Question: 2 ACCOUNTING ACTIVITY!! Please check the comment section. I pasted there the google drive link where the TWO activity and instruction can be seen. (Hey

2 ACCOUNTING ACTIVITY!!

Please check the comment section. I pasted there the google drive link where the TWO activity and instruction can be seen.

(Hey Tutors! Please answer the two activity given in the comment section!! I will leave a google drive link there!! I'm really having a hard time with it!! THANK YOU!!!)

FOR REFERENCES:

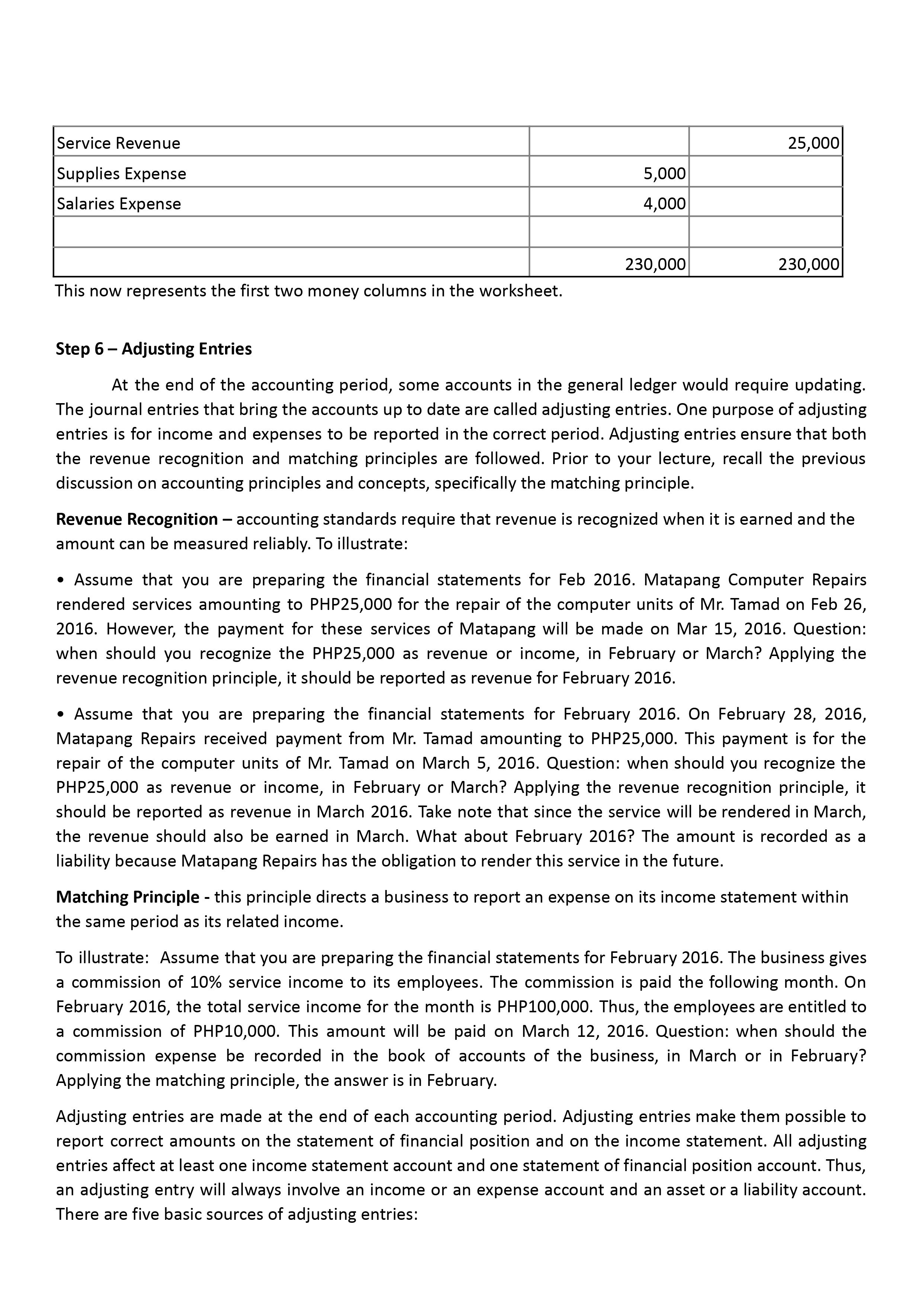

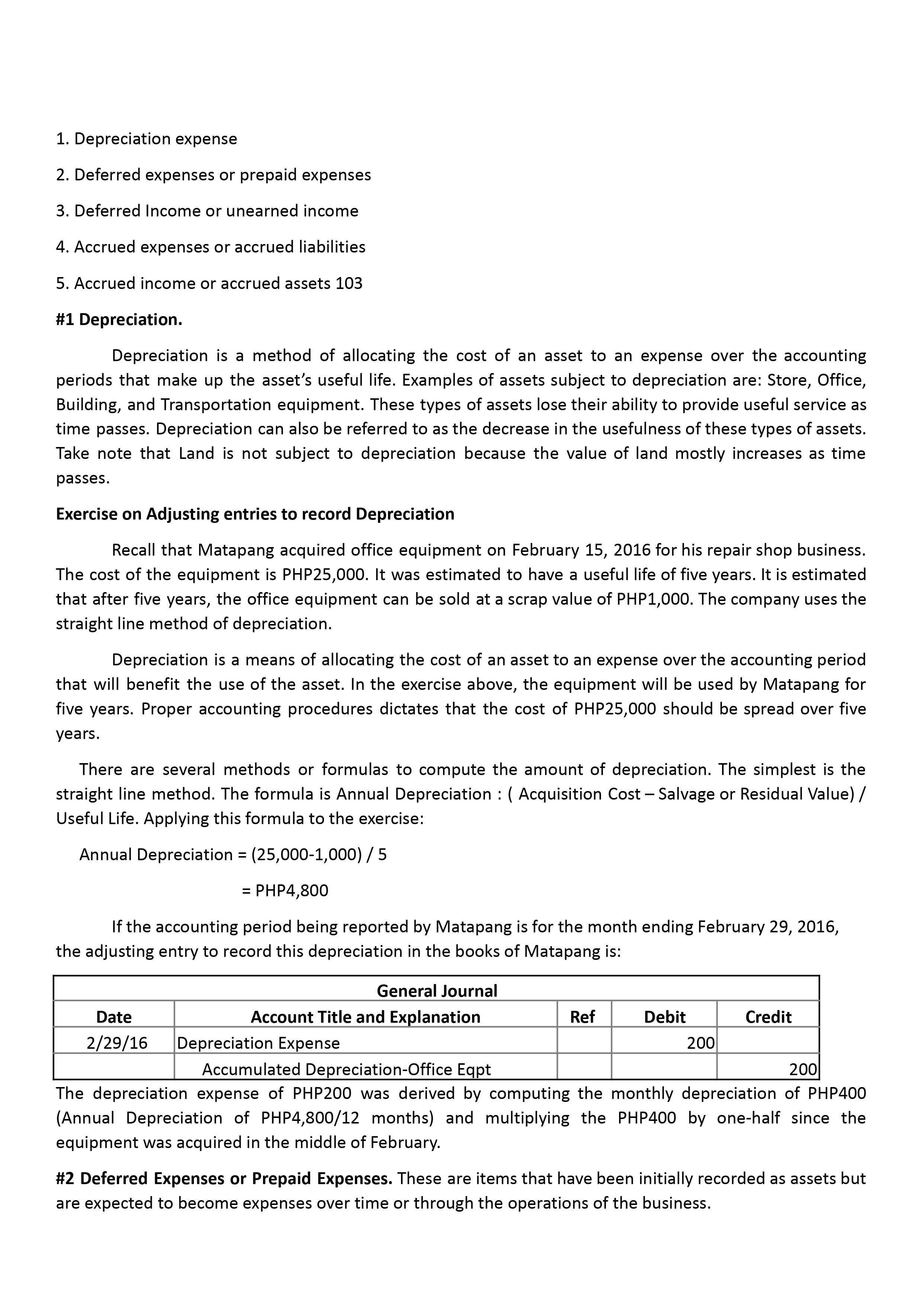

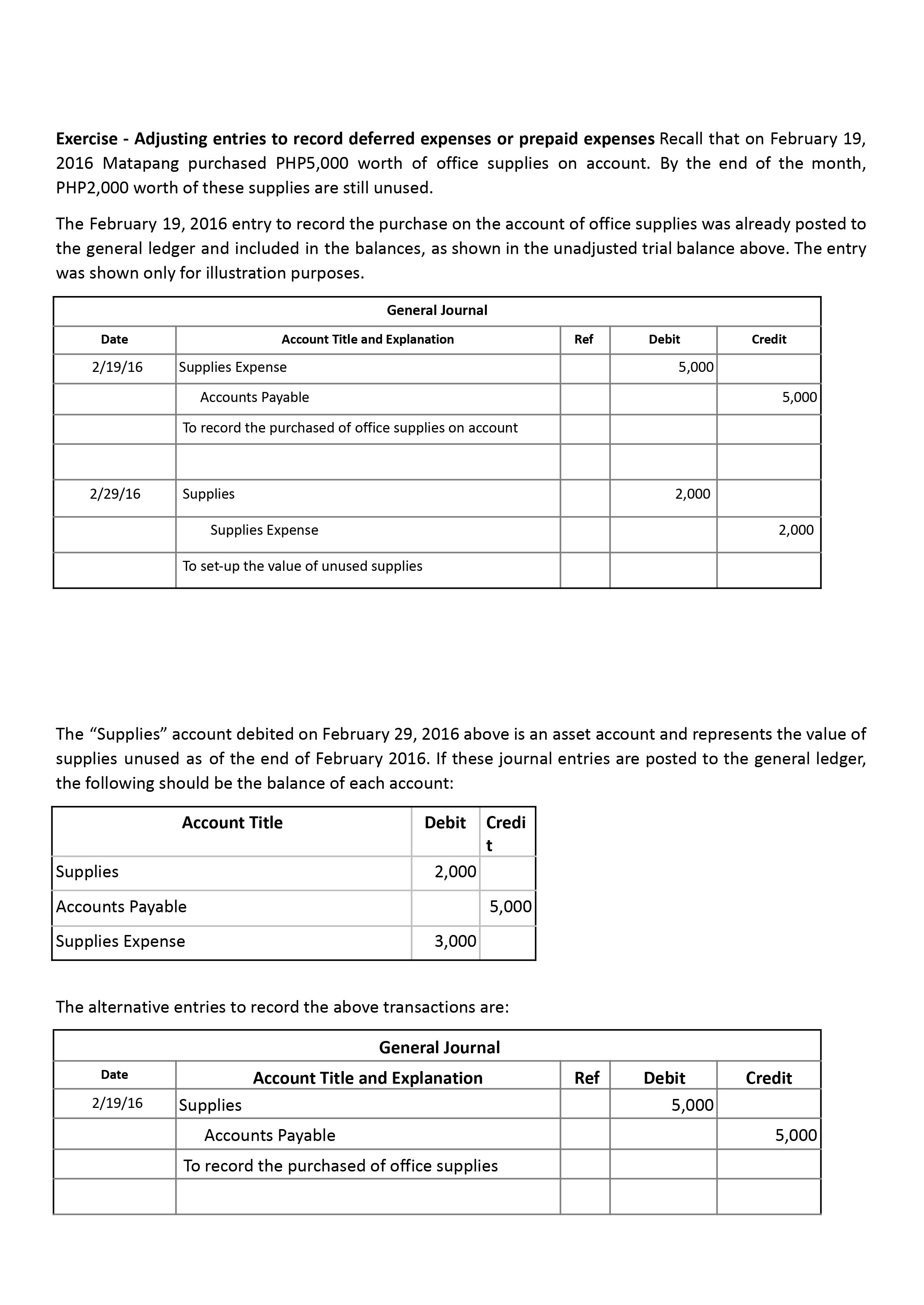

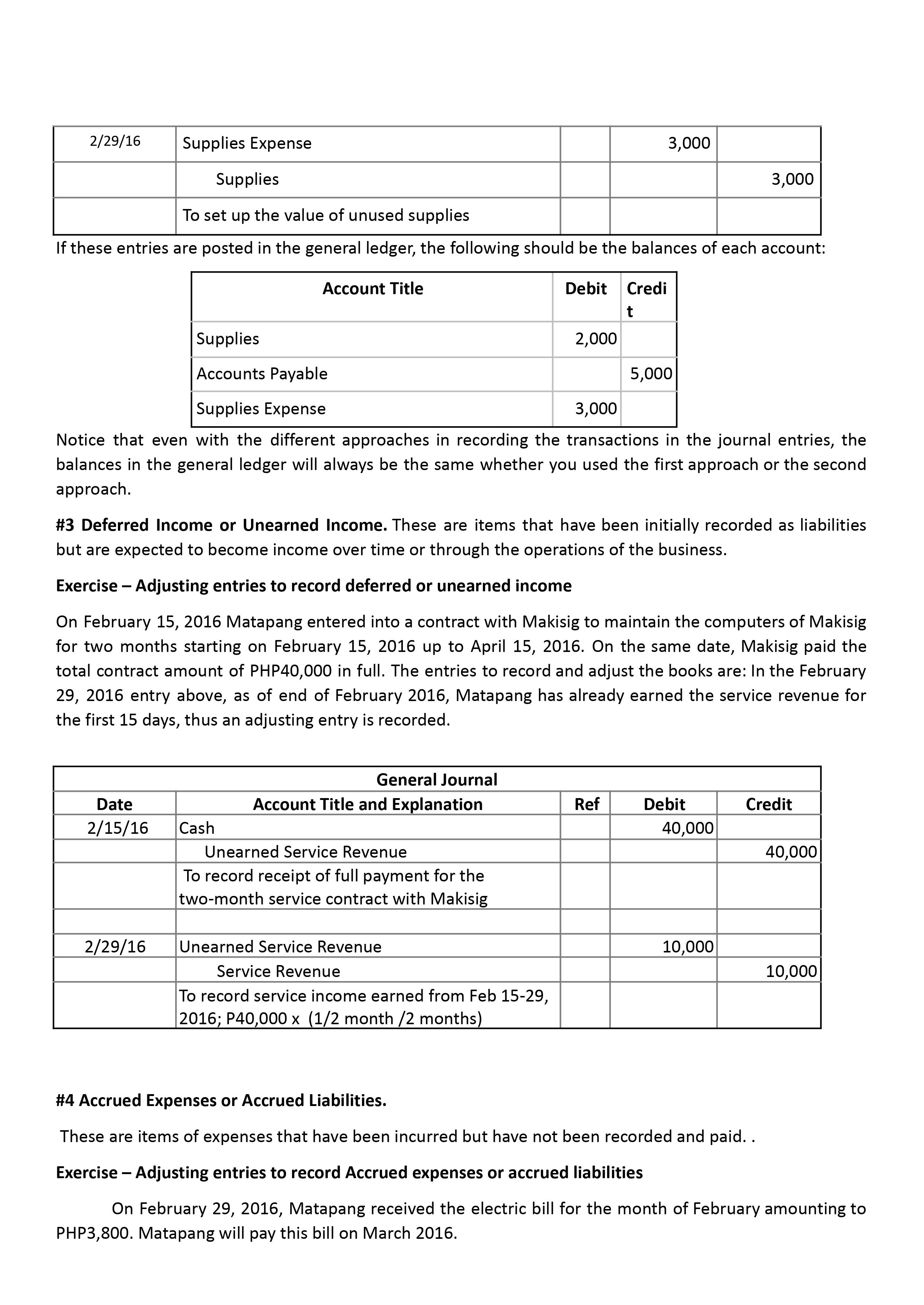

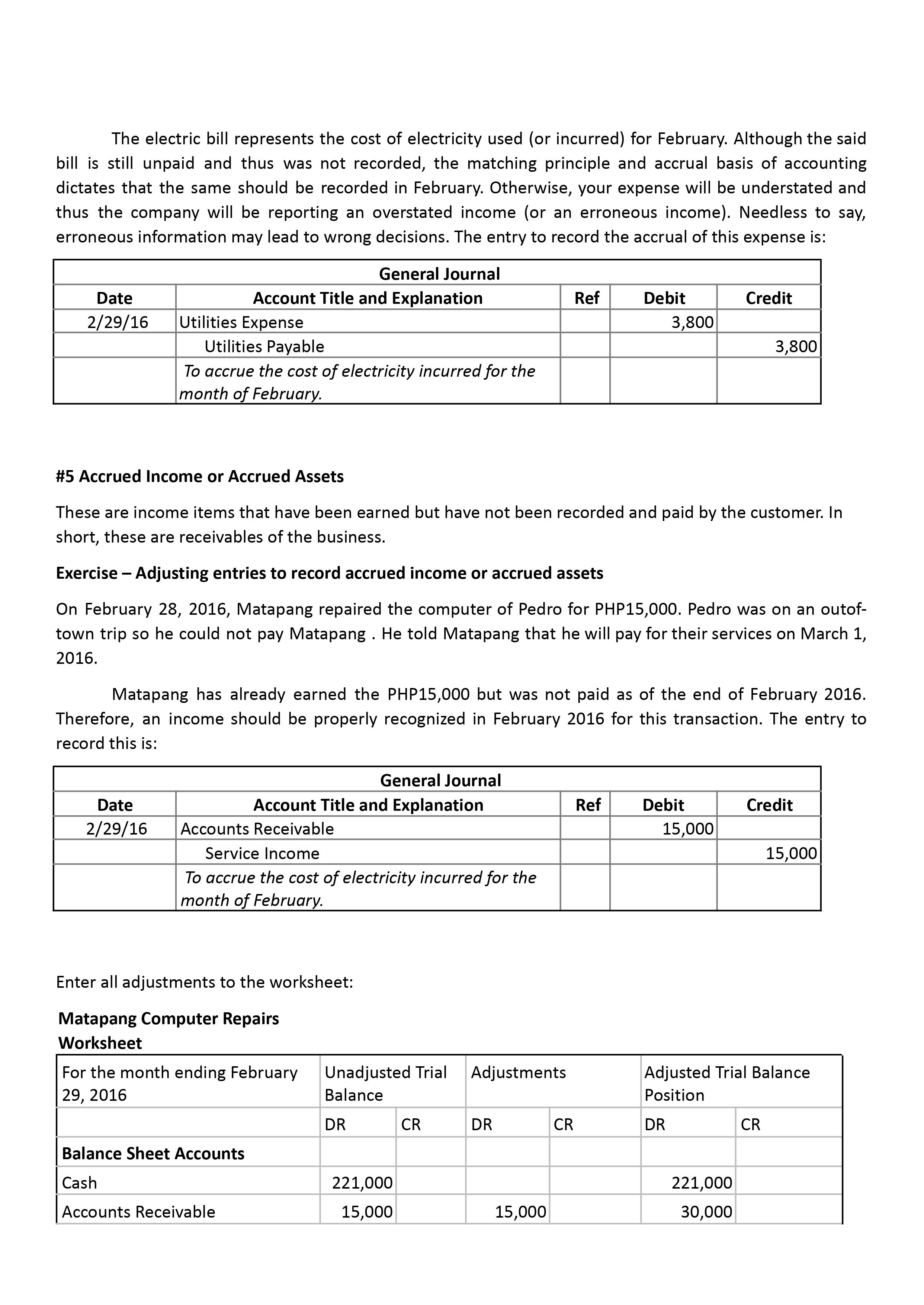

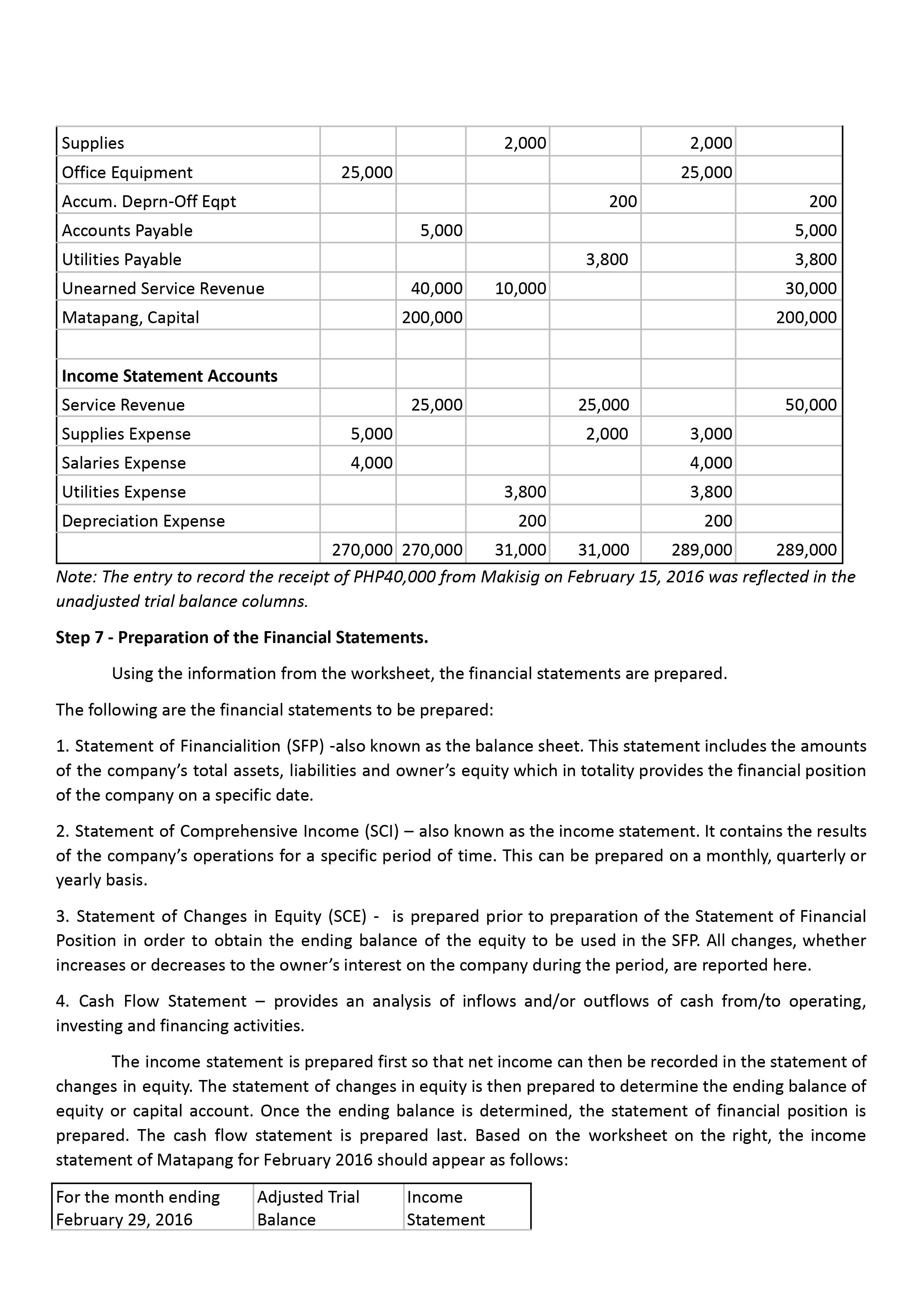

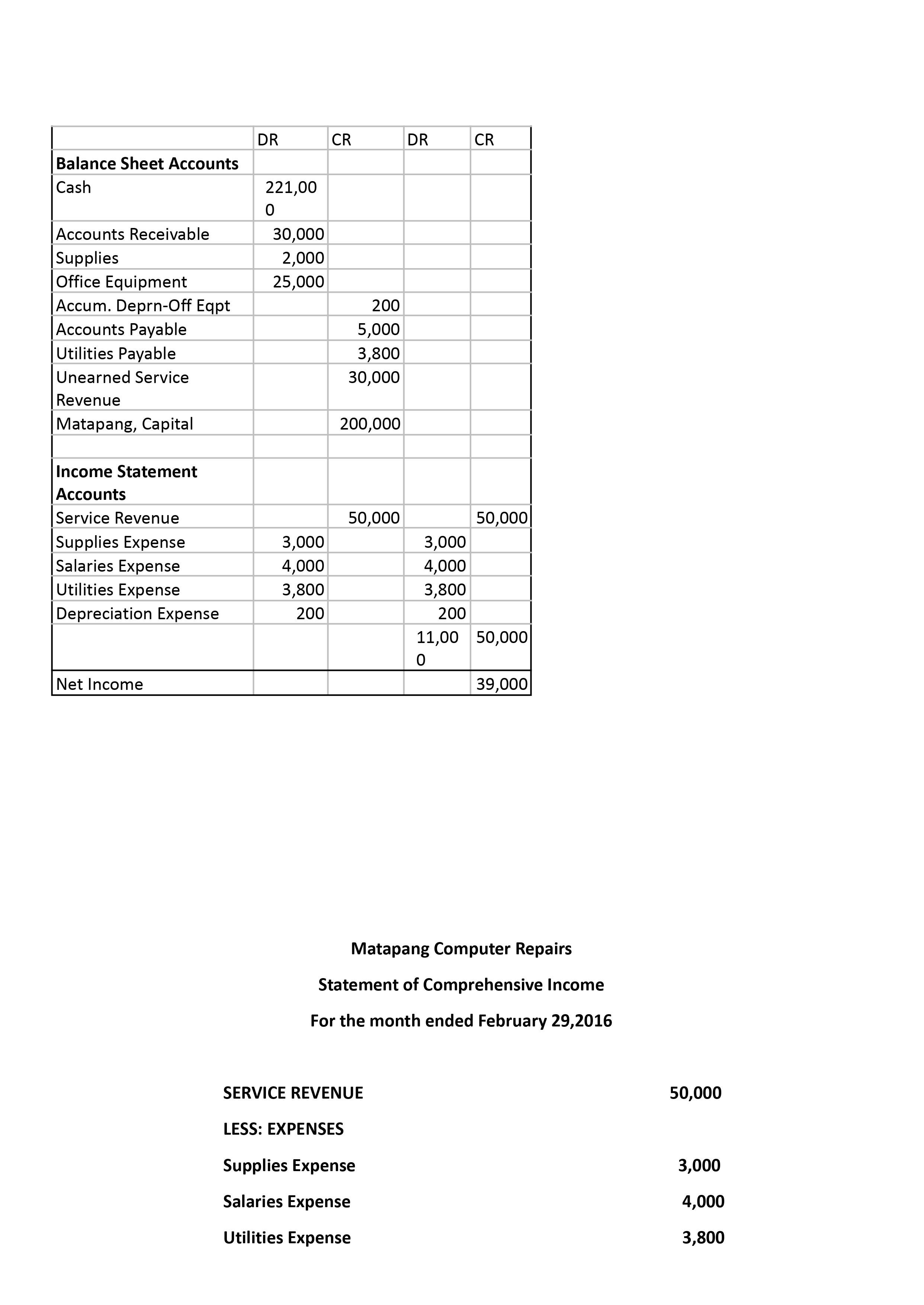

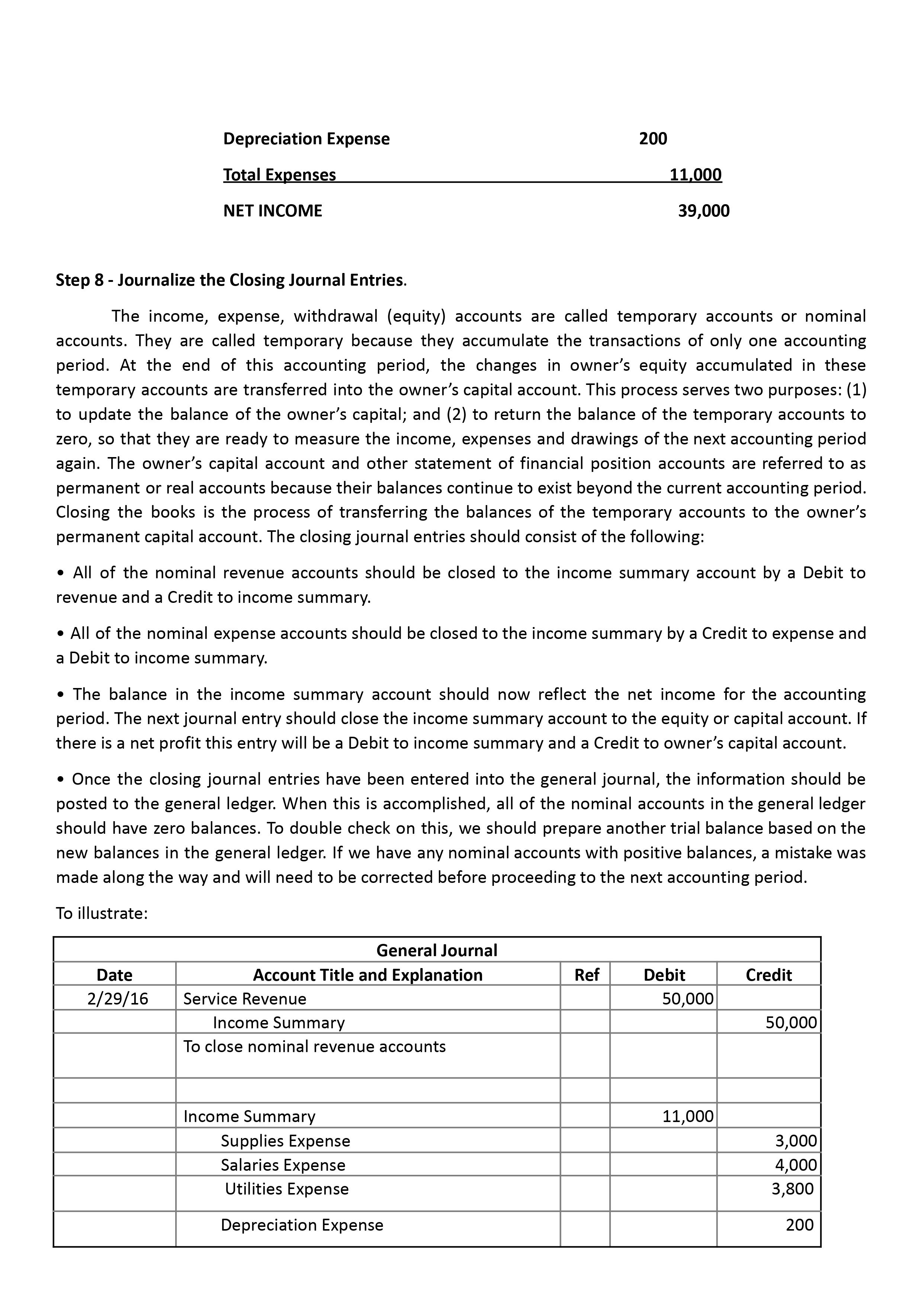

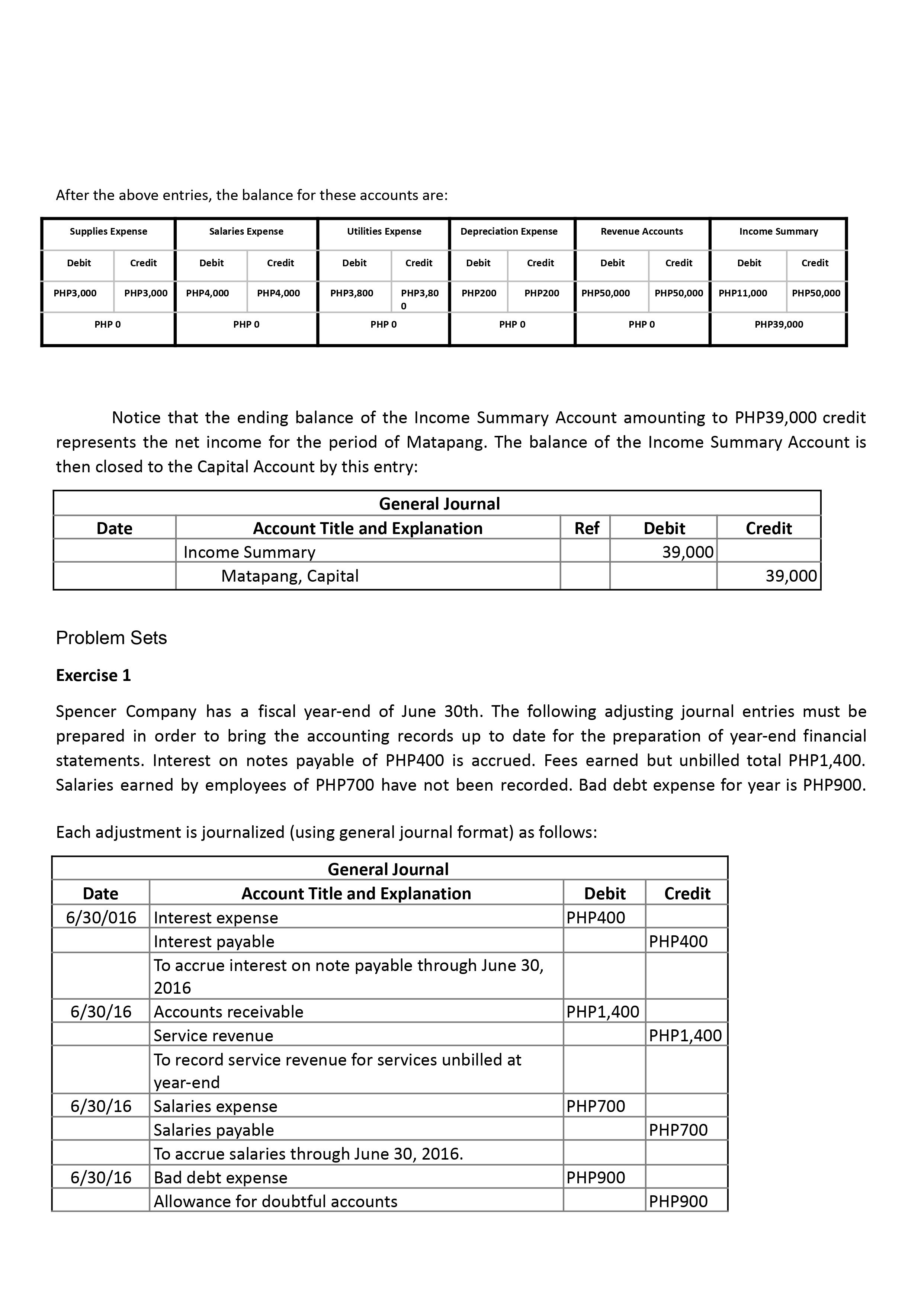

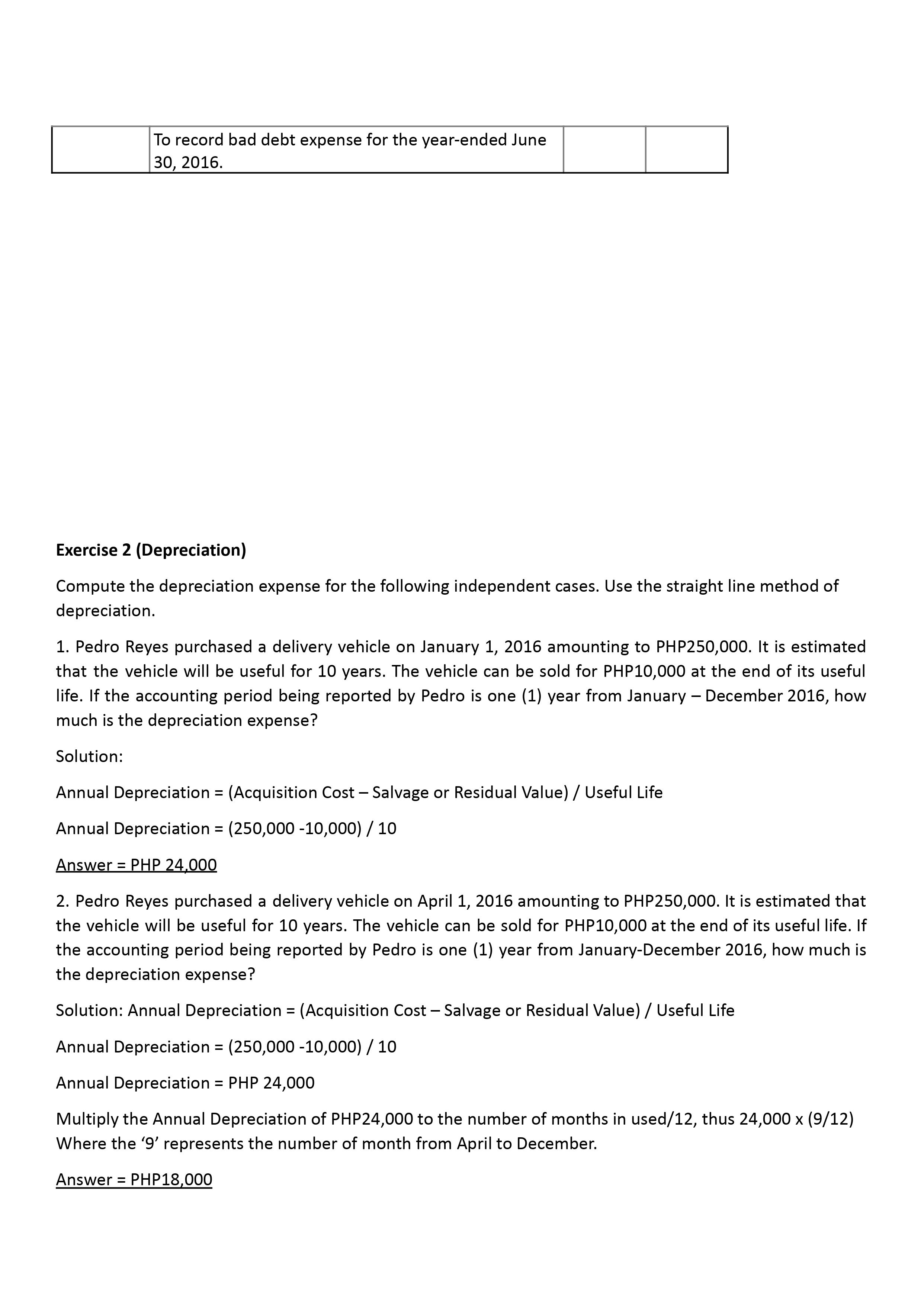

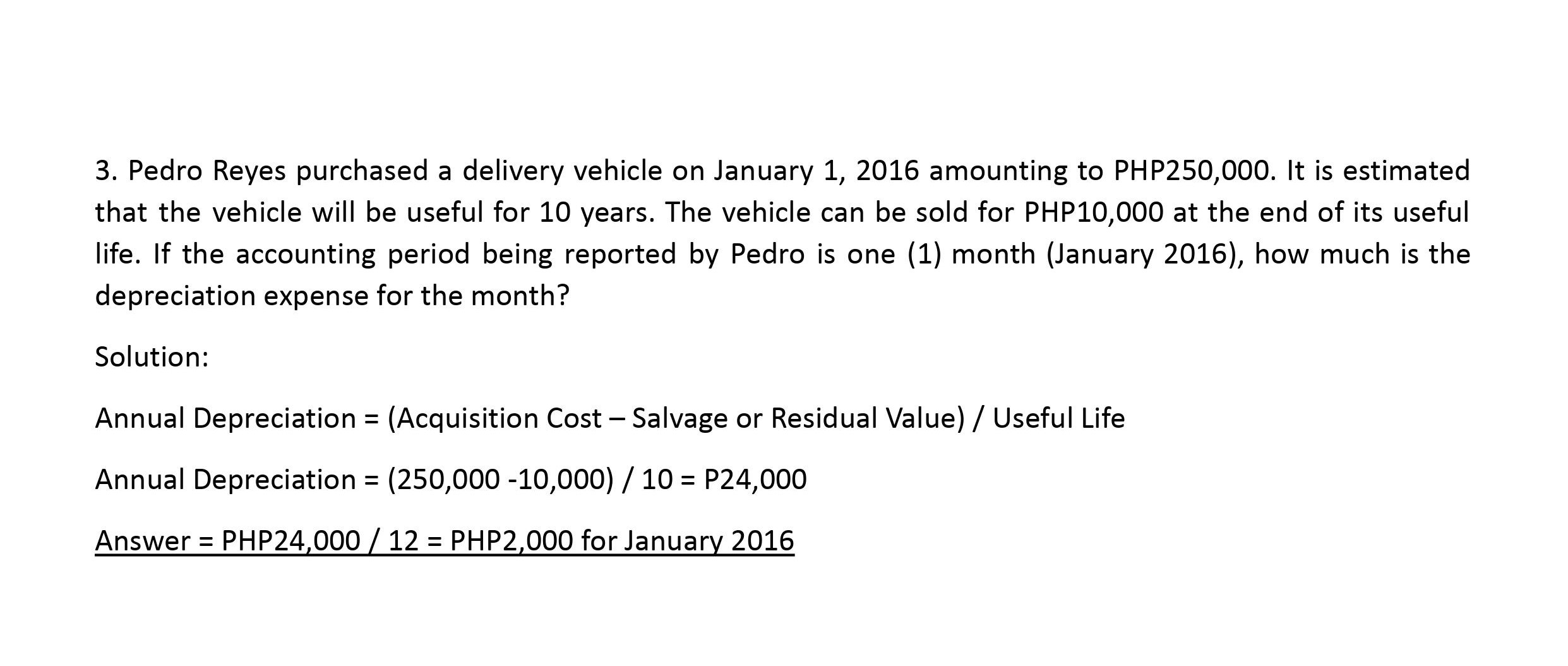

THE ACCOUNTING CYCLE Step 5 - Worksheet This step is simply about plotting the items in the unadjusted trial balance on the worksheet. In a manual accounting system, a worksheet is a large columnar sheet of paper specifically designed to conveniently arrange all the accounting information required at the end of a period. The worksheet is used to check whether ledger accounts are balanced and adjusted. The satisfactory completion of a worksheet provides assurance that all the details of the end-ofperiod accounting procedures were properly brought together. The worksheet serves as the source in the preparation of financial statements and other closing and adjusting entries. The body of the worksheet contains five pairs of money columns. A sample of a worksheet is shown below: Name of the Company Worksheet For the period (monthy/year) ended Unadjusted Adjustments Adjusted Trial Statement Statement Trial Balance Balance of Income of Financial Position Owner's, Withdrawal Income Statement Accounts Sales Sales Returns and Allowances Sales Discounts Interestlncome --------- purchases --------- Purchase Returns and Allowances Purchase Discounts Freight In Salaries Expense Supplies Expense Utilities Expense Recall our example in Module 7, about Pedro Matapang who started his Matapang Computer Repairs business on February 14, 2016. The following transactions transpired in February 2016: 1. February 14, 2016 - Pedro Matapang invested PHP200,000 into his Matapang Computer Repair business. 2. February 15, 2016 - Pedro purchased one computer unit from XY Computer Store to be used for his business. He issued check number 001 amounting to PHP25,000. 3. February 16, 2016 - Pedro hired Juana Magaling, an experienced secretary. 4. February 17, 2016 - Repaired the computer of Jean and collected PHP10,000. 5. February 18, 2016 - Repaired the computer of Mike; however, Mike will pay PHP15,000 only on March 18, 2016. 6. February 19, 2016 - Pedro purchased Office Supplies from MM Merchandise amounting to PHP5,000 on account. Pedro will pay this on March 30, 2016. 7. February 25, 2016 - Paid the salary of Juana amounting to PHP4,000. The entries to record the above transactions are on the right: 2016. The following transactions transpired in February 2016: 1. February 14, 2016 - Pedro Matapang invested PHP200,000 into his Matapang Computer Repair business. 2. February 15, 2016 - Pedro purchased one computer unit from XY Computer Store to be used for his business. He issued check number 001 amounting to PHP25,000 3. February 16, 2016 - Pedro hired Juana Magaling, an experienced secretary 4. February 17, 2016 - Repaired the computer of Jean and collected PHP10,000.5. February 18, 2016 - Repaired the computer of Mike; however, Mike will pay PHP15,000 only on March 18, 2016. 6. February 19, 2016 - Pedro purchased Office Supplies from MM Merchandise amounting to PHP5,000 on account. Pedro will pay this on March 30, 2016. 7. February 25, 2016 - Paid the salary of Juana amounting to PHP4,000. The entries to record the above transactions are on below: General Journal Date Account Title and Explanation Ref Debit Credit 2/14/16 Cash 200,00 0 Matapang, Capital 200,00 0 To record the initial investment of owner P. Matapang 2/15/16 Office Equipment 25,000 Cash 25,000 To record the purchase of 1 computer unit 2/17/16 Cash 10,000 Service Revenue 10,000 To record receipt of cash from customer 2/18/16 Accounts Receivable 15,000 Service Revenue 15,000 To record services rendered to a customer on account 2/19/16 Supplies Expense 5,000 Accounts Payable 5,000 To record purchase of office supplies on account 2/25/16 Salaries Expense 4,000 Cash 4,000 To record payment of salary of JuanaRecall that after posting to the general ledger, the unadjusted trial balance was: MATAPANG COMPUTER REPAIRS Unadjusted Trial Balance February 29, 2016 Account Title Debit Credit Balance Sheet Accounts Cash 181,000 Accounts Receivable 15,000 Office Equipment 25,000 Accounts Payable 5,000 Matapang, Capital 200,000 Income Statement Accounts 25.000 Supplies Expense 5,000 Salaries Expense 4,000 230,000 230,000 This now represents the first two money columns in the worksheet. Step 6 Adjusting Entries At the end of the accounting period, some accounts in the general ledger would require updating. The journal entries that bring the accounts up to date are called adjusting entries. One purpose of adjusting entries is for income and expenses to be reported in the correct period. Adjusting entries ensure that both the revenue recognition and matching principles are followed. Prior to your lecture, recall the previous discussion on accounting principles and concepts, specifically the matching principle. Revenue Recognition accounting standards require that revenue is recognized when it is earned and the amount can be measured reliably. To illustrate: - Assume that you are preparing the financial statements for Feb 2016. Matapang Computer Repairs rendered services amounting to PHP25,000 for the repair of the computer units of Mr. Tamad on Feb 26, 2016. However, the payment for these services of Matapang will be made on Mar 15, 2016. Question: when should you recognize the PHP25,000 as revenue or income, in February or March? Applying the revenue recognition principle, it should be reported as revenue for February 2016. 0 Assume that you are preparing the financial statements for February 2016. On February 28, 2016, Matapang Repairs received payment from Mr. Tamad amounting to PHP25,000. This payment is for the repair of the computer units of Mr. Tamad on March 5, 2016. Question: when should you recognize the PHP25,000 as revenue or income, in February or March? Applying the revenue recognition principle, it should be reported as revenue in March 2016. Take note that since the service will be rendered in March, the revenue should also be earned in March. What about February 2016? The amount is recorded as a liability because Matapang Repairs has the obligation to render this service in the future. Matching Principle - this principle directs a business to report an expense on its income statement within the same period as its related income. To illustrate: Assume that you are preparing the financial statements for February 2016. The business gives a commission of 10% service income to its employees. The commission is paid the following month. On February 2016, the total service income for the month is PHP100,000. Thus, the employees are entitled to a commission of PHP10,000. This amount will be paid on March 12, 2016. Question: when should the commission expense be recorded in the book of accounts of the business, in March or in February? Applying the matching principle, the answer is in February. Adjusting entries are made at the end of each accounting period. Adjusting entries make them possible to report correct amounts on the statement of financial position and on the income statement. All adjusting entries affect at least one income statement account and one statement of financial position account. Thus, an adjusting entry will always involve an income or an expense account and an asset or a liability account. There are five basic sources of adjusting entries: 1. Depreciation expense 2. Deferred expenses or prepaid expenses 3. Deferred Income or unearned income 4. Accrued expenses or accrued liabilities 5. Accrued income or accrued assets 103 #1 Depreciation. Depreciation is a method of allocating the cost of an asset to an expense over the accounting periods that make up the asset's useful life. Examples of assets subject to depreciation are: Store, Office, Building, and Transportation equipment. These types of assets lose their ability to provide useful service as time passes. Depreciation can also be referred to as the decrease in the usefulness ofthese types of assets. Take note that Land is not subject to depreciation because the value of land mostly increases as time passes. Exercise on Adjusting entries to record Depreciation Recall that Matapang acquired office equipment on February 15, 2016 for his repair shop business. The cost of the equipment is PHP25,000. It was estimated to have a useful life of five years. It is estimated that after five years, the office equipment can be sold at a scrap value of PHP1,000. The company uses the straight line method of depreciation. Depreciation is a means of allocating the cost of an asset to an expense over the accounting period that will benefit the use of the asset. In the exercise above, the equipment will be used by Matapang for five years. Proper accounting procedures dictates that the cost of PHP25,000 should be spread over five years. There are several methods or formulas to compute the amount of depreciation. The simplest is the straight line method. The formula is Annual Depreciation : ( Acquisition Cost Salvage or Residual Value)/ Useful Life. Applying this formula to the exercise: Annual Depreciation = (25,000-1,000) / 5 = PH P4,800 If the accounting period being reported by Matapang is for the month ending February 29, 2016, the adjusting entry to record this depreciation in the books of Matapang is: General Journal Account Title and Ex . lanation Credit 2/29/16 Depreciation Expense -_ Accumulated Depreciation-Office Eqpt -_ The depreciation expense of PHPZOO was derived by computing the monthly depreciation 02f0 PHP400 (Annual Depreciation of PHP4,800/12 months) and multiplying the PHP400 by one-half since the equipment was acquired in the middle of February. #2 Deferred Expenses or Prepaid Expenses. These are items that have been initially recorded as assets but are expected to become expenses over time or through the operations of the business. Exercise - Adjusting entries to record deferred expenses or prepaid expenses Recall that on February 19, 2016 Matapang purchased PHP5,000 worth of office supplies on account. By the end of the month, PHP2,000 worth of these supplies are still unused. The February 19, 2016 entry to record the purchase on the account of office supplies was already posted to the general ledger and included in the balances, as shown in the unadjusted trial balance above. The entry was shown only for illustration purposes. General Journal Account Title and Explanation Ref 2/19/16 Supplies Expense Accounts Payable To record the purchased of office supplies on account 2/29/16 Supplies Supplies Expense To setup the value of unused supplies The \"Supplies\" account debited on February 29, 2016 above is an asset account and represents the value of supplies unused as of the end of February 2016. If these journal entries are posted to the general ledger, the following should be the balance of each account: _ _ To record the purchased of office supplies _ Supplies Expense _ To set up the value of unused supplies Account Title W Accounts Payable Supplies Expense 3,000 Notice that even with the different approaches in recording the transactions in the journal entries, the balances in the general ledger will always be the same whether you used the first approach or the second approach. #3 Deferred Income or Unearned lncome.These are items that have been initially recorded as liabilities but are expected to become income over time or through the operations of the business. Exercise Adjusting entries to record deferred or unearned income On February 15, 2016 Matapang entered into a contract with Makisig to maintain the computers of Makisig for two months starting on February 15, 2016 up to April 15, 2016. On the same date, Makisig paid the total contract amount of PHP40,000 in full. The entries to record and adjust the books are: In the February 29, 2016 entry above, as of end of February 2016, Matapang has already earned the service revenue for the first 15 days, thus an adjusting entry is recorded. General Journal Account Title and Explanation Credit 2/15/16 two-month service contract with Makisig 40,000 40,000 2/29/16 Unearned SerVIce Revenue To record service income earned from Feb 15-29, 2016; P40 000 x (1/2 month /2 months) #4 Accrued Expenses or Accrued Liabilities. 10,000 These are items of expenses that have been incurred but have not been recorded and paid. . Exercise Adjusting entries to record Accrued expenses or accrued liabilities On February 29, 2016, Matapang received the electric bill for the month of February amounting to PHP3,800. Matapang will pay this bill on March 2016. The electric bill represents the cost of electricity used (or incurred) for February. Although the said bill is still unpaid and thus was not recorded, the matching principle and accrual basis of accounting dictates that the same should be recorded in February. Otherwise, your expense will be understated and thus the company will be reporting an overstated income (or an erroneous income). Needless to say, erroneous information may lead to wrong decisions. The entry to record the accrual of this expense is: General Journal m Account Title and Explanation mm Credit 2/29/16 Utilities Expense - 3,800 _ Utilities Payable -_ 3.800 To accrue the cost of electricity incurred for the month a Februar . #5 Accrued Income or Accrued Assets These are income items that have been earned but have not been recorded and paid by the customer. In short, these are receivables of the business. Exercise Adjusting entries to record accrued income or accrued assets On February 28, 2016, Matapang repaired the computer of Pedro for PHP15,000. Pedro was on an outof town trip so he could not pay Matapang . He told Matapang that he will pay for their services on March 1, 2016. Matapang has already earned the PHP15,000 but was not paid as of the end of February 2016. Therefore, an income should be properly recognized in February 2016 for this transaction. The entry to record this is: General Journal Account Title and Explanation Accounts Receivable SerVIce Income To accrue the cost of electricity incurred for the month of February. Enter all adjustments to the worksheet: Matapang Computer Repairs Worksheet For the month ending February Unadjusted Trial Adjustments Adjusted Trial Balance 29 2016 Balance Position Iil---_Iil-Iil_ Balance Sheet Accounts --_ 221.000 -_ 221,000 Accounts Receivable 15,000 15,000 30,000 Unearned Service Revenue Matapang, Capital Income Statement Accounts 270,000 270,000 Note: The entry to record the receipt of PHP40,000 from Makisig on February 15, 2016 was reflected in the unadjusted trial balance columns. Step 7 - Preparation of the Financial Statements. Using the information from the worksheet, the financial statements are prepared. The following are the financial statements to be prepared: 1. Statement of Financialition (SFP) -a|so known as the balance sheet. This statement includes the amounts of the company's total assets, liabilities and owner's equity which in totality provides the financial position of the company on a specific date. 2. Statement of Comprehensive Income (SCI) also known as the income statement. It contains the results of the company's operations for a specific period of time. This can be prepared on a monthly, quarterly or yearly basis. 3. Statement of Changes in Equity (SCE) - is prepared prior to preparation of the Statement of Financial Position in order to obtain the ending balance of the equity to be used in the SFP. All changes, whether increases or decreases to the owner's interest on the company during the period, are reported here. 4. Cash Flow Statement provides an analysis of inflows and/or outflows of cash from/to operating, investing and financing activities. The income statement is prepared first so that net income can then be recorded in the statement of changes in equity. The statement of changes in equity is then prepared to determine the ending balance of equity or capital account. Once the ending balance is determined, the statement of financial position is prepared. The cash flow statement is prepared last. Based on the worksheet on the right, the income statement of Matapang for February 2016 should appear as follows: For the month ending Adjusted Trial Income February 29, 2016 Balance Statement DR CR DR CR Balance Sheet Accounts Cash 221,00 0 Accounts Receivable 30,000 Supplies 2,000 Office Equipment 25,000 Accum. Deprn-Off Eqpt 200 Accounts Payable 5,000 Utilities Payable 3,800 Unearned Service 30,000 Revenue Matapang, Capital 200,000 Income Statement Accounts Service Revenue 50,000 50,000 Supplies Expense 3,000 3,000 Salaries Expense 4,000 4,000 Utilities Expense 3,800 3,800 Depreciation Expense 200 200 11,00 50,000 0 Net Income 39,000 Matapang Computer Repairs Statement of Comprehensive Income For the month ended February 29,2016 SERVICE REVENUE 50,000 LESS: EXPENSES Supplies Expense 3,000 Salaries Expense 4,000 Utilities Expense 3,800Depreciation Expense 200 Total Expenses 11.000 NET INCOME 39,000 Step 8 - Journalize the Closing Journal Entries. The income, expense, withdrawal (equity) accounts are called temporary accounts or nominal accounts. They are called temporary because they accumulate the transactions of only one accounting period. At the end of this accounting period, the changes in owner's equity accumulated in these temporary accounts are transferred into the owner's capital account. This process serves two purposes: (1) to update the balance of the owner's capital; and (2) to return the balance of the temporary accounts to zero, so that they are ready to measure the income, expenses and drawings of the next accounting period again. The owner's capital account and other statement of financial position accounts are referred to as permanent or real accounts because their balances continue to exist beyond the current accounting period. Closing the books is the process of transferring the balances of the temporary accounts to the owner's permanent capital account. The closing journal entries should consist of the following: 0 All of the nominal revenue accounts should be closed to the income summary account by a Debit to revenue and a Credit to income summary. 0 All of the nominal expense accounts should be closed to the income summary by a Credit to expense and a Debit to income summary. - The balance in the income summary account should now reflect the net income for the accounting period. The next journal entry should close the income summary account to the equity or capital account. If there is a net profit this entry will be a Debit to income summary and a Credit to owner's capital account. 0 Once the closing journal entries have been entered into the general journal, the information should be posted to the general ledger. When this is accomplished, all of the nominal accounts in the general ledger should have zero balances. To double check on this, we should prepare another trial balance based on the new balances in the general ledger. If we have any nominal accounts with positive balances, a mistake was made along the way and will need to be corrected before proceeding to the next accounting period. To illustrate: General Journal m Account Title and Ex . lanation Elm 2/29/16 - 50,000 -_ 50,000 - T cm "W\" --- - 11,000 Supplies Expense -_ 3,000 Salaries Expense - 4.000 After the above entries, the balance for these accounts are: Supplies Expense Salaries Expense Utilities Expense Depreciation Expense Revenue Account Income Summary Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit PHP3,000 PHP3,000 PHP4,000 PHP4,000 PHP3,800 PHP3,80 PHP200 PHP200 PHP50,000 PHP50,000 PHP11,000 PHP50,000 PHP 0 PHP 0 PHP 0 PHP 0 PHP 0 PHP39,000 Notice that the ending balance of the Income Summary Account amounting to PHP39,000 credit represents the net income for the period of Matapang. The balance of the Income Summary Account is then closed to the Capital Account by this entry: General Journal Date Account Title and Explanation Ref Debit Credit Income Summary 39,000 Matapang, Capital 39,000 Problem Sets Exercise 1 Spencer Company has a fiscal year-end of June 30th. The following adjusting journal entries must be prepared in order to bring the accounting records up to date for the preparation of year-end financial statements. Interest on notes payable of PHP400 is accrued. Fees earned but unbilled total PHP1,400. Salaries earned by employees of PHP700 have not been recorded. Bad debt expense for year is PHP900. Each adjustment is journalized (using general journal format) as follows: General Journal Date Account Title and Explanation Debit Credit 6/30/016 Interest expense PHP400 Interest payable PHP400 To accrue interest on note payable through June 30, 2016 6/30/16 Accounts receivable PHP1,400 Service revenue PHP1,400 To record service revenue for services unbilled at year-end 6/30/16 Salaries expense PHP700 Salaries payable PHP700 To accrue salaries through June 30, 2016. 6/30/16 Bad debt expense PHP900 Allowance for doubtful accounts PHP900To record bad debt expense for the year-ended June 30, 2016. Exercise 2 (Depreciation) Compute the depreciation expense for the following independent cases. Use the straight line method of depreciation. 1. Pedro Reyes purchased a delivery vehicle on January 1, 2016 amounting to PHP250,000. It is estimated that the vehicle will be useful for 10 years. The vehicle can be sold for PHP10,000 at the end of its useful life. If the accounting period being reported by Pedro is one (1) year from January December 2016, how much is the depreciation expense? Solution: Annual Depreciation = (Acquisition Cost Salvage or Residual Value) / Useful Life Annual Depreciation = (250,000 -10,000) / 10 Answer = PHP 24.000 2. Pedro Reyes purchased a delivery vehicle on April 1, 2016 amounting to PHP250,000. It is estimated that the vehicle will be useful for 10 years. The vehicle can be sold for PHP10,000 at the end of its useful life. If the accounting period being reported by Pedro is one (1) year from January-December 2016, how much is the depreciation expense? Solution: Annual Depreciation = (Acquisition Cost Salvage or Residual Value) / Useful Life Annual Depreciation = (250,000 -10,000) / 10 Annual Depreciation = PHP 24,000 Multiply the Annual Depreciation of PHP24,000 to the number of months in used/12, thus 24,000 x (9/12) Where the '9' represents the number of month from April to December. Answer = PHP18 000 3. Pedro Reyes purchased a delivery vehicle on January 1, 2016 amounting to PHP250,000. It is estimated that the vehicle will be useful for 10 years. The vehicle can be sold for PHP10,000 at the end of its useful life. If the accounting period being reported by Pedro is one (1) month (January 2016), how much is the depreciation expense for the month? Solution: Annual Depreciation = (Acquisition Cost - Salvage or Residual Value) / Useful Life Annual Depreciation = (250,000 -10,000) / 10 = P24,000 Answer = PHP24,000 / 12 = PHP2,000 for January 2016

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!