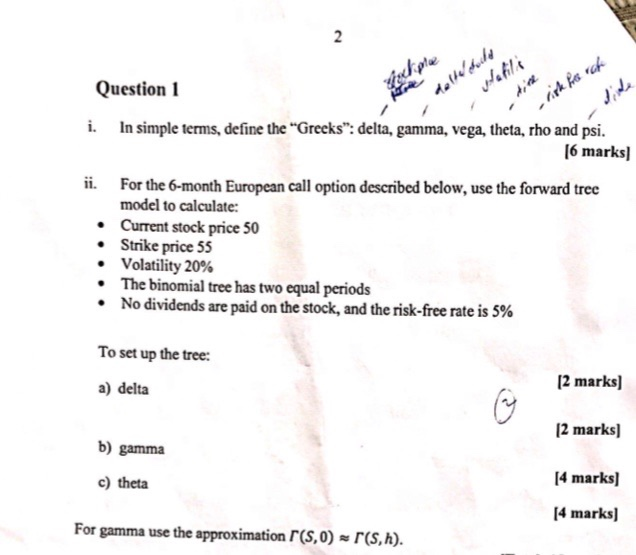

Question: 2 2 -risk forch Question 1 i. In simple terms, define the Greeks: delta, gamma, vega, theta, rho and psi. [6 marks) ii. For the

2 2 -risk forch Question 1 i. In simple terms, define the "Greeks: delta, gamma, vega, theta, rho and psi. [6 marks) ii. For the 6-month European call option described below, use the forward tree model to calculate: Current stock price 50 Strike price 55 Volatility 20% The binomial tree has two equal periods No dividends are paid on the stock, and the risk-free rate is 5% To set up the tree: a) delta [2 marks) [2 marks] b) gamma c) theta [4 marks] [4 marks) For gamma use the approximation r(s, 0) (sh)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock