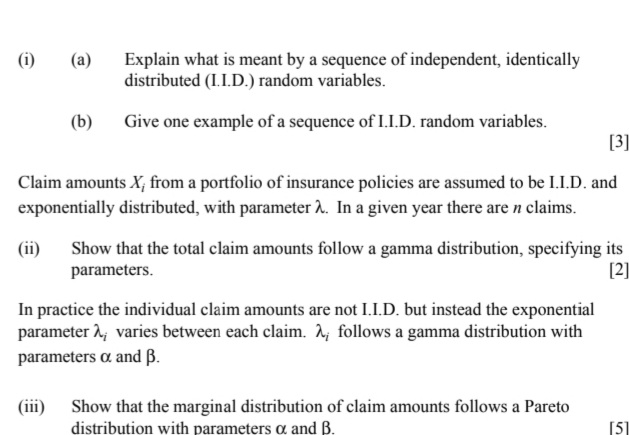

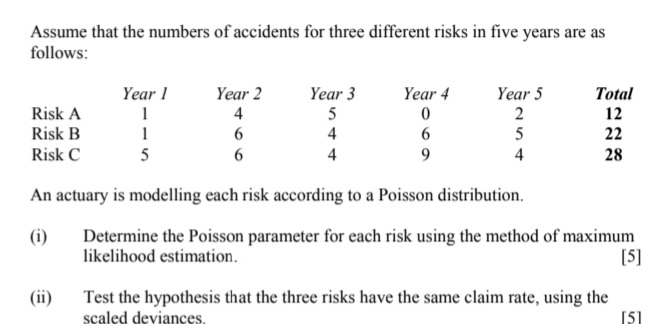

(i) (a) Explain what is meant by a sequence of independent, identically distributed (I.I.D.) random variables. (b ) Give one example of a sequence of I.I.D. random variables. [3] Claim amounts X, from a portfolio of insurance policies are assumed to be I.I.D. and exponentially distributed, with parameter 2. In a given year there are n claims. (ii) Show that the total claim amounts follow a gamma distribution, specifying its parameters. [2 In practice the individual claim amounts are not I.I.D. but instead the exponential parameter 2, varies between each claim. 2, follows a gamma distribution with parameters o and B. (iii) Show that the marginal distribution of claim amounts follows a Pareto distribution with parameters o and B.Assume that the numbers of accidents for three different risks in five years are as follows: Year I Year 2 Year 3 Year 4 Year 5 Total Risk A 5 12 Risk B AUN UI = = 4 22 Risk C 28 An actuary is modelling each risk according to a Poisson distribution. (i) Determine the Poisson parameter for each risk using the method of maximum likelihood estimation. [5] (ii) Test the hypothesis that the three risks have the same claim rate, using the scaled deviances. [5]Claim amounts, X, arising from a portfolio of insurance policies follow a Pareto distribution, with parameters o and 2.. The insurance company has bought excess of loss reinsurance cover, with retention M > 0. The reinsurer only has a record of claims greater than M. Consider the truncated distribution of claim amounts, Z = X -M| X> M. (i) Show that Z also follows a Pareto distribution, but with parameters of and 2 + M. [4]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts