Question: (2) A security market line (SML) is given in the diagram below, where M is the market portfolio and the slope is 0.1. If we

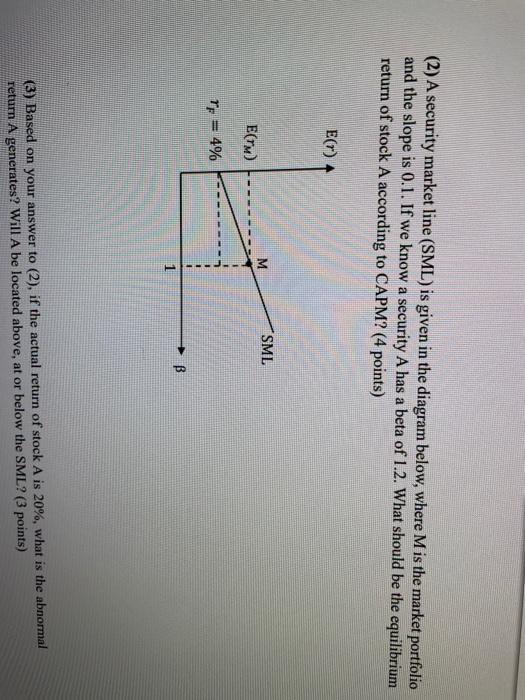

(2) A security market line (SML) is given in the diagram below, where M is the market portfolio and the slope is 0.1. If we know a security A has a beta of 1.2. What should be the equilibrium return of stock A according to CAPM? (4 points) E() M SML E(TM) TF = 4% B 1 (3) Based on your answer to (2), if the actual return of stock A is 20%, what is the abnormal return A generates? Will A be located above, at or below the SML? (3 points)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock