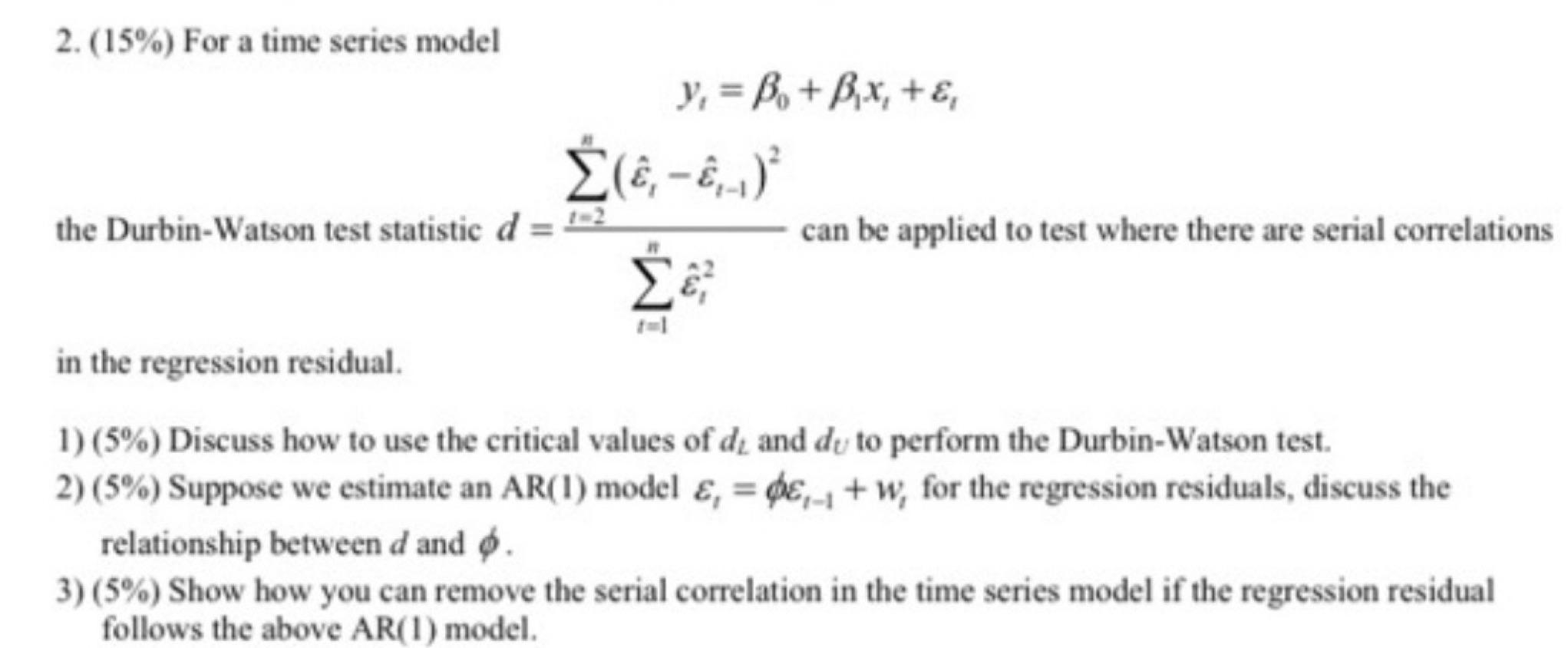

Question: 2. (15%) For a time series model the Durbin-Watson test statistic d y = B + Bx + (,-,.,) can be applied to test

2. (15%) For a time series model the Durbin-Watson test statistic d y = B + Bx + (,-,.,) can be applied to test where there are serial correlations in the regression residual. 1) (5%) Discuss how to use the critical values of de and de to perform the Durbin-Watson test. 2) (5%) Suppose we estimate an AR(1) model , =de,+w, for the regression residuals, discuss the relationship between d and . 3) (5%) Show how you can remove the serial correlation in the time series model if the regression residual follows the above AR(1) model.

Step by Step Solution

3.34 Rating (166 Votes )

There are 3 Steps involved in it

1 To perform the DurbinWatson test you compare the calculated DurbinWatson statistic d to the critic... View full answer

Get step-by-step solutions from verified subject matter experts