Question: 2. (20 points) Write a pseudo-code for pricing the European call option at t = 0 by the Monte Carlo method. Implement the pseudo-code by

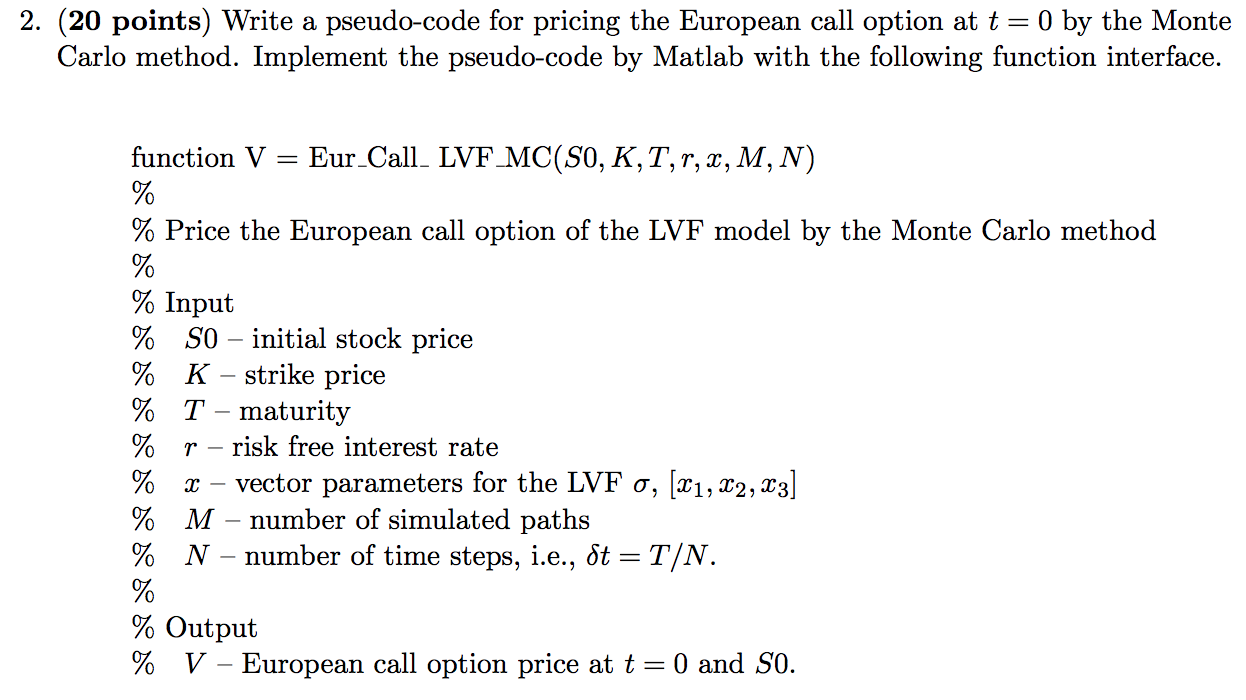

2. (20 points) Write a pseudo-code for pricing the European call option at t = 0 by the Monte Carlo method. Implement the pseudo-code by Matlab with the following function interface. function V Eur_Call. LVF_MC(SO,K,T,r, x, M, N) % % Price the European call option of the LVF model by the Monte Carlo method % % Input % SO initial stock price % K strike price % T - maturity % p- risk free interest rate % X vector parameters for the LVF o, [21, 22, 23] % M number of simulated paths % N number of time steps, i.e., St=T/N. % % Output % V - European call option price at t = 0 and SO

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock