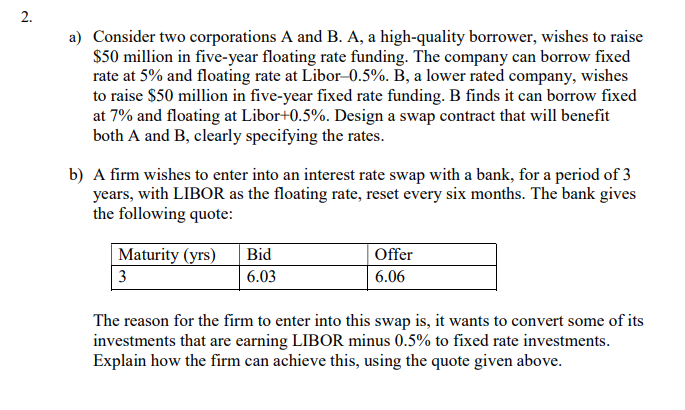

Question: 2. a) Consider two corporations A and B. A, a high-quality borrower, wishes to raise $50 million in five-year floating rate funding. The company can

2. a) Consider two corporations A and B. A, a high-quality borrower, wishes to raise $50 million in five-year floating rate funding. The company can borrow fixed rate at 5% and floating rate at Libor-0.5%. B, a lower rated company, wishes to raise $50 million in five-year fixed rate funding. B finds it can borrow fixed at 7% and floating at Libor+0.5%. Design a swap contract that will benefit both A and B, clearly specifying the rates. b) A firm wishes to enter into an interest rate swap with a bank, for a period of 3 years, with LIBOR as the floating rate, reset every six months. The bank gives the following quote: Maturity (yrs) 3 Bid 6.03 Offer 6.06 The reason for the firm to enter into this swap is, it wants to convert some of its investments that are earning LIBOR minus 0.5% to fixed rate investments. Explain how the firm can achieve this, using the quote given above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts