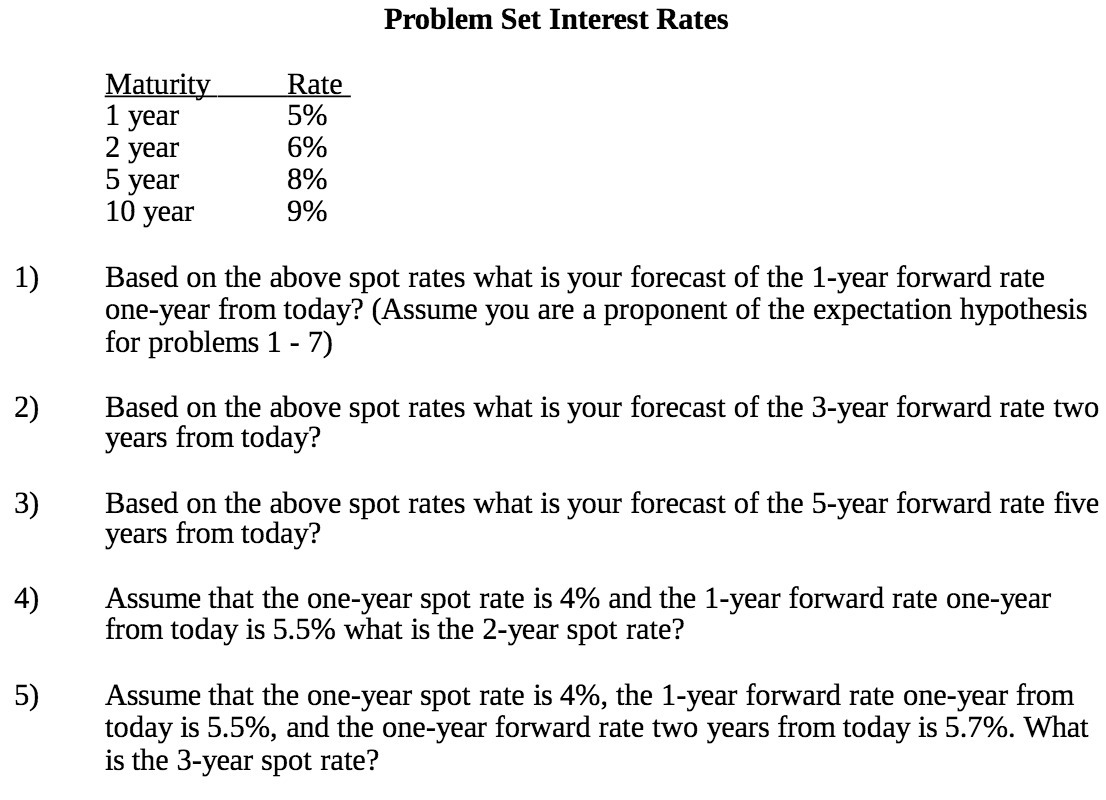

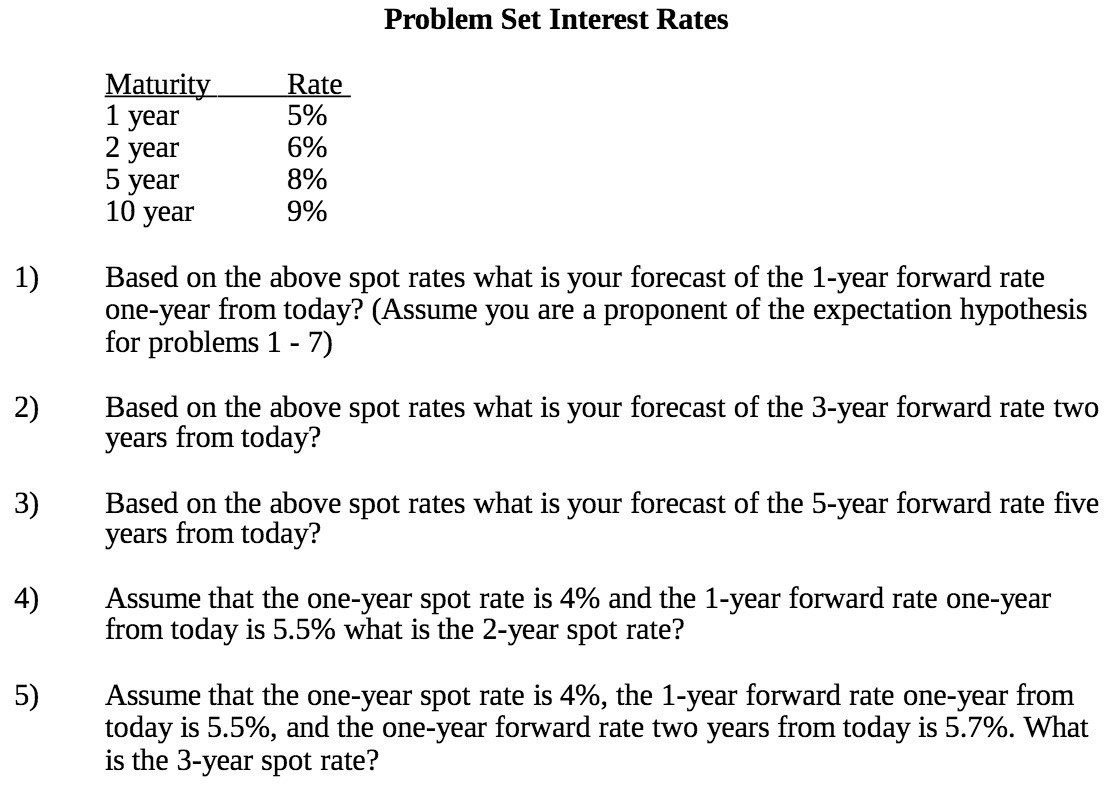

Question: 2) 3) 4) 5) Problem Set Interest Rates Maturity Rate 1 year 5% 2 year 6% 5 year 8% 10 year 9% Based on the

2) 3) 4) 5) Problem Set Interest Rates Maturity Rate 1 year 5% 2 year 6% 5 year 8% 10 year 9% Based on the above spot rates what is your forecast of the 1-year forward rate one-year from today? (Assume you are a proponent of the expectation hypothesis for problems 1 - 7) Based on the above spot rates what is your forecast of the 3-year forward rate two years from today? Based on the above spot rates what is your forecast of the 5-year forward rate ve years from today? Assume that the one-year spot rate is 4% and the 1-year forward rate one-year from today is 5.5% what is the 2-year spot rate? Assume that the one-year spot rate is 4%, the 1-year forward rate one-year from today is 5.5%, and the one-year forward rate two years from today is 5.7%. What is the 3-year spot rate

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts